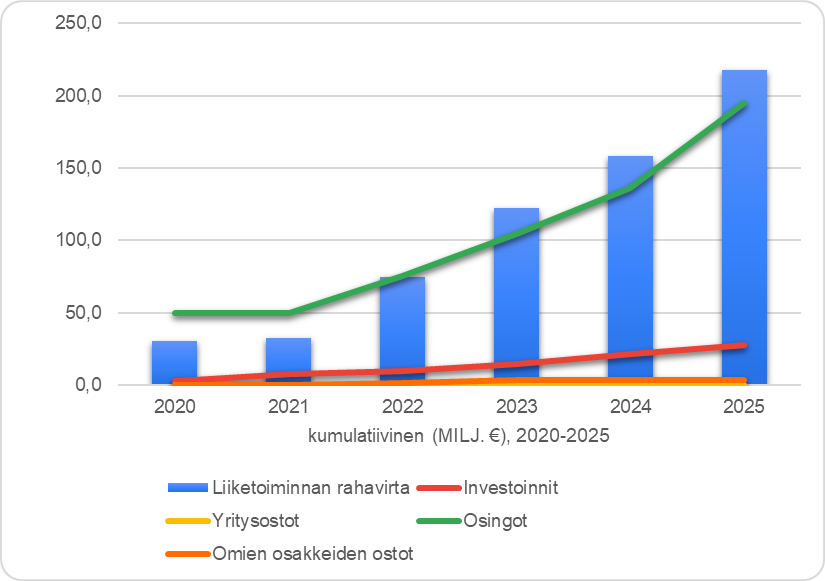

Puuilo’s capital allocation is certainly interesting. The company grows organically at a rapid pace year after year, but it doesn’t need to invest much at all ![]() If one looks at the operating cash flow and capital allocation, e.g., from 2020-2025, the company has cumulatively paid back 90% of its operating cash flow to shareholders in the form of dividends. Investments, by contrast, have only accounted for 13% cumulatively over the same period! I tried to visualize this a bit in a chart:

If one looks at the operating cash flow and capital allocation, e.g., from 2020-2025, the company has cumulatively paid back 90% of its operating cash flow to shareholders in the form of dividends. Investments, by contrast, have only accounted for 13% cumulatively over the same period! I tried to visualize this a bit in a chart:

Note: Lease liability payments have been deducted from operating cash flow.

| From Operating Cash Flow 2021-2025 | |

|---|---|

| To Investments | 13 % |

| To Acquisitions | 0 % |

| To Dividends | 90 % |

| To Share Repurchases | 2 % |

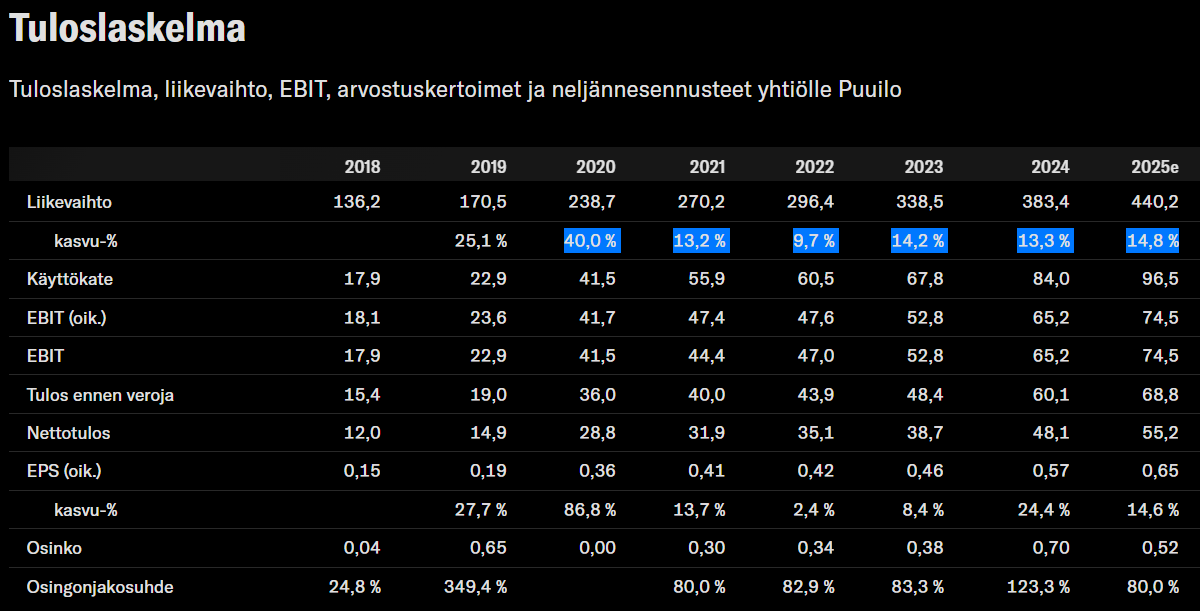

This is indeed a somewhat rare combination of growth and dividends ![]() And why not? There’s no need to invest any more of that cash flow if the company can achieve such a return on capital employed (ROCE) of about 30% by carefully selecting suitable store locations, etc., and still grow significantly even in bad times

And why not? There’s no need to invest any more of that cash flow if the company can achieve such a return on capital employed (ROCE) of about 30% by carefully selecting suitable store locations, etc., and still grow significantly even in bad times ![]()

Usually, I’m always complaining in company threads when capital is allocated to dividend payments when there could be better uses for it, but in Puuilo’s case, I’m not complaining ![]() If a company can grow with such small investments and so profitably, but has a very limited runway left in its domestic market, then by all means, the money should go to shareholders rather than, say, going the Tokmanni route and buying some giant chain abroad

If a company can grow with such small investments and so profitably, but has a very limited runway left in its domestic market, then by all means, the money should go to shareholders rather than, say, going the Tokmanni route and buying some giant chain abroad ![]()

At the same time, it can quietly test its concept selectively abroad with “pocket money,” in case it can grow there someday. So, the company is in no hurry whatsoever, and there’s no need to flash any wild visions of conquering the world, or in this case, the Nordics, on strategy slides ![]()