It is worth noting here that Rebl’s strategic spearhead project and its growth potential are based more on marketing information logistics solutions (MiM), which client companies using retail media may need. The company already has many retail clients, to whom it offers printing services (direct mail), visibility solutions (displays and banners), and other services. Thus, the growth of Rebl’s retail media would on the one hand facilitate the sale of MiM solutions, but at the same time, companies’ need for e.g., in-store displays would likely increase. However, the greatest growth and profitability potential lies precisely in those MiM solutions.

3 Likes

Here are Arttu’s comments on Rebl’s recent acquisition. ![]()

1 Like

In my opinion, a lot of good things are happening in the company right now. The direction is really positive. Many new initiatives and the change from old to new is fast.

1 Like

Here are Arttu’s preliminary comments as Rebl publishes its Q1 report on Friday.

We anticipate the operating environment has remained challenging, with both revenue and operating profit continuing to decline. The guidance, which anticipates stable revenue and improving results, is unlikely to be revised in connection with the report. In connection with the preliminary comments, we made slight changes to our operational forecasts and added the non-cash flow impact resulting from the positive value development of the Ilkka ownership to our forecasts. From the results day, we expect confirmation of the positive development of the operating environment, as well as comments on the impacts of the trade war on the industry, the sales pipeline, and the first steps of the MiM solution being developed for Tokmanni.

Here is Arttu’s company report right after Q1.

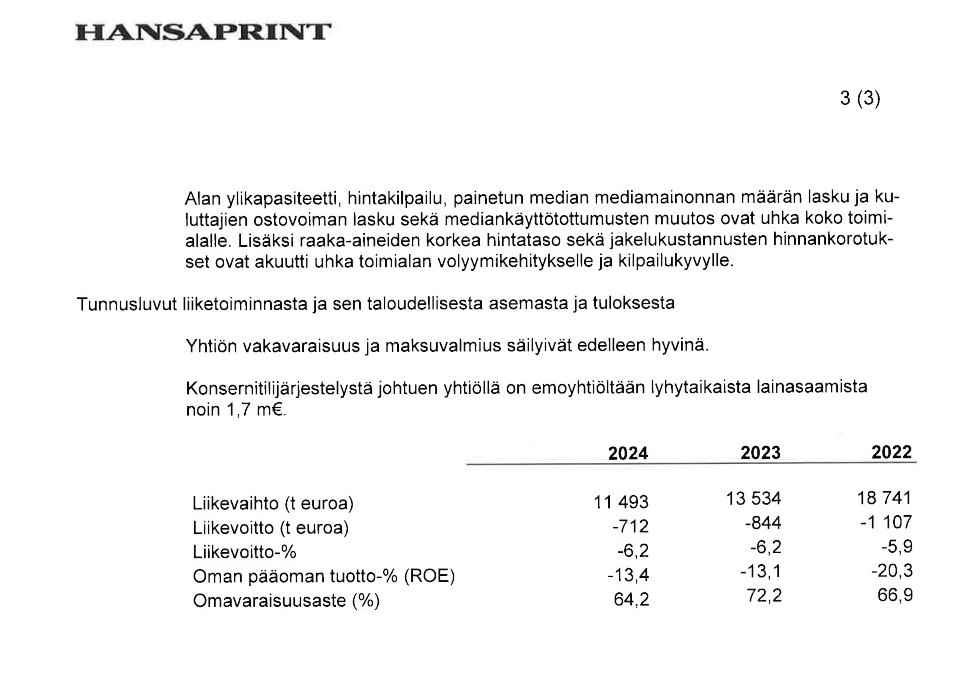

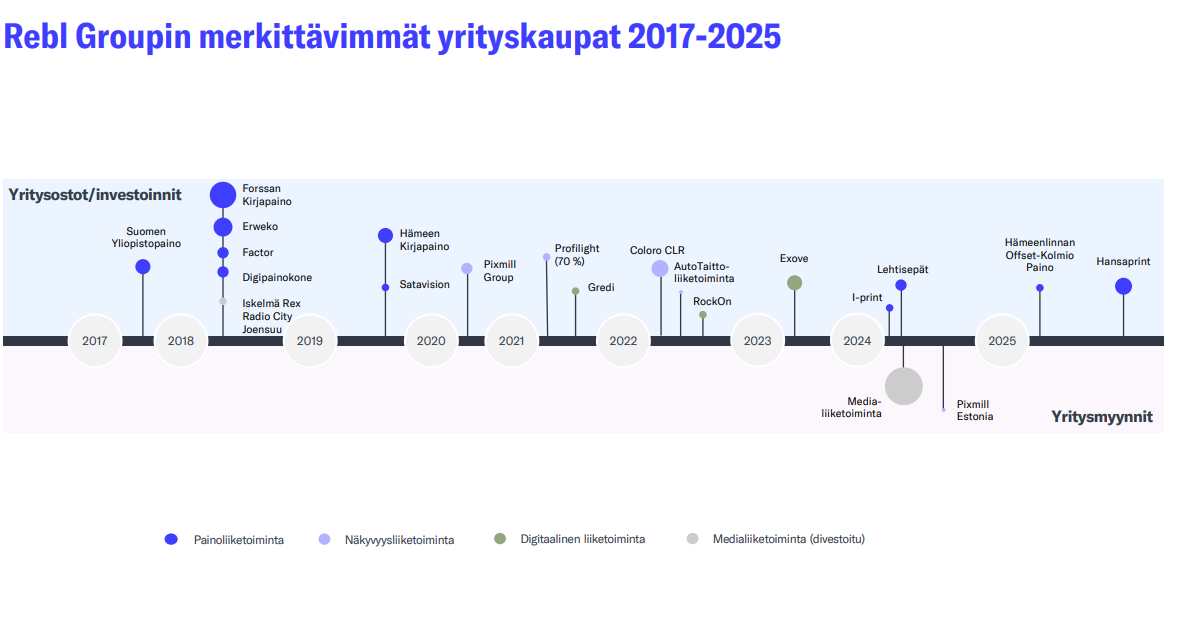

Rebl Group has apparently decided to play out this dwindling printing business card to the end: Rebl Group is acquiring its competitor Hansa Print, whose revenue in 2024 was €11.5M and operating profit was at a loss of €0.7M.

Hansa Print’s owners threw in the towel. The purchase price is two euros, and Rebl Group records €0.3M in negative goodwill, meaning the acquisition was made below book value. Hansa Print’s equity after continuous losses was €0.8M in 2024, so the beginning of the year has probably also been loss-making, as the businesses were acquired for free. P/S ratios are starting to look good when companies with €10M in revenue are bought for free ![]() .

.

Overcapacity in a declining industry is not an attractive environment, but perhaps Rebl Group aims to be the last of the Mohicans in the industry, so that the pricing environment would change. These acquisitions below book value probably serve as a substitute for organic investments, as additional machinery and equipment will also be obtained from Hansa. However, Hansa’s EBITDA was also at a loss of €0.5M in 2024, so it certainly wasn’t a cash cow company. Nevertheless, Rebl Group has a very interesting angle on an industry where volumes are decreasing year by year as everything shifts to digital. It remains to be seen how the company fares.

Here is the latest financial statement from the trade register:

hansaprintoy.pdf (8.0 MB)

Here is the release itself:

6 Likes

The sad thing about these arrangements is that they should have been implemented ages ago. It’s the stubbornness of the industry owners that these arrangements are being made so late.

Perhaps now a reasonable balance will finally be achieved for the market; a lot of time and money has certainly been spent on this.

1 Like

Here are Arttu’s comments on Rebl Group’s recent acquisition.

Rebl Group announced on Friday that it had acquired Hansaprint’s business for a marginal price of two euros. The deal strengthens Rebl’s traditional printing as well as its store and event marketing solutions. Hansaprint’s operations have been loss-making. Despite this, we view the deal neutrally, as the price paid for the business is low, and Hansaprint’s deep integration may enable synergy benefits that improve the group’s results. We will add the impact of the deal to our forecasts in the coming days.

2 Likes

And here was also a fresh company report from Arttu. ![]()

With the Hansaprint deal, Rebl aims to increase its own utilization rates, especially in the Printing Business. Although we anticipate that the change negotiations held due to the deal will raise the company’s profit, the value creation of the new entity remains at a modest level. We raise our target price to 1.50 (previously 1.25) euros due to forecast changes. The recommendation remains at the reduce level due to the stock’s weak return-risk ratio.

1 Like

Sale’s comments on Rebl’s long-term contract ![]()

Arttu has written a company report on Rebl Group after the negative profit warning.

Rebl Group lowered its operating profit guidance and forecasts a decline in earnings in 2025. In relation to the cost savings planned for the rest of the year, this was a clear disappointment. We clearly cut our earnings forecasts in connection with the report, which led to our target price decreasing to 1.3 euros (previously 1.5). Due to the stock’s high risk level, stretched valuation, and subdued capital return outlook, we reiterate our reduce recommendation.

Profit Warning Release:

REBL GROUP OYJ INSIDE INFORMATION 4.8.2025 AT 3:30 PM

Rebl Group Plc lowers its earnings guidance for 2025 regarding operating profit. Based on the weaker-than-expected revenue and earnings development in the first half of the year and the forecast for the rest of the year, operating profit is expected to fall short of the previously given outlook, according to which operating profit would improve from the 2024 level.

The company’s operating profit outlook is weakened by the continued uncertainty of the general economic situation and its slowing effect on the start of new investments. The slower-than-expected recovery of the markets has been reflected in demand remaining weaker than estimated in all business areas, and at the same time, the increased cost level has weakened earnings development.

Previous guidance (27.2.2025-4.8.2025): The Group’s revenue is expected to remain at last year’s level, and operating profit is estimated to improve from the 2024 level. In 2024, the Group’s continuing operations had revenue of 114.0 million euros and an operating profit of -1.2 million euros.

New guidance (4.8.2025-): The Group’s revenue is expected to remain at last year’s level, and operating profit is estimated to weaken from the 2024 level.

1 Like

Here is a recent company report from Arttu after the latest “events”.

Rebl Group announced it would initiate change negotiations for operational and financial reasons to improve the group’s profitability and competitiveness, secure future operational capability, and streamline operations. This, together with the recent profit warning, in our opinion, signals that an improvement in the demand environment is not expected anytime soon. Due to this news, we made forecast changes, which remained moderate on a net basis. Thus, we reiterate the target price of 1.3 euros and the ‘reduce’ recommendation due to the challenging valuation of the share.

Artun’s comments on Rebl Group concluding its change negotiations.

Here are Arttu’s preliminary comments as Rebl Group publishes its results on Friday. ![]()

We expect the group’s revenue to have decreased and operating profit to have weakened amidst a sluggish economic situation. The company lowered its earnings guidance at the beginning of August, which is presumably going to be reiterated in connection with the report. In addition to normal earnings drivers, our interest on the results day will focus on business-specific demand situations and outlooks, as well as the sales pipeline for MiM solutions.

Arttu has prepared a new company report on Rebl Group after the Q2 releases.

Rebl Group’s Q2 result weakened from the comparison period and was at an absolutely weak level. The sluggish earnings trend has also tightened the balance sheet position, as a result of which the company has started negotiations with its financiers to secure future funding. In our opinion, the risk level of the share is high from both a valuation and a balance sheet perspective.

Arttu has published a comprehensive report on Rebl Group, which, like other extensive reports, is accessible to everyone, meaning there are no paywalls. ![]()

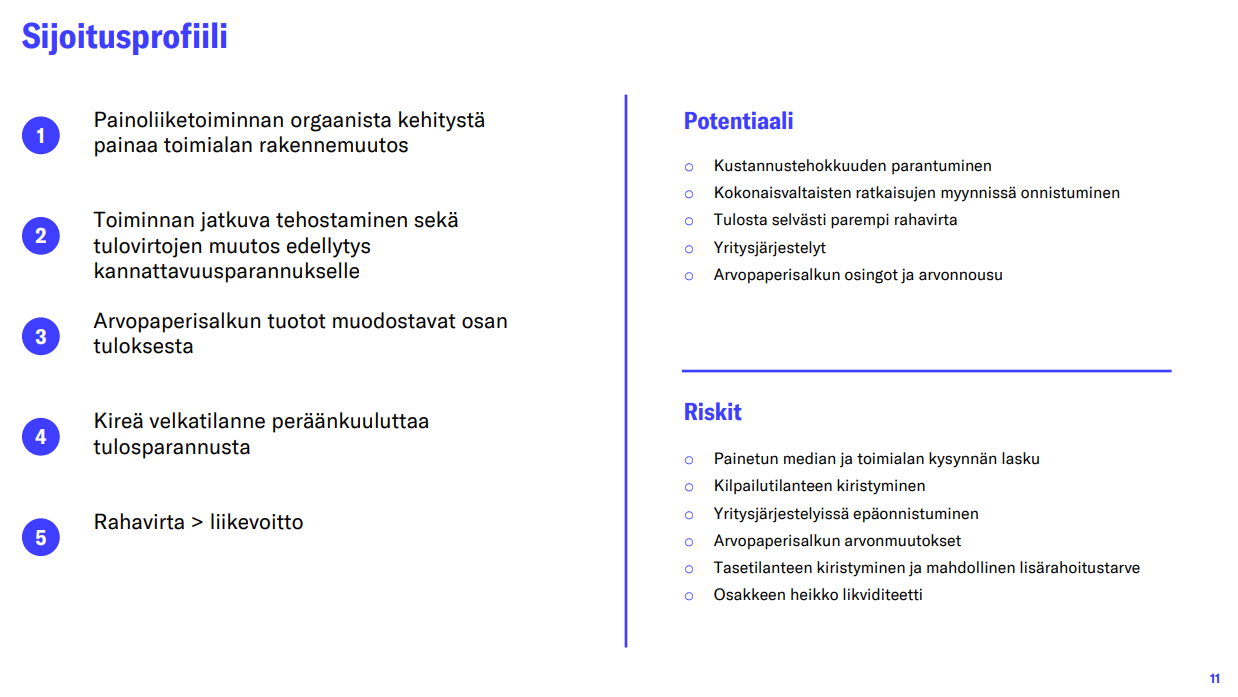

Rebl Group’s profitability improvement relies on enhancing the efficiency of the declining Printing Business and accelerating the earnings growth of other business operations. The ramp-up of Marketing Information Management solutions serves as a crucial driver for earnings growth, although its true impact is yet to be proven due to its early stage. In our opinion, the stock’s risk-reward ratio is at a weak level due to the elevated valuation and indebtedness.

https://www.inderes.fi/research/rebl-group-laaja-raportti-tulovirtojen-tervehdyttaminen-viela-kesken

Quoted from the report:

1 Like

Today, we discussed Rebl Group quite a bit with Arttu, and we tried to take slightly different angles for the video than what was covered in the video filmed by Antti a year ago. That’s why, for example, we completely dropped the discussion of the securities portfolio today, as the situation hasn’t changed much in a year. ![]()

Has Rebl Group become a prisoner of market conditions, as the printed media market shrinks, but it’s difficult to find a buyer for the printing business? Analyst Arttu Heikura discusses Rebl Group’s current state and future scenarios.

Topics:

00:00 Introduction

00:19 Printing business facing a challenging situation in a shrinking market

04:07 Demand for visibility solutions is growing

06:45 Digital business is the group’s youngest segment

09:55 Marketing data management as a strategic spearhead project

16:32 Indebtedness is high

18:17 What would turn the tide?

25:10 Share valuation

1 Like

Here are Vilppo’s comments on how Rebl Group lowered its revenue guidance.

Petri and Arttu have prepared a new pre-company report as Rebl publishes its Q3 results on Friday. ![]()

We anticipate the company’s total revenue to have reached slight growth, driven by an acquisition. However, the positive impact of the acquisition is largely overshadowed by the contraction in organic revenue, which also keeps the earnings level weak. We have made negative adjustments to our forecasts, reflecting which we lower our target price to 1.05 euros (previously 1.10 euros). However, due to the share price decline, we raise our recommendation to ‘reduce’ (previously ‘sell’). Our recently published comprehensive report on Rebl Group can be read from this link.

Here is a new company report on Rebl Group from Petri and Arttu right after Q3. ![]()

Rebl Group’s Q3 figures reported on Friday fell slightly short of our forecasts, as the revenue impact of the significant Hansa acquisition was smaller than we anticipated. We have made slight downward revisions to our forecasts, which were lowered in connection with the earnings preview, after the report. We expect efficiency measures to turn the company’s operating profit (EBITDA) to growth next year, but a sustainable turnaround in earnings requires a return to revenue growth, which is challenging with the current structure. In our opinion, the share already prices this in, which, together with high indebtedness, keeps the risk-reward ratio weak. Thus, we reiterate our target price of 1.05 euros and our Reduce recommendation.