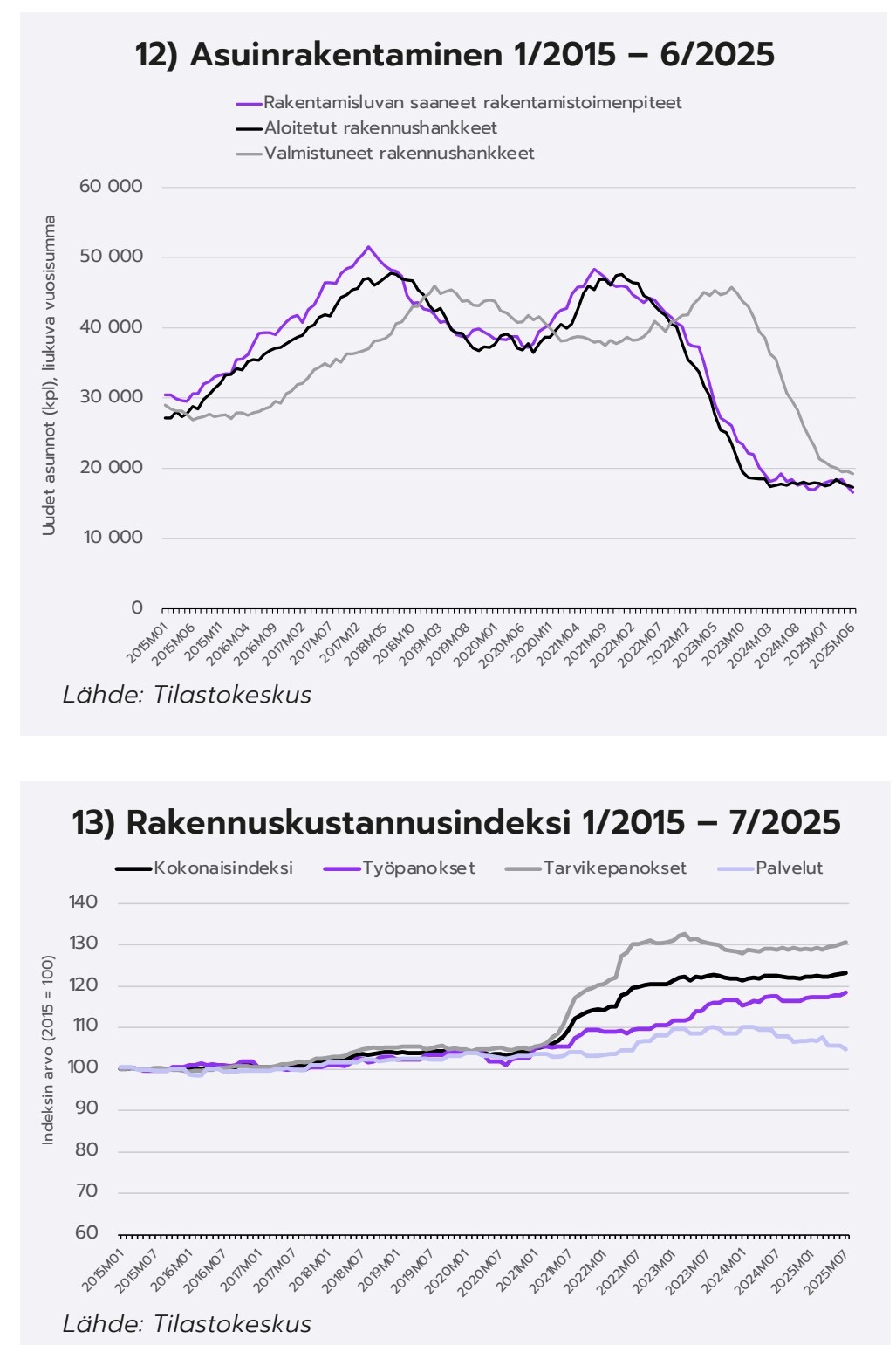

Indeksissä on perusvuosi 2015. Silloin rakennettiin 8500 ARA-asuntoa. Nykyään tuo valtionputiikki, joka vastaa valtion tukemasta asuntotuotannosta on Varke ja viimeisimmän datan mukaan liukuva 12kk tuotanto on 9000 asuntoa ja alkuvuoden muutos edelliseen +16%. Noista 9000 asunnosta vajaa 2400 on ASO asuntoja. ASO tuotanto tulee hiipumaan ensi vuoden aikana, kun tähän tietoon viimeiset ASO-asunnot valmistuvat. Alkuvuodesta arvioitiin vuoden 2025 aloitusten jäävän Varke-tuotannon osalta 6000 asuntoon. Näin ollen voisi olettaa että tuota käppyrää saa skaalata alaspäin uudelleen ensi vuonna, koska vapaarahoitteinen asuntotuotanto ei enää ehdi ASO-tuotannon loppumisesta aiheutuvaa lovea paikkaamaan vaikka saisikin jostain piristysruiskeen.

11 tykkäystä

Asuntomessut: Valtava kävijäpettymys | Kauppalehti

Ampparin linkistä hetken luettavissa ilman maksumuuria. Ei lupaa hyvää rakennusteollisuudelle kun uudisrakentaminen ei tuon enempää kiinnosta. Ododtuksissa 100.000 käviää, tuli 65.000

4 tykkäystä

Kaikki on suhteellista. Asuntomessut varsin pitkän matkan päässä ns. ruuhka-Suomesta, millä varmasti vaikutusta varsinkin ei-niin-vakavalla-mielellä kävijöihin.

Jos asiaa peilaa uusien asuntojen myynnin lähes täydelliseen pysähdykseen, on kävijämäärä mielestäni yllättävänkin korkea.

3 tykkäystä

Oulun asuntomessualue oli yhtä kaukana ruuhkasuomesta myös vuonna 2005 ja silloin kävijöitä oli 121.000, eli lähes tupla määrä tämän vuotiseen verrattuna. Lisäksi Oulun ja sen liitoskuntien väkiluku on noussut vuodesta 2005 noin 40.000:lla.

20 tykkäystä

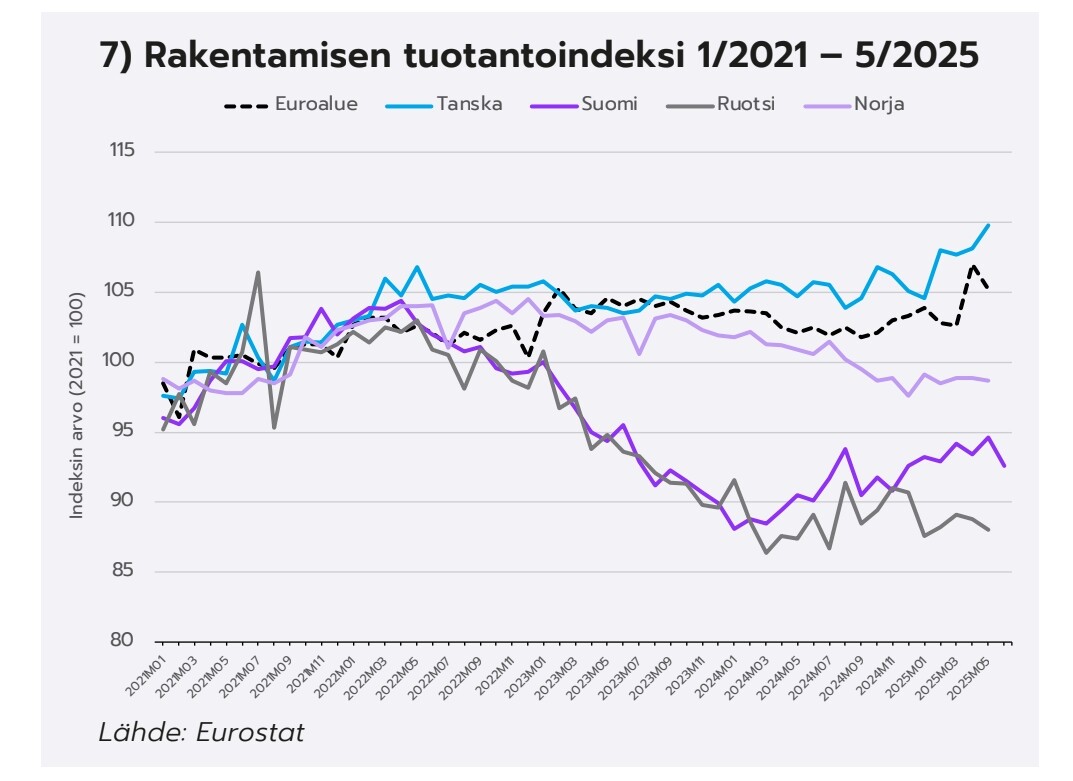

Raklin suhdannekatsaus.

2025 maltillista kasvua, 2026 nousua.

Asuinrakentaminen jatkaa mörnimistä, ja kustannuspanosten edulliseksi tulemista turha odottaa avuksi, tarvikkeet jääneet nousseelle tasolla, palkat nousevat.

Sinänsä uudistuotantovarastoa ei kovin paljon ole vapaana, se on loppuunmyyty kyllä ennen kuin uusia asuntoja valmistuu. Mutta laimea kysyntä, asuntokaupan ketjuuntuminen, edullisemmat vanhat asunnon, yms yms

Kokonaisuudessaan rakentamisen kuluvan vuoden ennustetta on heikennetty ja osa kasvusta siirtyy ensi vuoden puolelle. Rakentamisen tuotannon arvon odotetaan nyt kasvavan

2,5–3,0 prosenttia 2025 ja 7 prosenttia 2026.

rakli-suhdannekatsaus-syyskuu-2025.pdf https://share.google/RgxgVSmCitKmfHivQ

9 tykkäystä

Jussi Halme on tehnyt videon rakennusalaan liittyen. ![]()

*Suomen rakentaminen on juuri nyt isojen haasteiden keskellä – asuntorakentaminen on pysähtynyt historiallisen alas, ja tuhannet osaajat ovat hakeutuneet töihin ulkomaille. Mutta samalla remonttibuumi, valtion massiiviset investoinnit ja suuret infraprojektit pitävät alaa elossa. *

Onko edessä pitkä synkkä kausi vai uuden kasvusyklin alku? Tässä videossa sukellamme syvälle rakentamisen nykytilaan, eri sektorien eroihin ja siihen, mistä harvat valonpilkahdukset löytyvät.

5 tykkäystä

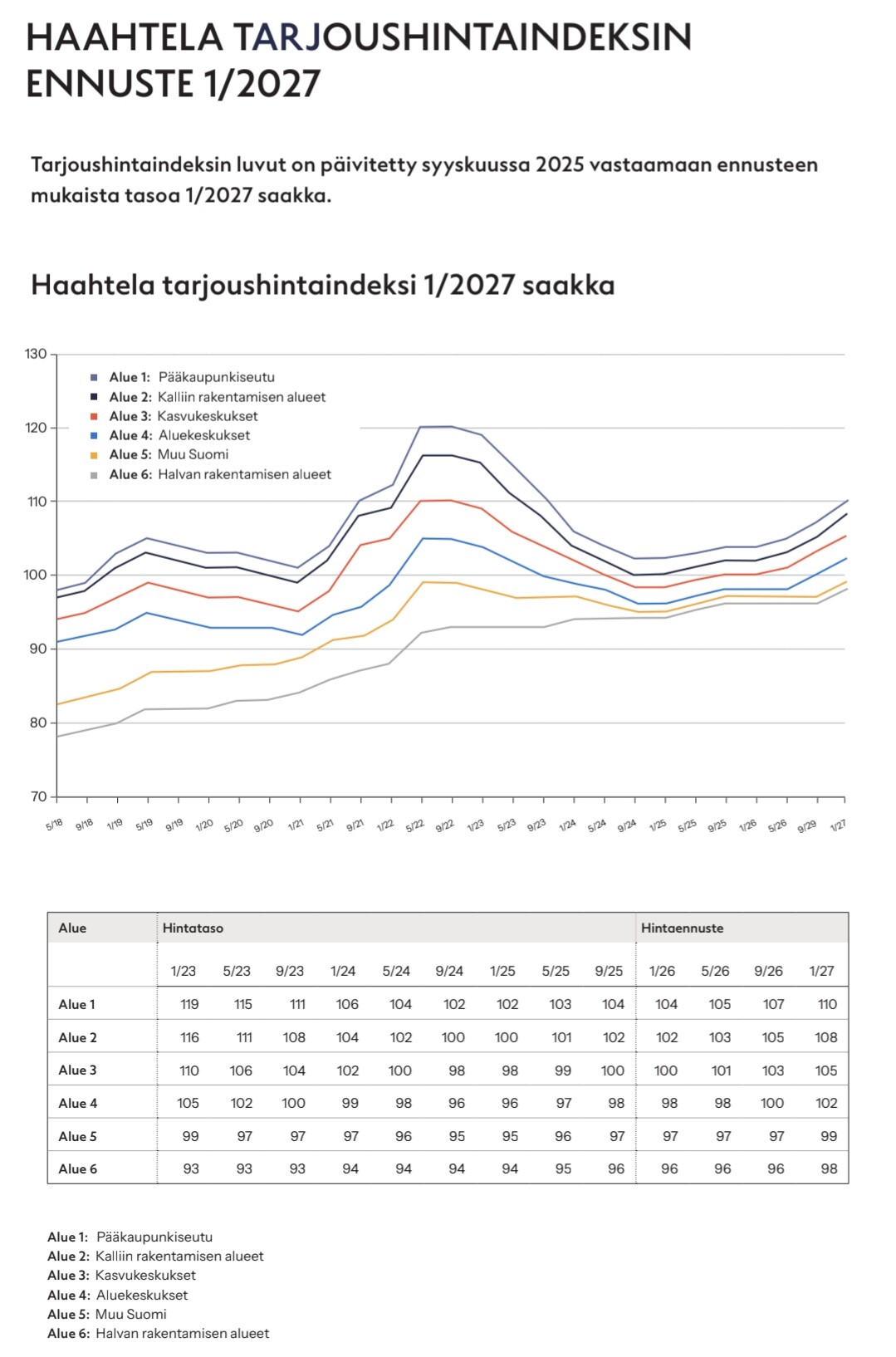

Tiukkaa settiä ja näkemystä Haahtelan tarjouhintaindeksin suhdannekatsauksessa.

Itse povaan, että rakentamisen alakulo tulee jatkumaan, mutta muutos ja piristyminen tulee sitten aikanaan yllättäen nopeasti ja huomaamattomasti.

14 tykkäystä

Uutta dataa myönnettyjen rakennuslupien määrästä.

4 tykkäystä

Haahtelan karun tekstin päälle ennusteensa jonka pitäisi peilata tarjoushintoja / kustannuksia.

Kiitoksia kaikille hyvistä pointeista,

-korkotaso - vaikka laskenut onkin - ei annan asuntosijoittajalle kunnon tuottoja

-heikoilta alueilta ei varaa muuttaa, omasta ei saa oikein pohjarahaa jolla tekisi muuttovoittokunnilla oikein mitään

-hyvä ansiokehitys keskimäärin ei tarkoita esim että nuorilla olisi varaa ensiasuntoihin

-muutama vuosi sitten asunnon ostaneet ovat lähtötilanteessa, ts asunnon velkasuhde ennallaan asuntojen hintojen laskettua, ts velanmaksukyky vs pankkien politiikat

-heikkojen myyntivuosien jäljiltä myyntipainetta / pettyneet asuntosijoittajat, asuntorahastot, yms

-talousluottamus kannusta ottamaan lisää velkaa

-toisaalta asuntokaupan heikko tola luo tilannetta, jossa ei uskalleta vaihtaa kun oman myynnistä ei ole tietoa, ketjuuntuminen

-yms

11 tykkäystä

Ja kuten logiikka menee, ei lupia - ei rakennuksia.

Artikkeli vain tilaajille, mutta uskaltanen tämän verran sieltä raapaista:

Vasta huhtikuussa alan yrityksiä edustava Rakennusteollisuus RT ennusti toiveikkaasti, että rakentaminen kasvaisi tänä vuonna 4,0 prosenttia ja ensi vuonna 6,0 prosenttia.

Tätä lähellekään ei päästä. Leikatussa ennusteessa RT odottaa, että tämän vuoden kasvu jää alle prosenttiin. Ensi vuoden kasvuksi ennustetaan enää 3,5 prosenttia.

”Alkuvuosi petti odotukset ja rakennustuotanto on jäänyt ennakoitua heikommaksi. Tämän vuoden kasvu yltää vain niukasti nollan yläpuolelle. Vahvempaa toipumista on luvassa aikaisintaan vuonna 2027”, tiivistää Rakennusteollisuus RT:n pääekonomisti Jouni Vihmo.

6 tykkäystä

Liittyy toki yhtä lailla asuntosijoittamiseenkin, mutta laitetaan tähän kun liittyy tietysti päivän teemaankin eli RT:n tänään julkaisemaan suhdannekatsaukseen. 60 dian setti, joka täytyy käydä illemmalla läpi Sandelsin kanssa, mutta nyt jo yksittäisenä poimintana yksi:

Tässä jos missä, olisi kiva saada kylkeen maantieteellinen erittely, kun maassamme se vuosi vuodelta jakaantuu yhä enemmän kahtia.

Sitä kun ei ole (data olisi olemassa, mutta en jaksa selata), niin on mentävä tällä. Tälläkin hetkellä on siis melkein 70 000 asuntoa etsimässä ostajaa/vuokraajaa? Jos nämä kaikki eivät ole Pihtiputaalla, niin eihän tilanne nyt vielä hirveästi kannusta lisää rakentamaan.

11 tykkäystä

Ylempi kuvaaja ei kuitenkaan kerro vapaana eli tyhjänä olevien asuntojen määrää. Tällä hetkellä moni myy ennen kuin ostaa uuden asunnon. Kertooko tilasto enemmän pitkistä myyntiajoista vai oikeasti tyhjillään olevista asunnoista. Oman arvioni mukaan enemmän jälkimmäisestä.

Oikotiellä 15 suurimmassa kaupungissa 18000 tyhjää asuntoa (kaikki asuntotyypit, mukaan lukien rivarit ja omakotitalot). Näistä varmaan osassa asukas, koska ilmoitus asuntoilmoitukset tehdään (yleensä) kun vuokralainen vielä huoneistossa. Vuokra-asuntojen kohdalla luku kertoo kuitenkin paremmin tyhjänä olevien asuntojen määrän kuin myynnissä olevien asuntojen data.

1 tykkäys

Aina on monia jotka laittaa asunnon myyntiin ennen uuden ostamista. Ja yhtä lailla tilasto kertoo aina noista molemmista taustatekijöistä. Painotus tosiaan vaan vaihtelee.

Tilastointi kun pysyy samana vuodesta toiseen, niin pitäisin oleellisimpana havaintona tuota trendiä ja absoluuttisia määriä. Eli ollaan edelleen kirkkaasti sillä puolella että tarjontaa on enemmän kuin kysyntää.

2 tykkäystä

Tänään julkaistu mielestäni hyvä kirjoitus asuinrakentamisen tilasta ja tapahtumista mitkä vaikuttaneet nykyiseen asuinrakentamisen markkinaan sekä rakennusyhtiöihin joilla on ollut omaperusteista kerrostalotuotantoa.

Kirjoituksen perusteella ei ole odotettavissa sen kummempaa muutosta seuraavan 2-3 vuoden aikana tuotantomäärien kasvuun asuinmarkkinassa.

9 tykkäystä

Pahin syöksy selvästi takanapäin, mutta käänne ylös antaa edelleen odottaa itseään.

7 tykkäystä

Referaatti olis kiva!

(Eihän nyt kellään mitään maksullista hesaria ole)

Tuossa huomattava on “book-to-bill”-suhteen kääntyminen eli valmistuu enemmän kuin mitä tulee uusia lupia. Ja silloinhan mennään aina alamäkeen. Lupien vähyys tekee koko ajan uusia ennätyksiä, joka voisi puoltaa jo pikku hiljaa kulmakertoimen muutosta, mutta luulen että vaakasuunnassa edetään jonkun aikaa.

Uudisrakentamiseen myönnettyjen rakentamislupien kuutiomäärän vuosisumma oli syyskuussa 2025 suurin Uudellamaalla ja Pirkanmaalla. Kuutiomäärä oli yhdeksässä maakunnassa suurempi kuin vuotta aiemmin.

In Finland we call this kasvukeskuksiin rakentamista.

4 tykkäystä

Tietysti 2022–2023 nähty vapaa pudotus on takanapäin mutta kyllä tuo statistiikka lohduttomalta näyttää, asunnoissa kun tarkastellaan liukuvaa vuosisummaa kappalemäärissä Tilastokeskuksen aikasarjan (vuodesta 1995 eteenpäin) matalin taso syyskuussa sekä luvissa että aloituksissa. Korkotuetun tuotannon määrän tippuessa on vaikea nähdä asuntoaloituksissa kokonaisuudessaan merkittävää kasvua ensi vuonnakaan, vaikka lähtötaso on matala. Toisaalta tuetun tuotannon lasku helpottaa vuokra-asuntojen ylitarjontaa.

16 tykkäystä

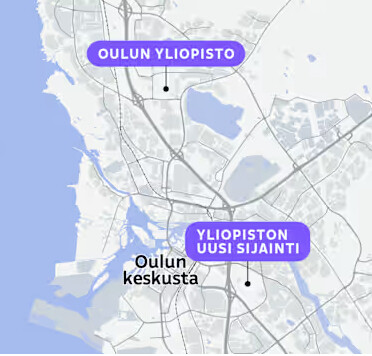

Oulussa iso päätös tänään. Yliopisto muuttaa Linnanmaalta Kontinkankaalle vanhan sairaalan paikalle.

Tämä tulee tietämään aivan massiivisen määrän töitä alueelle. Alkuvaiheessa konsulteille ja suunnittelijoille, työ alkaa heti ensi vuoden alusta. Infraa pitää laittaa valtavasti uusiksi, luultavasti koko joukkoliikenteen konseptia pitää miettiä puhtaalta pöydältä. Myös uutta asuntorakentamista alueelle tullaan tarvitsemaan.

Oulussa vuosikymmenen loppua kohden starttaamassa isoja projekteja: Monitoimiareena, matkakeskus ja Yliopisto. Nämä sijoittuu noin kilometrin säteelle toisistaan, joten infrapuolella tulee hommaa riittämään.

23 tykkäystä

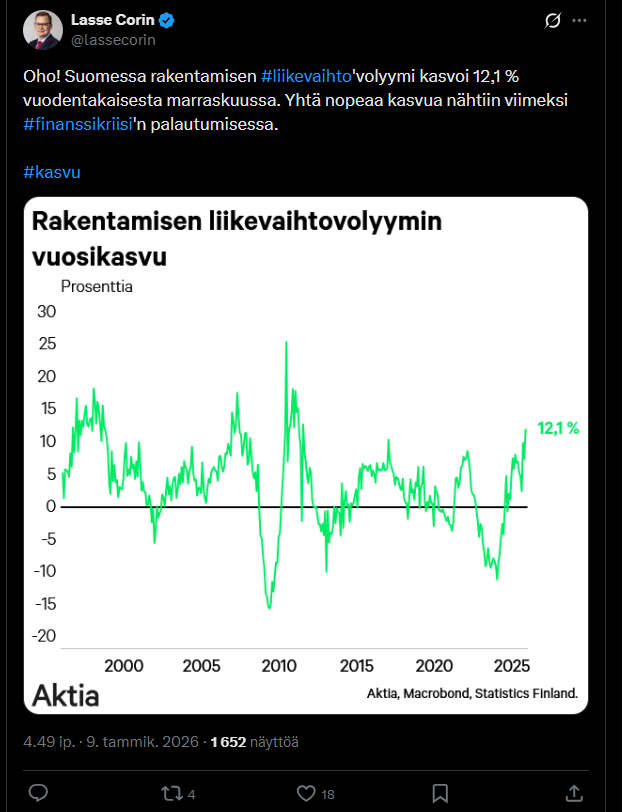

Tällainen tuli vastaan @JHeiskanen:n jakamana ![]()

21 tykkäystä

Vastaava korkeakoulun siirto on työn alla myös Hämeenlinnassa. HAMKin ja kaupungin suunnitelmissa on siirtää kampus joko bussiaseman tilalle tai järvenrantakaistaleelle tien toiselle puolelle.

2 tykkäystä