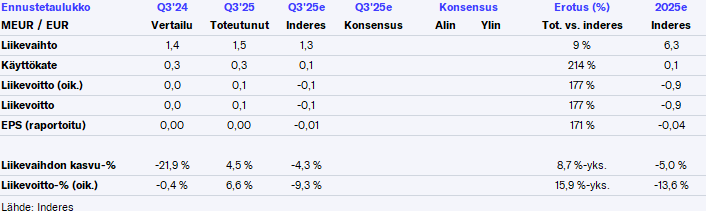

The report was surprisingly good in terms of numbers, as revenue gained momentum from license deals. Based on the interview, deals could well be realized in the last quarter, but from the outside, it is difficult to estimate how license deals will develop and be timed.

The ratio of materials and services to revenue decreased slightly compared to previous quarters. A lower level may, of course, also be related to the higher level of license deals.

Employee benefit expenses per person were at a lower level than in the comparison period. For other recent quarters, they have been quite high. Other operating expenses were slightly below the comparison period, so significantly larger investments in sales and marketing were apparently not made.

EBITDA is positive for the current year, so if desired, significant investments can be made in sales and marketing during the last quarter. Investments have indeed been made in at least a few events right at the beginning of the quarter.

R&D expenses were capitalized slightly less than in the comparison period, so the result is on a slightly stronger footing in that regard. The difference between R&D depreciation and capitalization was 129 thousand. At least I like to think that the adjusted operating profit is better by the same amount. After next year, depreciation should decrease to approximately the level of capitalization, which will also make the reported figures better.

Depreciation was almost 50 thousand lower than in the last quarter. After next year, I understand they will roughly halve from the current level. Adjusted operating profit for the quarter was 97 + 129 = 226 thousand, or 15.3% of revenue.

Financial expenses were 16 thousand, and the final repayment of 500 thousand euros related to them will be made at the end of January. After this, operating profit and net profit should be approximately at the same level, as hardly any taxes on profit should be paid for a while due to previous losses.

R&D intangibles on the balance sheet are gradually decreasing, and the balance sheet is starting to be in very good shape. Accumulated losses are 4,852 thousand, which is slightly more than the total assets found on the balance sheet.

Operating cash flow should be quite good for the rest of the year, as a large portion of the cash flow will come into the cash account around the turn of the year. Last year, 1,032 thousand flowed into cash in the last quarter. Now, at the end of Q3, 180 thousand more is tied up in working capital than in the comparison period, so cash flow could be even better.