Dynamics’ new production lines started after years of construction, that segment grew by 73%

This was not a surprise:

“Outlook for 2025: organic sales growth between 16-20%, compared to previous organic sales growth between 12-16%. Reiterating EBIT growth higher than the organic sales growth and positive operational cash flow for the full year.”

I predicted in February that the guidance was truly underestimated, as it was, and over 20% is still possible. Saab is conservative in these forecasts.

Surprise for the upcoming stock market week. Inderes starts coverage of Saab! And even wilder news was the sell recommendation from 530kr —> a whopping 310kr. This is wild. A bold view!

An interesting chart from SAAB’s comprehensive report, which can indeed be found here for free reading.

"SAAB, stemming from Sweden’s industrial heritage, is a defense technology company whose offerings, suitable for Western use, cover the air, land, and naval domains. The current upturn in the defense sector, initiated by the war of aggression against Ukraine and reinforced by European and NATO demand, is driving SAAB’s high growth, profitability, and return on capital. As we expect this exceptionally strong demand period to ease much faster than the market appears to anticipate, we consider the current valuation (P/E 50x for 2025) unsustainable and initiate coverage with a Sell recommendation and a target price of SEK 310."

War expenditures (or, in current diplomatic language, defense expenditures) are not tied to the economic cycle, but they have varied very strongly as the threat perception has changed. The cornerstone of Renato’s SELL argument also appears to be the leveling off of defense spending demand later in the 2030s, whereas the market expects more aggressive growth further into the future.

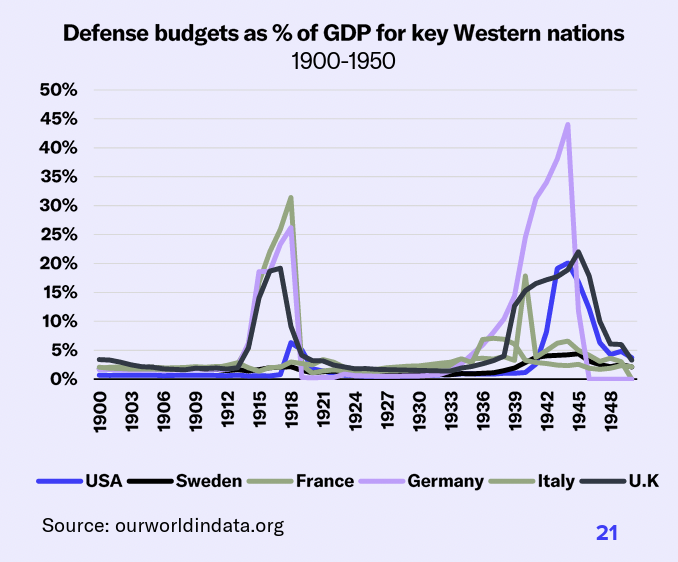

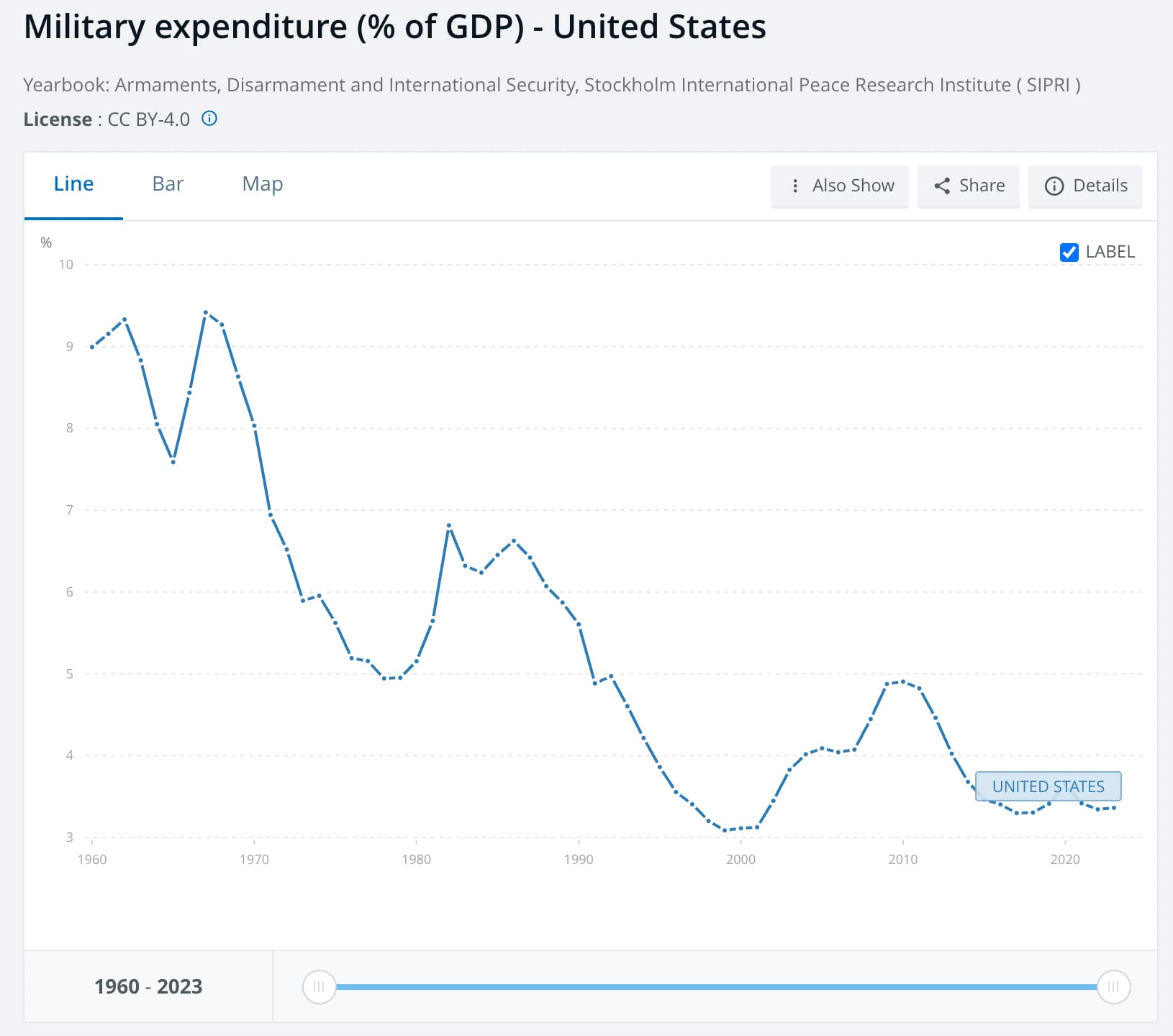

Below are examples of World War I and II. Note how even then, a 5% investment of GDP during peacetime was very rare.

However, the USA maintained a considerable ratio throughout the Cold War. Of course, it actively fought wars in Vietnam, and the Reagan arms buildup that brought down the main competitor in the 1980s is clearly visible there.

Calling defense spending war spending indicates something I won’t delve into further now. It should be noted, however, that the absolute majority of defense spending is used to prevent war from ever happening, i.e., to raise a deterrent. That, in turn, means a threshold to attack a country, i.e., the start of a war.

I myself have scraped decent profits from SAAB as well as many other “merchants of death.” I also know the industry through other channels. SAAB’s strength lies in its broad product portfolio and expertise in both operational aspects and training systems, meaning there is plenty to do despite the threat landscape. Its problems, in turn, are its small size and relative obscurity, as well as certain compatibility challenges, for example with the Gripen. However, time is now strongly on SAAB’s side due to changes in US policy, and it is considered a much more viable candidate than before. This also removes some of the problems. If production merely keeps pace with demand, SAAB has nothing to worry about in the current market, despite its tight valuation.

There might indeed be some air in Saab’s price, but this extensive report is mainly a purely numerical, i.e., conservative Excel exercise; it has not considered the possibility (speculated) that the war in Europe will expand instead of fading. It also has not considered that Saab’s worst competitor has traditionally been the USA, and that with Trump’s MEGA-politics, these competitors have severely shot themselves in the foot, which has again opened up an opportunity for Saab to win “mega-deals” that were previously regularly lost due to foreign policy reasons.

Here are Renato Rios’s comments on the Indian Air Force reportedly choosing French Rafales instead of Gripen.

Although SAAB’s Gripen is a highly competitive aircraft, the Indian Air Force appears to be leaning towards the French Rafale in a deal worth approximately SEK 200 billion. The selection of a system already part of the country’s defense infrastructure, along with the bidders’ capacity profiles, influences the outcome, and it would not be surprising if, according to media reports, the French Rafale wins the tender. As the probability of the French Rafale appears higher, we consider the situation normal business without impact on our forecasts.

Here are comments from Renato Rios on the MANGROVE consortium, led by SAAB Kockums, being selected to lead the Autonomous Undersea Warfare Battlespace Mission Network (AUWB MN) project.

Saab is probably the most well-known company on the list for Finns through its passenger car manufacturing. However, the company has not manufactured passenger cars for years, but is a company focused on defense industry products and aircraft manufacturing. Saab was founded in 1937 to manufacture aircraft for the Swedish Armed Forces. After World War II, the company expanded its production to cars. Saab’s car business was sold to General Motors in the early 2000s. Today, the Saab brand is owned by the Chinese-Swedish Nevs.

Saab is the largest defense industry company in the Nordic countries with a market value of approximately 127 billion kronor. Saab has approximately 18,000 employees worldwide.

@Sijoittaja-alokas linked an article about the defense sector in another thread. Let’s put it here too, as it also largely concerns Saab.

Renato Rios has given his comments regarding Friday’s announcement.

Saab announced on Friday an order of approximately SEK 4 billion from the Swedish Armed Forces. Not an unexpected continuation contract for Saab for Gripen maintenance. The order covers support and maintenance services for Gripen fighter jets for the years 2026-27. However, the size of the order is relatively small, and it does not cause changes to our forecasts.

Hi, I’m Renato from Inderes–I cover Saab! Our new language-agnostic forum is live; let’s discuss Saab, defense (maybe some geopolitics relating to that) and tangent topics. Looking forward to the dialogue!

Saab announced that it has received an order worth approximately SEK 9.6 billion from the Swedish Defence Materiel Administration (FMV). The order covers the final production phase of two previously ordered Blekinge-class A26 submarines, as well as additional materials and services. This is significant for the Kockums division and further strengthens the medium- and long-term order backlog and revenue visibility. As this is an extension of an existing program, we leave our forecasts unchanged.

What is going on with SAAB’s shares lately? Orders keep coming in, even if nothing extraordinary, and activity is still high, so sector demand seems to continue at a good pace–at least nothing seems to have changed fundamentally in the last couple weeks.

Our view is that the pullback mainly reflects the macro backdrop and a stretched valuation. The market appears to be assigning a slightly higher probability to de-escalation in geopolitical conflicts as the role of the United States in the war in Ukraine and in the Israel and Hamas conflict has become clearer. Given the elevated valuation, the share is sensitive to even small signals of lower conflict intensity, prompting investors to risk adjust their Saab positions. If this is the start of a broader de escalation, the share price could continue toward more normalised levels. At the same time, Europe and the wider world are likely to keep rearming, which suggests the valuation will stay above what we consider reasonable in the long term, though not at today’s levels.

Here are Renata’s comments on SAAB’s follow-up order.

SAAB announced that it has received an order of approximately SEK 2.6 billion from the Swedish Defence Materiel Administration (FMV) for the continuation of concept studies for future fighter systems during 2025-27. The order is strategically important for long-term competitiveness, but its scope and size are in line with our expectations, so we leave our forecasts unchanged.

Here are @Renato_E_Rios’s comments as Saab publishes its Q3 report on Friday.

We expect revenue to remain in line with the 2025 guidance, driven by robust project execution and order backlog conversion, and a stable order intake to maintain the order backlog. We anticipate profitability to remain relatively strong. Ahead of the report, we do not see fundamental changes to the investment story or the underlying demand dynamics.

The stock price reacted surprisingly moderately today. A deal for 100 fighter jets is every shareholder’s wet dream. Even ten would have been enough. As these haven’t been sold to more than a few countries. It would be absolutely amazing IF it materializes.

The quantity is surreal even from a production capacity standpoint; it would take a decade to manufacture even with several production sites. It feels like this utopian quantity is aimed at achieving maximum media visibility and sending some kind of message to those threatening Europe. Would there even be enough money for the upkeep of such a fleet? The aircraft themselves would cost some 10-12 billion. That could easily be found from partner countries.

Here are @Renato_E_Rios’ comments on this recent major news. The Swedish Prime Minister and the Ukrainian President signed a memorandum of understanding yesterday. The potential deal is valued at approximately SEK 130–200 billion, and could increase revenue by approximately SEK 18 billion by 2029, with the potential to improve profitability. The potential deal supports our forecasts and would significantly strengthen them if realized. However, details, probability, and timing remain uncertain. The signed agreement could trigger forecast upgrades depending on its size. For now, we keep our forecasts unchanged and monitor the situation.