I’ll post my own scattered thoughts on the results in this thread as well.

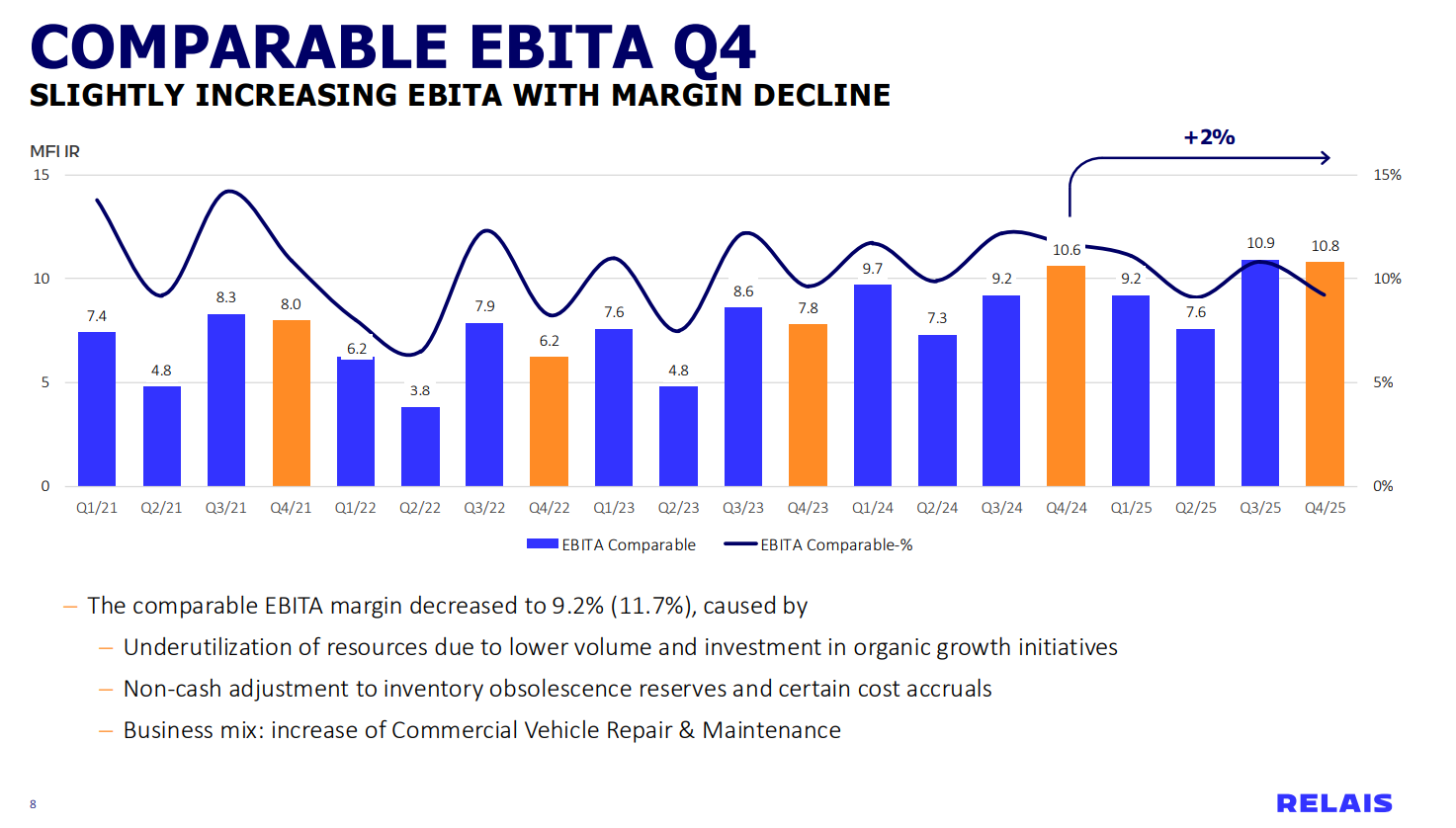

It was a somewhat soft quarter in terms of profitability, there’s no getting around that. However, a quarter is too short a timeframe to draw significant conclusions in one direction or the other.

After Q3, investor expectations were clearly higher, as the market gave a bit of a slap after the result. Though, the closing price on the earnings day was only about -5%, so there was probably some of that famous margin of safety in the valuation, as a worse thrashing was avoided despite the slight disappointment.

The weaker profitability was explained by, among other things, low (workshop?) capacity utilization, and apparently, the earnings contribution from the Norwegian workshops acquired in the spring was poor. The numbers weren’t opened up in more detail regarding that. As maintenance/workshop services increase their share of the group’s net sales, profitability also decreases structurally slightly when measured by profit margin, but on the other hand, the return on capital should be better in that business.

In the Q&A, it was said about the Norwegian workshops that they are currently implementing best practices and lessons from Finland and Sweden to improve profitability, etc. This was successfully done in Finland with Raskone back in the day, where the absolute result was more than doubled very quickly.

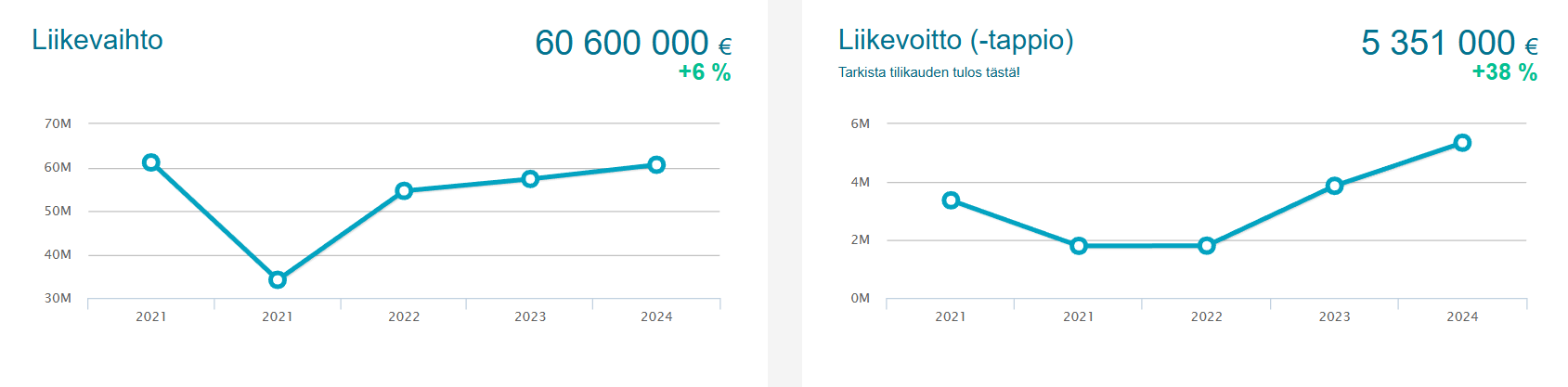

Raskone Oy:

There will always be fluctuation between quarters. Q1 has been very good for Relais so far in terms of weather; utilization rates have definitely risen from the Q4 situation, as the freezing weather has lasted for weeks and there’s no end in sight yet. There might even be a positive surprise in store. The CFO at least couldn’t keep a straight face when asked about this.

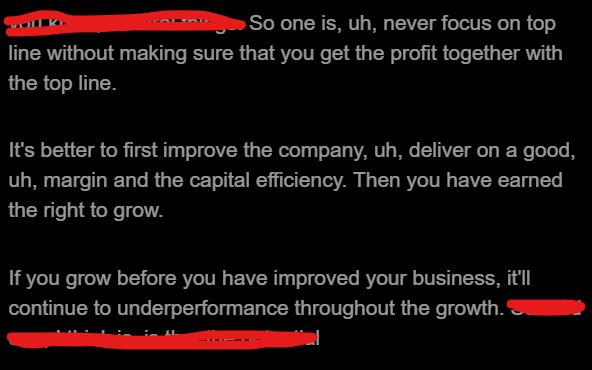

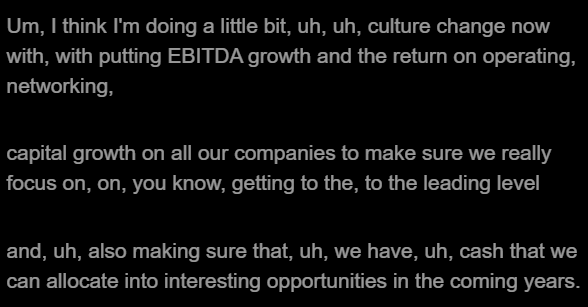

Then to the more interesting and essential part, i.e., long-term matters. The new strategy/financial targets haven’t been published yet, but the new CEO’s speeches gave some hints. It strongly seems that we will get what you would expect from a Swedish CEO, i.e., the familiar tricks and metrics from Swedish serial acquirers operating with decentralized business models. ![]()

How many times did we hear the word decentralized or capital allocation or capital efficiency in the presentation? ![]() Additionally, it seemed that the Profit/Working Capital ratio (return on working capital %) or similar, familiar from those same serial acquirers in our western neighbor, would be introduced into the new strategy as a key mindset and metric. All in all, sensible thoughts from the new CEO: focusing on core operations, aiming to encourage every business unit to improve return on capital, and allocating capital where it yields the best returns. Of course, the main owners will continue to decide if part of this capital goes back into the owners’ pockets. It will be interesting to hear before summer what the new strategy and targets actually contain.

Additionally, it seemed that the Profit/Working Capital ratio (return on working capital %) or similar, familiar from those same serial acquirers in our western neighbor, would be introduced into the new strategy as a key mindset and metric. All in all, sensible thoughts from the new CEO: focusing on core operations, aiming to encourage every business unit to improve return on capital, and allocating capital where it yields the best returns. Of course, the main owners will continue to decide if part of this capital goes back into the owners’ pockets. It will be interesting to hear before summer what the new strategy and targets actually contain.

Momentum Group’s capital allocation, for example, is built around this P/WC, which was just discussed in the serial acquirer thread. In itself an obvious concept, but effective when implemented with discipline.

Summarized from Momentum’s annual report: