Itse pohdin tätä asiaa noin 3 vuotta sitten. Tuolloin Tokmanni ja Puuilo molemmat näyttivät halvalta. Ostin siis molempia varmuudeksi.

Nyt jälkikäteen katsottuna olisi ollut järkevää tankata vain jälkimmäistä. Heivasin omat ja vaimon Tokmannit 12€ kieppeillä ja ostin Puuiloa nouseviin kursseihin lisää.

Jos jatkossa tulee vastaava tilanne, niin pyrin ostamaan laadukkaampaa yhtiötä, vaikka se näyttäisi kalliimmalle.

Hyvää pohdintaa! Puuilon arvonmäärityksessä suurimmat kysymysmerkit tällä hetkellä lienevätkin kotimarkkinassa vääjäämättömästi lähestyvät kasvun rajat sekä kansainvälistymisen jokerikortti.

Mahtuuko näivettyvään Suomeen enää yhtää Puuiloa strategiakauden lopussa vuonna 2030, kun myymälöitä voi olla silloin jo yli 90? Tuskin enää kovin montaa, kun kilpailijatkin laajentavat koko ajan? Jos konseptia muutetaan vaikkapa pienempään myymäläkokoon kasvun jatkamiseksi, säilyykö kannattavuus/pääoman tuotot?

Miten Ruotsissa onnistutaan? Päästäänkö pilottimyymälöissä sellaiseen tuottoon, että sinne on mahdollisuus investoida arvoaluovasti Suomen myymälöiden tahkoamaa vuolasta rahavirtaa?

Jos kansainvälistyminen floppaa, on kasvun tyrehtyminen BKT:n tasolle vuosikymmenen vaihteessa mielestäni hyvin todennäköistä. Ehkä sitä voidaan hieman tästä jatkaa, mutta kannattavuuden tai pääoma tuottojen kustannuksella. Ei siinä, hyvää bisnestä silloinkin voidaan Suomessa tehdä, mutta kasvun tyrehtyminen näkyy varmasti arvostuksessa, eikä siinä varmasti ainakaan nousuvaraa olisi nykytasoilta.

Jos Ruotsiin laajentuminen onnistuukin, eikä siinä käy kuin hesulin pienyhtiöille tyypillisesti, on tilanne täysin toinen ja arvostuksessa voisi hyvinkin olla nousuvaraa. Tämän arviointi onkin sitten jokseenkin mahdotonta😄 ei auta kuin odottaa ja katsoa! Ruotsissa olisi varmasti kasvulatua taas seuraavat 10 vuotta

Tämä on hyvä nosto. Ongelmahan on se, että pääomantuotto mittarit ovat taaksepäin katsovia ja jos esimerkiksi Ruotsiin laajentuminen menee päin mäntyä niin noilla aikaisemmilla ROIC luvuilla voidaan nakata vesilintuja. Siitä meillä monella on ikäviä muistoja Kamuxin ja Talenomin tapauksissa. Suomessa kasvulatu on omissa papereissani samanlainen, eli noin 90 myymälää. Voi olla enemmän tai vähän vähemmän, mutta se ei mielestäni enää suurta kuvaa muuta.

Tässä vaiheessa kun Suomen markkina on täynnä “Puuiloa”, niin mielestäni nousee esille se kysymys kumpi on seuraavaksi mielekkäämpää pääomankäyttöä, kanavoidaanko pääomia Ruotsiin laajentumiseen vai päätetäänkö että ostetaan omia osakkeita (tai jaetaan tuotot osinkoina). Osakkeenomistajan kannalta se millä on korkeampi oletettu tuotto on parempi ratkaisu. Liikevaihdon lisääminen ei minun mielestä tuota mitään lisäarvoa, jos sitä tehdään kannattamattomasti (esim. Tokmanni). Näin ollen laajentuminen ei välttämättä ole hyvä ratkaisu. Mutta, haluan ainakin uskoa että Puuilo voisi laajentua onnistuneesti Ruotsiin ja luotan että johto tekee oikean päätöksen, heillä on toivottavasti paras näkemys asiaan.

Pilootti hanke kuulostaa omaan korvaani myös turvallisemmalta keinolta kokeilla asiaa sitoutumatta liian suuriin investointeihin. On mielestäni kuitenkin todennäköistä, että aluksi investointivaiheessa kannattavuus / investoinnin tuotto tulee olemaan heikompi Suomeen verrattuna, koska olettaisin että laajentumisessa ei päästä hyötymään samanlaisista synergioista kuin sillon kun avataan uusi myymälä Suomeen. Tämä varmasti myös heikentää yhtiön kannattavuutta.

Toistaiseksi Puuilo on kuitenkin onnistunut erinomaisesti ja haluan katsoa miten johto navigoi laajentumisen. Mutta kuten sanoit niin kukaan ei tässä vaiheessa osaa sanoa onnistuuko se vai ei, johto voi tehdä kaiken oikein mutta seuraavalla viikolla uusi kilpailija avaa naapuriin tai ihan mitä tahansa muuta voi sattua mikä ei ole yhtiöstä riippuvaa. Tärkeämpää on mielestäni seurata miten lähdetään laajentumaan, esim ostetaanko kiinteistöjä vai vuokrataanko, tehdäänkö yritysostoja jne… Eli paljonko pääomaa sitoutuu tähän laajentumiseen ja miten se vaikuttaa riskitasoon.

Tein saman virheen, mutta siinä vaiheessa kun möin Tokmannit en uskaltanut ostaa lisää Puuiloa koska kurssi tuntui kalliilta…olisiko Puuilo ollut silloin noin 8€. Huoh

Jep, iso ja riskinen yritysosto uudelta markkinalta olisi huomattavasti riskisempi, esimerkkinä vaikkapa juurikin Tokmannin Dollarstore😄 Pilotointi kuulostaa tosiaan siinä mielessä hyvälle, että rationaalisesti toimivalla johdolla pitäisi olla takaportti perääntyä Ruotsista, mikäli konsepti ei vain ota tuulta alleeen siellä ja pilottimyymälöissä ei saada riittävän hyviä tuottoja investointien jatkamisen perustelemiseksi. Sitten voidaan vaikka jakaa rahat omistajille, jota tosin tehdään jo nyt raskaasti, kun investointitarpeet ovat maltilliset kasvusta huolimatta.

Ei tainut nimittäin esimerkiksi Talenom aikoinaan puhua pilotoinnista Ruotsiin lähtiessään, vaan sinne mentiin isoilla suunnitelmilla raskaasti investoiden velkavivulla niin ohjelmistoihin kuin yritysostoihin. Hillotolpaksi asetettiin kotimarkkinalla saavutettu alan huippukannattavuus, jota ei ainakaan vielä ole saavutettu Ruotsissa (jos saavutetaan koskaan sen tarinan murentuessa) Tässä vaiheessa voi sitten olla hankala enää perääntyä kuin vasta aivan pakkoraossa, uponneiden kustannusten harhaa parhaimmillaan. Vähän sama tilanne Kamuxissa.

Mielestäni sijoittaja voi selvitä Puuilossa ihan kohtuullisen kuivin jaloin nykyisellä valuaatiolla, vaikka Ruotsi floppaisi ja sieltä peräännyttäisiin nopeasti sekä kotimarkkinalla bisnes rullaisi nykyisellään. Pakko oli tosin hieman kotiutella voittoja tässä vaiheessa siitä huolimatta.

Grafton on julkaissut alustavat luvut viime vuodelta. Grafton on päätynyt yhdistämään IKH:n luvut Alankomaan bisnekseen, jotta Suomen bisneksen heikkous saadaan piilotettua paremmin. Suomen ongelmana pidetään harvinaisen leutoa talvisäätä ja talouden heikkouden jatkumista.

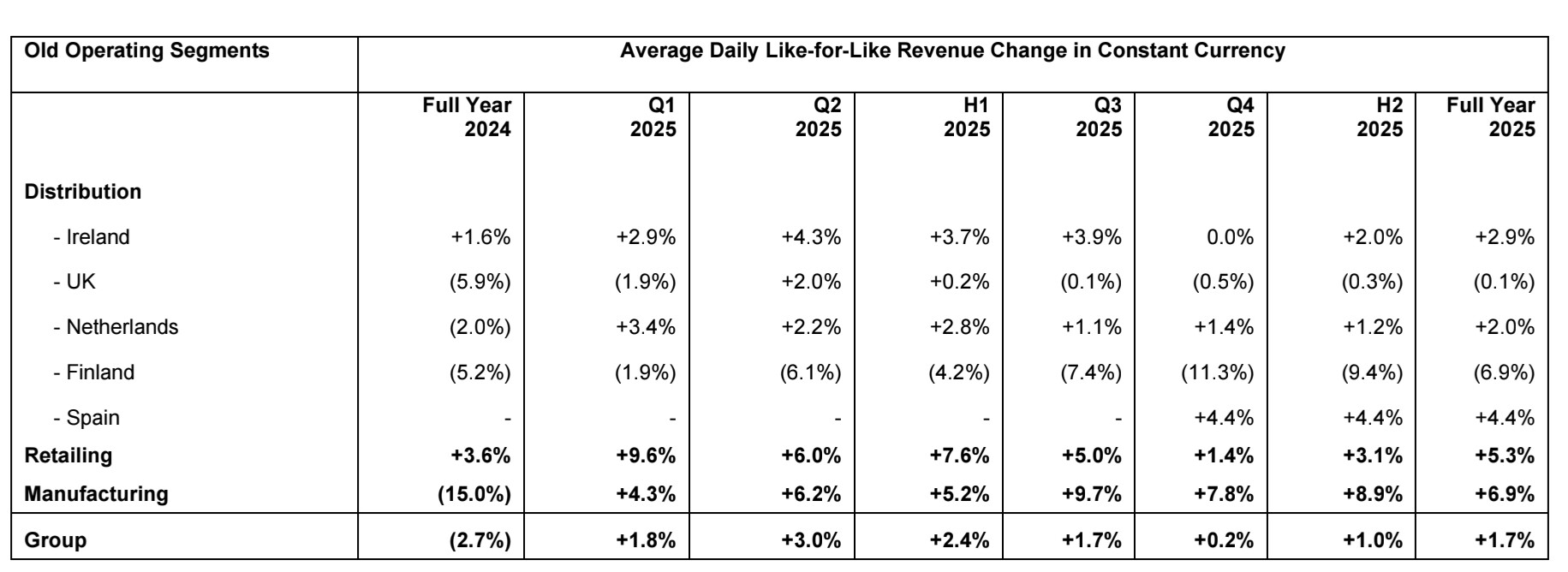

Average daily like-for-like revenue in Northern Europe declined by 0.5 per cent for the year and was down 2.9 per cent in the Period. Modest growth in the Netherlands, driven by strong project related sales, was more than offset by declines in Finland which reflected unusually mild winter weather and ongoing weakness in the economy.

Puuilo jatkaa kasvuaan ja avaa uuden myymälän syksyllä 2026 Raaseporiin, Karjaan Leppiin. Noin 3 000 m²:n kokoinen myymälä sijoittuu keskeiselle paikalle Karjaan K-raudan ja ABC-aseman naapuriin, kahden valtatien risteykseen. Samaan rakennukseen avataan myös Rusta. Avauksen yhteydessä myymälä työllistää 13–14 henkilöä, ja rekrytointi käynnistyy kesän 2026 aikana.

Tällä hetkellä lähin Puuilo-myymälä sijaitsee Lohjalla, mutta toimitusjohtaja Juha Saarela näkee Raaseporissa merkittävää potentiaalia: “Raasepori on meille luonteva laajentumiskohde. Alueella on paljon omakotiasujia ja mökkiläisiä, joita Puuilon valikoima palvelee erinomaisesti. Karjaa toimii alueellisena palvelukeskittymänä, ja uusi myymälä on helposti saavutettavissa kahden valtatien risteyskohdassa .”

Suurimmat kunnat ilman Puuilo-myymälää. Mukana ilmoitetut avaukset:

Turku 209 471

Nurmijärvi 45 265

Kangasala 34 320 (avataan syksyllä 2026)

Raasepori 26 926 (avataan syksyllä 2026)

Sipoo 22 934

Hollola 22 756 (avataan keväällä 2026)

Siilinjärvi 21 342

Pirkkala 21 256

Valkeakoski 20 845

Naantali 20 285

Mustasaari 19 766

Kempele 19 684

Pietarsaari 19 582

Kurikka 19 453

Kemi 19 337

Hamina 19 195

Jämsä 19 121

Laukaa 18 823

Pieksämäki 17 152

Akaa 16 347

Janakkala 15 903

Orimattila 15 554

Ylivieska 15 276 (avataan 2027)

Turun seudulla on kolme myymälää Raisiossa, Kaarinassa ja Liedossa. Uusia myymäläavauksia tulee varmaan myös pienempiin listan ulkopuolisiin kuntiin ja lisäksi kuntiin missä on jo Puuilo. Uusista myymäläavauksista on jo ilmoitettu Jyväskylään, Lahteen ja Espooseen, ja näitä tulee varmaan myös lisää.

Jos selaa taakse päin näitä myymälälistojani, niin huomaan “Turkuun ei tarvita Puuilo-myymälää” - kommentin lisäksi, että kovaa tahtia uusia myymälöitä on tehty vanhoihin listakuntiin.

Puuilo jatkaa myymäläverkostonsa kehittämistä uudistamalla Kajaanin myymälänsä. Nykyinen myymälärakennus on tullut käyttöikänsä päähän, eivätkä sen tilat enää vastaa Puuilon tämänhetkisiä tarpeita. Sijainti on kuitenkin todettu erinomaiseksi ja toimivaksi, minkä vuoksi täysin uusi, noin 3 000 m²:n kokoinen myymälä rakennetaan samalle tontille palvelemaan kasvavaa asiakaskuntaa. Rakennustyöt alkavat keväällä 2026 ja etenevät vaiheittain siten, että vanha myymälä jatkaa toimintaansa normaalisti uuden myymälän valmistumiseen saakka. Uusi myymälä avataan viimeistään kesällä 2027, ja sen valmistuttua vanha myymälärakennus tullaan purkamaan.

Motonetin toimitusjohtaja oli kertonut Arhin haastattelussa, että heillä oli ollut positiivinen loppuvuosi elokuusta 2025 alkaen ja että sama vauhti olisi jatkunut myös tänä vuonna.

Vielä Q3-raportin (elo-lokakuu) perusteella Puuilon kohdalla ei ollut samanlaista positiivista kuluttajan käännettä havaittavissa, sillä keskiostos oli edelleen laskussa.

Pitää kysellä Q4:n yhteydessä Juhan mietteitä kilpailijan näkemyksistä.

Puuilon pitkäaikainen ja erottuva markkinointi palkittiin Effien kärkisijoilla:

GRAND EFFIE EN. TUUN. Huumorista strategiaksi ja vakavasti otettaviin tuloksiin.

Puuilo & Filmo & WPP Media, Sherpa, OIKIO Digital Performance Agency, Bad agency, Klikattavaa

Tämä työ on noussut moderniksi benchmarkiksi suomalaisessa markkinoinnissa. Johdonmukainen, vähän pähkähullu ja kansanomainen tekeminen on rakentanut ikonisen brändin, jossa jokainen kampanja vahvistaa edellistä. Tuloksena on erottuva, hymyä herättävä ja kaupallisesti tehokas kokonaisuus, josta monen brändin kannattaisi ottaa oppia.

Bilteman myymäläverkoston laajentaminen jatkuu. Pari vuotta sitten putkessa oli 8 uutta myymälää, joista nyt 6 on avattu. Näiden kuuden avatun myymälän lisäksi putkessa on tällä hetkellä ainakin 6 uutta myymälää.

Samalla kun odotamme tilinpäätöstiedotetta (julkaistaan 25.3.), huomasin että puuilo.se sivustolta näyttää poistuneen Ruotsin maajohtajan hakuilmoitus. Mahdollisesti siis löytynyt maajohtaja..