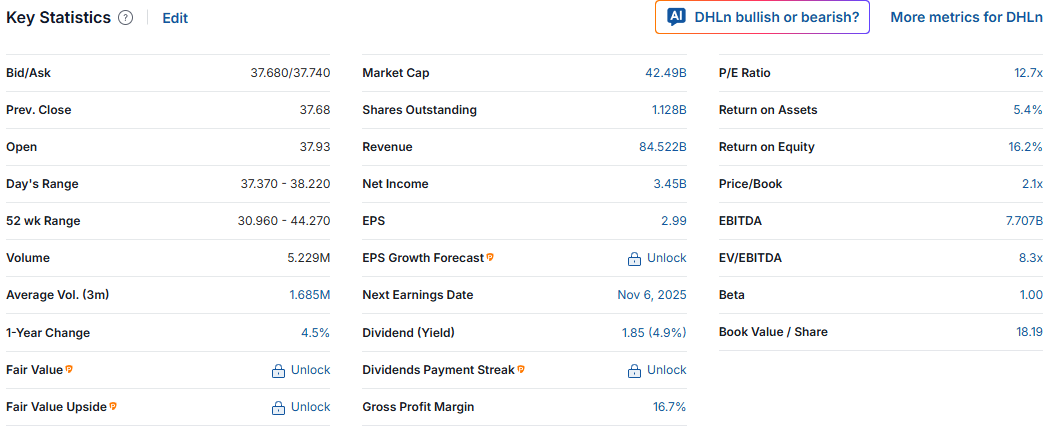

The German Post has developed surprisingly positively.

The return on capital seems to be at a quite good level for generating shareholder value. The stock’s valuation feels rather moderate.

The German Post has developed surprisingly positively.

The return on capital seems to be at a quite good level for generating shareholder value. The stock’s valuation feels rather moderate.

A few things to consider:

In Finland, official letters will transition to digital in 2026. The phasing out of letter mail will gain new momentum (the majority of current letter mail is official mail). As a result, letter delivery will likely become structurally unprofitable. Who will cover these losses (Posti or the state as a delivery subsidy for letter mail to Posti) has not been disclosed. This is of great significance. Alternatively, letter mail delivery could, of course, be discontinued to cut losses. The downside then is that half of Finland would no longer receive their online purchases at home but would have to pick them up from a local store 20 km away in remote areas, etc.

Was Posti’s result “forced” significantly into the black last year with an IPO in mind, and will it return to a poorer, more normal level in the coming years? There is no visibility on this from the Inderes discussion forum; we cannot see the company’s internal decisions that affected the accounting.

As a comparison: Altia was largely brought to the stock exchange as a dividend story. For example, a Nordea analyst raved that the company was worth at least over 10 euros. Well, contrary to expectations, Altia’s, now Anora’s, revenue then began to shrink, and a tough competitive situation started. The current share price of 3 euros is, with current information, justified for Anora. A dividend story during an IPO cannot always be trusted.

In my opinion, Posti’s automated network is superior; I always use it if possible. I don’t use foreign courier services; they arrive unannounced at the locked main door of an apartment building in the middle of the workday, don’t call, and then take the package 10 km away to some gas station for pickup. Posti has a competitive advantage here.

I must also comment on delivery problems: You’d be surprised if you saw how poorly people write address information on letters. For example, the street address Kauppiaskatu 17 F 215 might be written as Kauppiaskatu 17. Then the sender or recipient blames the postman/Posti for not being able to guess which of the building’s 250 mailboxes it was. I have investigated a large number of such situations over 20 years (I am not a Posti employee). The resident’s answer is usually: “I use my smartphone’s automatic address autofill for my online orders, I didn’t notice that some of the information was wrong.” So, it’s the customer’s error, but they still blame Posti. Another common reason is that one digit in the phone number is wrong, and therefore the arrival notification disappears into cyberspace… No more on this, but when investigating problems, the reasons behind them can be surprising. Of course, errors also occur.

Deutsche Post is a bit of a different animal compared to our Posti; it’s a huge global logistics giant. Posti, on the other hand, is much more smaller-scale and local, although changes have also been made there in the same direction, but the difference in scale is absolutely enormous.

Of course, there has already been some reduction in official mail, as customers have been directed to use Suomi.fi or, in healthcare, Maisa, which is much more convenient.

This is indeed a question that concerns me somewhat. Hopefully, answers will emerge as the offering progresses.

Altia’s market is melting away as people no longer buy strong alcoholic beverages in the same way as before. Which, in the bigger picture, is a good thing. I can’t say how visible that was at the time of the IPO.

Exactly the same experiences.

It’s not that different based on 2024 figures. Short-term assets are roughly the same amount relative to the balance sheet total. Posti generated slightly more revenue relative to the balance sheet total than DHL, but Posti’s operational profitability is then slightly worse. Return on equity was then roughly at the same level.

DHL / Posti

Short-term assets / Balance Sheet Total

28.7 / 27.4

Revenue / Balance Sheet Total

1.20 / 1.33

Operating profit, %

7.75 / 4.47

ROE, %

14.7 / 15.5 %

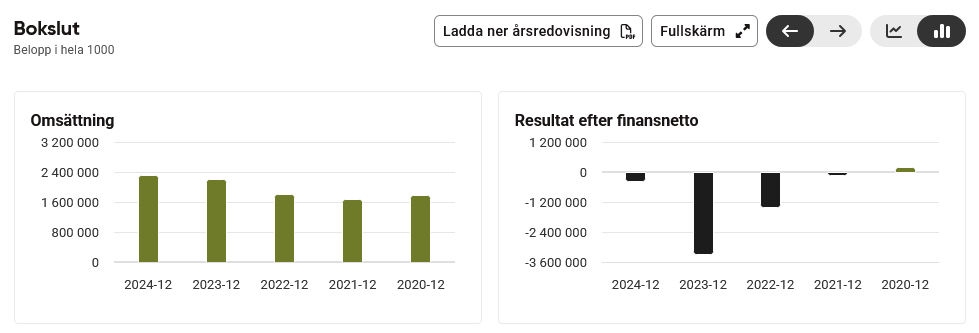

The current year, however, seems to be significantly weaker for Posti in terms of operating profit compared to the reference period.

I have to agree with this. Posti’s luck is that UPS’s service in Finland is, at least for consumer customers, absolutely terrible. The only downside of parcel lockers is that they are often full, meaning they are victims of their own popularity.

This will likely require quite significant commitments from the anchor investors. One would think that anchor investors would include, for example, pension insurers, but it would be desirable if the list also included entities investing their own money. The price will probably be pushed down during the listing, to ensure a successful listing, some return for the anchor investors, and dividends for the public next spring.

The state would need to use some legislation to smoke out foreign low-cost carriers and make the postal cartel flourish.

If I think from my own perspective as an investor, the most fascinating thing about Posti’s IPO would be that it is a national company forced to renew itself due to the growth of e-commerce and the disruption in logistics. An IPO could bring much-needed drive and competitive pressure from international rivals.

On the other hand, I am cautious about the fact that Posti’s strong state ownership and political steering could hinder purely business-driven decision-making. Furthermore, the logistics sector is already very competitive and margins are thin.

So, my take: an interesting case to follow, but for an investment decision, one would need to see the pricing (at what valuation multiples Posti would enter the market) and the strategy (how credibly it can transform from a letter logistics company into a growth company in parcel traffic and delivery).

According to Helsingin Sanomat, Posti would be coming to the Stock Exchange with a market value of 300 m€.

Thoughts on the valuation? Would the EV/EBITDA then be around 2.7 with these figures.. sounds reasonable even if the business were to suffer a small contraction..

Sounds reasonable, but a million shares only for private investors. It will surely be oversubscribed, and that will give it a brisk start when the gates open as free trading begins.

There are indeed many articles in the newspapers, but no brochures seem to be available. An interesting listing, but I’ll have to wait for more detailed information.

I teased the AI with 2024 actual figures and today’s published market cap of 300 million, and compared it to the 400 million I previously used in that interpretation.

Starting Data (2024 Actuals)

• Revenue: 1,521 M€

• Adjusted EBITDA: 208 M€

• Adjusted EBIT: 80 M€

• Net Debt: 258 M€

• Market Cap: 300 M€

• EV = 300 + 258 = 558 M€

![]() Valuation Multiples (with 300 M€ market cap)

Valuation Multiples (with 300 M€ market cap)

Multiples Calculation Result

EV / Revenue 558 / 1,521 0.37x

EV / EBITDA 558 / 208 2.68x

EV / EBIT 558 / 80 7.0x

P/E (adjusted) 300 / (80 × 0.75 ≈ 60) 5.0x

![]() Interpretation

Interpretation

• EV/EBITDA 2.7x → very low, clearly below international logistics companies (typically 5–8x).

• EV/EBIT 7x → still low, but closer to a “neutral” level.

• P/E 5x → the market prices Posti’s earnings very cautiously, which suggests either structural risks or weak growth expectations.

• EV/Revenue 0.37x → essentially, the market pays only a third of revenue, which is a truly low level.

![]() This calculation confirms that if Posti’s market cap were 300 M€, the company would appear even more undervalued relative to international peers like DHL.

This calculation confirms that if Posti’s market cap were 300 M€, the company would appear even more undervalued relative to international peers like DHL.

How do you get from an adjusted operating profit of €80 million to an adjusted net profit of approximately €60 million? Surely taxes and interest expenses would be much higher if, according to your calculation, net debt is also €258 million? In addition, Posti has estimated this year’s adjusted operating profit to be €65-75 million. EV/EBIT (adj) could therefore be around 8 if EV is €558 million at the IPO.

Perhaps the adjusted net profit could be €45-48 million and P/E then somewhere around 6-6.5. I haven’t delved into the numbers myself yet, so it’s only based on what’s been seen in this thread.

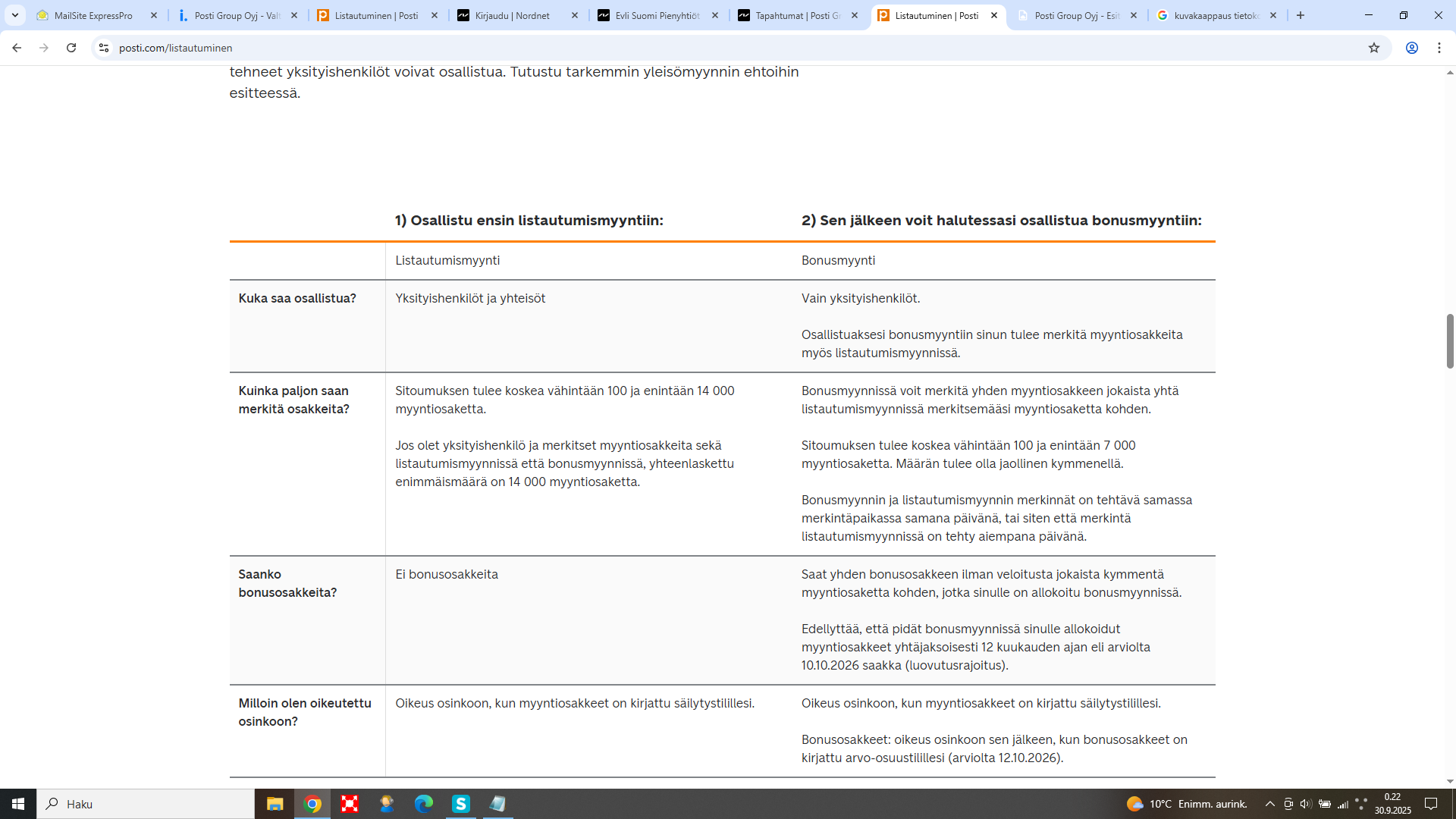

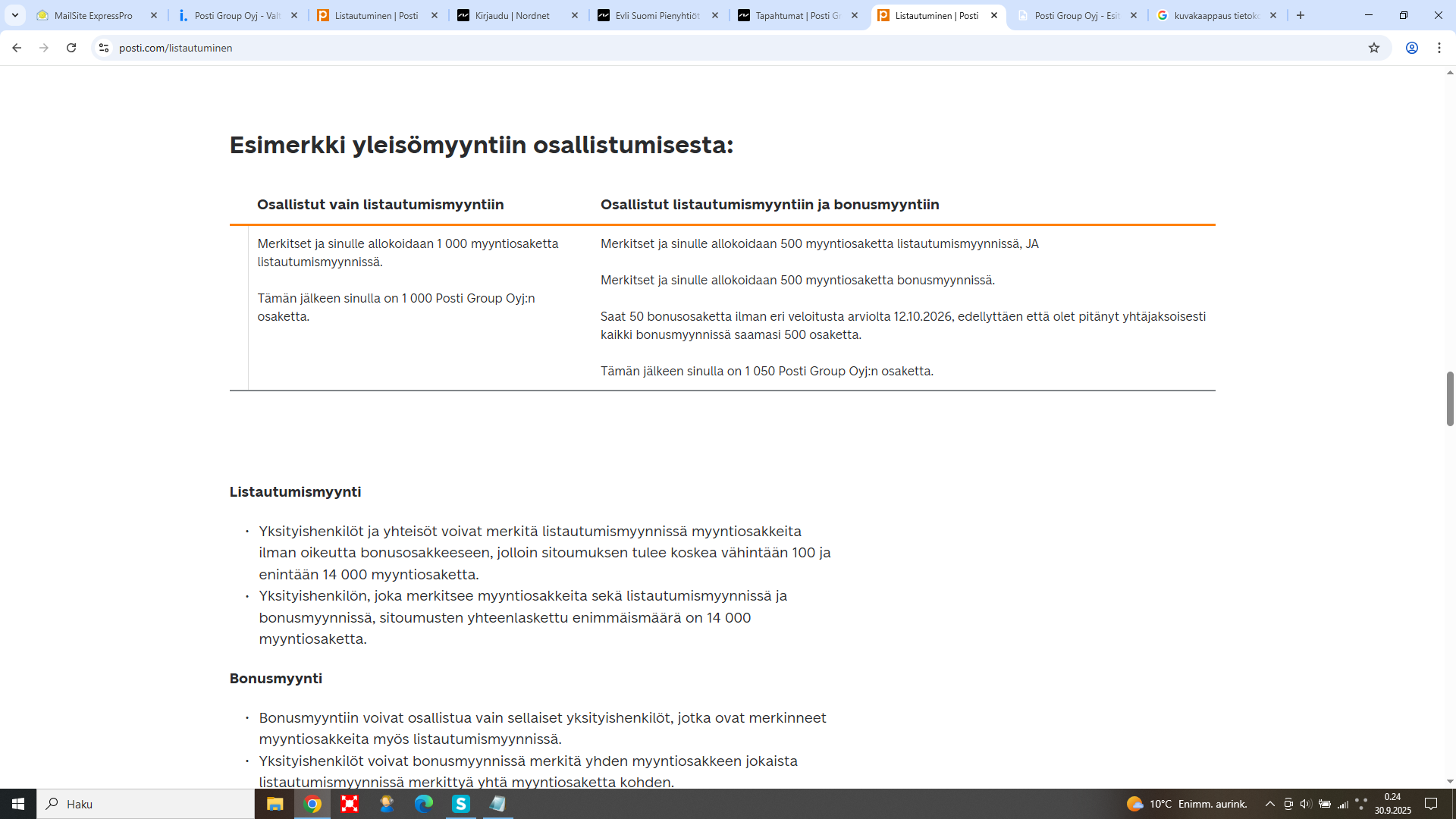

Bonus shares will be realized! Receiving bonus shares requires holding the shares obtained from the offering for one year, approximately until 10.10.2026

| 1) First, participate in the IPO sale: | 2) After that, you can participate in the bonus sale if you wish: | |

|---|---|---|

| IPO Sale | Bonus Sale | |

| Who can participate? | Individuals and entities | Only individuals. |

Sorry for the poor computer skills, the whole story: Listautuminen | Posti

IPO Prospectus: https://assets.ctfassets.net/1v32pqxqm0al/181j6a2jRuZcsMnw3lJ7uL/c6d8a78524a8920e8bb87d01ad492b4d/Posti_Group_Oyj_-_Esite_-_29.9.2025.pdf

I didn’t actually check those figures at all. I asked to use the 2024 financial statements and assumed it would be done as instructed.

Edit; new question

Now we have precise figures from Posti’s 2024 financial statements. Let’s look at the reported net profit to calculate P/E and other key ratios without assumptions:

![]() Posti Group 2024 (Financial Statement Release)

Posti Group 2024 (Financial Statement Release)

• Revenue: €1,521.4 M

• Adjusted EBITDA: €207.6 M

• Adjusted EBIT: €80.1 M

• Reported EBIT: €68.0 M

• Net Profit: €47.0 M (reported in financial statements) A

• Net Debt: €258 M

![]() Valuation Multiples (Market Cap €300 M)

Valuation Multiples (Market Cap €300 M)

• EV = 300 + 258 = €558 M

• EV/Revenue = 558 / 1,521 = 0.37x

• EV/EBITDA = 558 / 207.6 = 2.7x

• EV/EBIT (adjusted) = 558 / 80.1 = 7.0x

• EV/EBIT (reported) = 558 / 68.0 = 8.2x

• P/E = 300 / 47 = 6.4x

Conclusion

• Posti’s net profit in 2024 was €47 M, which confirms that the previous 25% tax assumption (EBIT 80 → net profit €60 M) was slightly optimistic.

And with 2025 H1 figures

Good Tero, let’s take the calculations based on Posti’s January–March 2025 interim report A B.

![]() Posti Group Q1/2025 (Interim Report)

Posti Group Q1/2025 (Interim Report)

• Revenue: €357.1 M (–6.5% y/y)

• Adjusted EBITDA: €42.5 M (11.9% of revenue)

• Adjusted EBIT: €10.5 M (3.0% of revenue)

• Reported EBIT: €5.0 M

• Profit for the period: –€0.2 M (loss-making)

• Net Debt: €454 M (increased from €258 M to €454 M due to extraordinary dividend and investments)

![]() Valuation Multiples (Q1/2025 Annualized)

Valuation Multiples (Q1/2025 Annualized)

If Q1 figures are scaled for the full year (indicative only, as Posti’s business is seasonal):

• Revenue (annualized) ≈ 357.1 × 4 = €1,428 M

• Adjusted EBITDA (annualized) ≈ 42.5 × 4 = €170 M

• Adjusted EBIT (annualized) ≈ 10.5 × 4 = €42 M

• Net Profit (annualized) ≈ –0.2 × 4 = –€1 M

![]() Valuation Multiples (Market Cap €300 M)

Valuation Multiples (Market Cap €300 M)

• EV = 300 + 454 = €754 M

• EV/Revenue = 754 / 1,428 ≈ 0.53x

• EV/EBITDA = 754 / 170 ≈ 4.4x

• EV/EBIT = 754 / 42 ≈ 18.0x

• P/E = 300 / (–1) → not meaningful, as profit is negative

Conclusion

• Based on the Q1/2025 interim report, Posti’s profitability clearly weakened: EBIT margin only 3% and net profit negative.

• Net debt increased to €454 M, which raises EV and multiples.

• EV/EBITDA has risen to the 4–5x level (closer to international peers), but this is more due to weakening results and increased debt than improved valuation.

• EV/EBIT is already 18–20x, which is a high level with such low earnings.

• In practice, the market continues to price Posti cautiously, but the weakening balance sheet and drop in earnings make the multiples less attractive than with the good figures of 2024.

You can subscribe through Nordnet, but also through Nordea and Danske. The subscription starts at 10:00 AM. All this information can be found on Posti’s website ![]()

There don’t seem to be anchor investors, or did I miss that part? If so, should this be interpreted as a bad, good, or neutral thing? ![]()

Was it that OST cannot mark? But it must be AOT.

You can also subscribe for an OST (at least in Nordnet and Nordea). It’s worth reading the materials and the Q&A: