https://twitter.com/FirstSquawk/status/1252536946854785024?s=20

4 tykkäystä

@Geweth ;n ja Vernerin Kiina-keskustelu on hypnoottista luettavaa - perustakaa ihmeessä se Kiina-palsta!

8 tykkäystä

Minäpäs väsään. Hetki vain ![]()

4 tykkäystä

Ketju avattu lyhyellä alustuksella Kiinan talouden tulevaisuus

9 tykkäystä

Euroopassa on niin vahvat instituutiot että muutamia poikkeuksia lukuunottamatta (Puola, Unkari) maanosa on kestänyt vuosikymmenen kitukasvua ja taloudellista stagnaatiota ilman isompia kriisejä tai hajoamista (euroalueen hajoamista saa jännittää, EU:n ei niinkään tai yksittäisten maiden.

Unkarissa avoimesti antisemitistinen Jobbik sai viime vaaleissa 19 prosentin kannatuksen.

Ruotsidemokraattienkin kannatus taitaa olla yli 20 prosenttia, vaikakkin käsitykseni mukaan ovat huomattavasti maltillisempia kuin vaikka Itä-Euroopan verrokit.

Saksassa, ehkä Euroopan liberaaleimmassa maassa, useissa osavaltioissa populistinen AfD sai myös 20 prosentin kannatuksen.

Olet ihan oikeassa siinä, että varsinkin Länsi-Euroopassa demokratia on hyvin juurtunut, enkä usko mihinkään radikaaliin suunnanmuutokseen. Ongelmallista on, että nämä Itä-Euroopan maat ravistelevat EU:ta liitoksistaan. Riittääkö, että Unkarin rahahanat laitetaan kiinni? Mitä jos EU hajuaa?

En halua olla turhan pessimistinen, mutta mielestäni kansainvälisessä järjestelmässä on meneillään suurin murros sitten toisen maailmansodan.

Mutta kuinka tuottavia nuo investoinnit ovat? Kiinan tuottavuuden kasvu on heikentynyt merkittävästi viime vuosina. Kiinan talouskasvumalli on investointivetoinen, ja aiheellinen huoli nousee siitä kaataako maa rahaa heikosti tuottaviin projekteihin niin kotimaassa kuin alati enemmän ulkomaille.

Haluatko avata, mitä gradussa käsittelet tarkemmin Kiinasta?

Kiinasta riittää kyllä aineiksia aiheeseen kuin aiheeseen.

Tutkin siis Kiinan investointeja Euroopan unionin alueelle strategisesta näkökulmasta, eli mennään valta, ei ROI edellä. Tosin aikaisemmin mainitsemassani Pireuksen satamassa konttiliikenne olisi COSCO:n mukaan nelinkertaistunut omistajanvaihdoksen jälkeen finanssikriisin jälkimainingeissa. En tiedä sitten miten pitää paikkaansa.

Toinen ääripää on sitten nämä Suomeen suunnitteilla olevat hankkeet. Virkamiesselvityksen mukaan Jäämeren rata tai Tallinna-tunneli eivät ole kaupallisesti kannattavia. Näihin on kuitenkin löytynyt rahaa Kiinan valtioon kytköksissä olevilta rahoituslaitoksilta. Niin mikä se motiivi sitten olikaan?

En tietty osaa sanoa, kuinka kauan tällaisia projekteja voidaan rahoittaa ilman suurempia ongelmia.

Pari tutkijaa on myös selvittänyt Huawein omistusrakenteita, ja todenneet mediassa esillä olleen Ren Zhenghein omistavan noin prosentin firmasta. Loput 99 prosenttia omistaa trade union committee, josta ei sitten oikeastaan tiedetä mitään. Perinteisesti tällaiset instituutiot on ollut kommunistisen puolueen hallinnassa.

16 tykkäystä

Aivan fantasista keskustelua ja analysointia ! Tämän takia tätä foorumia luen.

Kiitos @Geweth & @Verneri_Pulkkinen ym. kun avasitte asioita ja annoitte mielipiteitä. Mielenkiintoinen aihe todella, itse aloittelen myös gradua, mutta kauppiksen puolella ja minulla olisi suuri mielenkiinto kohdistaa tutkimukseni Kiinalaisten toimiin länsimaissa ja miten he ovat infiltroituneet / tulevat infiltroitumaan tulevaisuudessa. Onko tämä hetken trendi vai ‘‘Kiinalaistuuko’’ koko länsimaalainen liiketoiminta. ?

9 tykkäystä

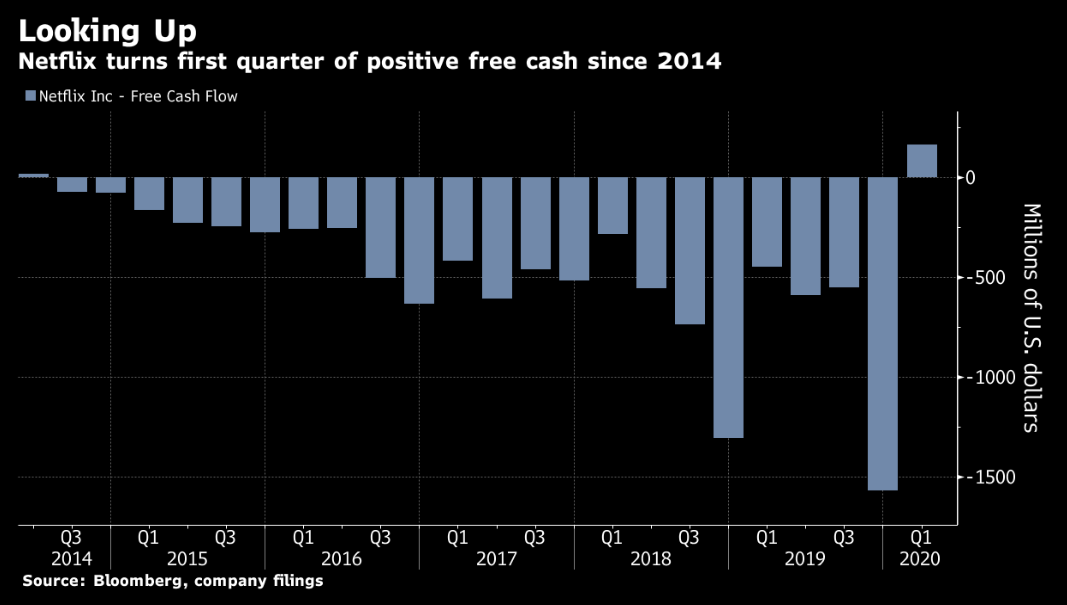

Netflixille koronavirus-boostia tilaajamäärissä.

Numeroiden osalta normisettiä

For the just-ended quarter, Netflix’s earnings per share fell short of analyst expectations. The company posted diluted earnings per share of $1.57, below the $1.65 consensus, according to IBES data from Refinitiv.

Total revenue rose to $5.77 billion from $4.52 billion. Analysts on average had expected $5.76 billion.

Appreciation of the U.S. dollar, due partially to the coronavirus crisis, dragged on international revenue, the company said.

04/21/2020 07:31pm EDT

3 tykkäystä

Kiitos jakamisesta, olin juuri itsekin laittamassa Netflixistä juttua ![]()

Oli siellä numeroissa yksi “anomalia”: positiivinen vapaa kassavirta!

Tuotantomenot alhaalla kun ei voi kuvata, samalla kun kassavirta on mehevää tilaajilta. Vuoden 2020 tuotanto on kuitenkin jo purkissa, eli heti ei repertuaariin tule osumaa koronan takia.

15 tykkäystä

Hubein maakunnan BKT laski 39 % Q1’2020.

Siitä saa hieman osviittaa minkälainen osuma tulee kun kokonainen alue/maa on karanteenissa.

Tietysti myös Euroopassa maiden sisällä alueelliset erot ovat todnäk isoja, mutta nuo -20 - 30 % ennusteet Q2:lle eivät Hubein valossa vaikuta lainkaan epärealistisilta.

13 tykkäystä

Helsingin pörssin ”parhaat” TINA-kaverit KONE ja Elisa molemmat lähellä ATH:ta kun maailma ei koronaan niiden osalta loppunut(kaan) kuten tuloskaudella on käynyt ilmi.

15 tykkäystä

Keskiviikkona jatkui myös tuloskausi. Toistaiseksi 84 yritystä S&P 500-listalta on ilmoittanut tuloksensa, joka on 67 prosentilla yrityksistä ollut analyytikoiden ennusteita parempi.

Toivottavasti pysytään tässä tahdissa, koska pahin on vasta edessä talouslukujen osalta…

edit:

https://twitter.com/Fxhedgers/status/1253190657566371840?s=20

saa nähä puhuuko totta ![]()

4 tykkäystä

Eiköhän Q2 tulokset tule olemaan rumempia ja siihen mennessä alkaa sitten erottumaan jyviä akanoista - jotkut firmat tulevat ajamaan kovaa kiville, toisille koko soppa on vain pieni töyssy.

Lisäksi on kysymysmerkki kuinka pitkään keskuspankkien INFIIINITEE POWER -linja pysyy. kannattelemassa pörssikursseja.

2 tykkäystä

Ei varmaan lyhyellä aikavälillä edes väliä, puhuuko. Jos totuus Q3:sta alkaa paljastua vasta Q3:n ollessa käsillä, markkina malttanee katsoa jo 6-12 kuukauden päähän taas. Saatetaan nollailla nousuja tarpeen mukaan, mutta tuskin mitään isompaa.

Mutta onhan kasvu helppoa 2021 jos 2020 ollaan melkein seis. Niinkin, että mitä enemmän turpaan otetaan nyt, sitä varmemmin kasvu on ensi vuonna vahvaa.

Tämähän on suorastaan perverssiä ajattelua. ![]()

18 tykkäystä

Mutta mahtavaa, olen täysin samaa mieltä kanssasi. ![]()

Jos markkinoilla aiotaan nähdä aiempien pohjien testaamista, on sen mielestäni tapahduttava nyt kesällä. Aikatekijä on bullien puolella.

Tämä tosin sillä olettamuksella ettei koronakriisi muuntaudu vakavaksi finanssikriisiksi. Ja toisaalta rokote on kansainvälisesti saatavilla noin 6-9 kk päästä.

Edit: sen verran lisään etten siis itsekään usko täysin V muotoiseen markkinan toipumiseen. Sitä nykyisellään pidän kuitenkin mahdollisena että pohjat olisi jo tehty. Sen verran paljon nuo keskuspankkien toimet ovat muuttaneet peliä.

6 tykkäystä

Itse odotan vielä lähtökohtaisesti notkahdusta, mutta Q1 tuloskausi on tähän mennessä ollut sen verran vahvaa että on ihan realismia että vaikka Q2 tulokset tulevat olemaan rumia, jos virusrintamalla ei tapahdu pahaa takapakkia, voi markkina “paperoida yli” Q2-notkon ja katsoa jo pitkälle ensi vuoteen ja näin kurssireaktiot väistämättömästi tulossa oleviin Q2-punoituksiin voi olla hyvin maltillinen.

Tosin firmasta toiseen erot voivat olla hyvin suuria. Ne firmat jotka osoittavat että bisnekset eivät kaadu Koronaan rallattelevat ja ne joiden bisneksiin homma iskee suuresti ottavat osumaa. Sitä osakepoimijoiden kulta-aikaa…

9 tykkäystä

Uskon myös, että ennen Q2 julkkareita on laskupainetta, mutta julkkarin jälkeen voidaan korjata jopa ylöspäin, jos uskotaan pahimman olevan jo takana. Varmuudella tietää vasta silloin miltä silloin näyttää.

Pidemmällä aikavälillä pyllystä voi puraista ns. “rallatteluolettama”, mikä koskee liian laajalti hyviksi uskottuja yhtiöitä ja sellaisia, joiden ajateltiin hyötyvän koronasta. Nyt ATH-hinnoissa olevilla ei paljon nousuvaraa luulisi olevan edes silloin, jos kaikki menee suhteellisen nopeasti ohi. Jos kaikki ovat sitä mieltä, että Netflix on paras hevonen, niin kyllä se on aika varmasti täyteen ostettu. ![]()

Edes TINA ja arvostuskertoimien venyminen ei nostane näitä ylös merkittävästi hetkeen, kun vieressä on tulostuotoltaan paremmilta vaikuttavia osakkeita.

1 tykkäys

ei vaikutusta

![]()

5 tykkäystä

Noh noh, kyllä se DAX on tuon jälkeen dipannut ainakin 5 pistettä… eikun nyt jo melkeen kymmenen ![]()

Avauksessahan tuon sitten näkee, nämä futuurien pre-market heilunnat ovat aina välillä vähän hämyjä ja tuntuvat jopa enemmän position pelaamiselta avaukseen. No, ainakin tällä hetkellä näyttäisi flatilta tai lievästi positiiviselta avaukselta. Heti avauksesta voi tietty dipata mutta en ainakaan vielä usko että se on pysyvämpi vaan hetkellinen niiaus.

1 tykkäys

Kysyin edellä projektiivisia näkemyksiänne muiden toimijoiden pandemiaoletuksesta ( ja viitekehys huomioiden moni varmaan mielsi juuri suhteessa kurssitasoihin.) En osannut kuvaa tähän siirtää.

Kiitos vastauksistanne. Mäkilegendaa mukaillen sixty-fifty tulos. Yritin jatkotyöstää tulosta matriisina, jossa on toisella akselilla optimistinen vs pessimistinen pandemianäkemys. Toisella akselilla tämän hetken kurssitason vahva vs heikko kytky reaalitalouden näkymiin. Ajattelen tässä lähikuukausia.

Jos kytky on vahva ja oletus optimistinen on vaikea nähdä nousuvaraa, kun huomioi tämän hetken kurssitason verrattuna vaikka vuoden takaiseen. Ajatukseni on, että kaikki realistiset positiiviset uutiset on jo priced in.

Jos pessimistinen näkemys olisi priced in ja kytky vahva, niin nousupotentiaalia voisi tuoda vain todellinen game changer: “ihmelääke”, toimivaksi osoitettu rokote ennätysajassa tai pandemian sammuminen oleellisesti ennakoitua nopeammin tai vaikka Ruotsin mallin osoittautuminen menestykseksi.

Toinen rivi menee maallikolle vaikeaksi. Mielestäni heikkoon kytkyyn on selvät viitteet. Mitkä tekijät sen aiheuttavat ja kauanko ne vaikuttavat? Heikko kytky ei voine jatkua kuin rajallisen ajan? Em. suhteuttaminen optimistiseen tai pessimistiseen pandemiaoletukseen voi olla tehtävissä, mutta menee itselle “sumeaksi”. Jos pandemia “kuivuu” ehtyvätkö myös massiivisimmat tukitoimet ja jos jatkuvat, niin missä muodossa? Minkälaisia vinoumia voi syntyä?

Markkinoille asteittain tuloa suunnittevalle lähinnä indeksirahastoilla operoivalle kaikki kohdat johtavat siihen, että wait and see on perusteltua toistaiseksi.

1 tykkäys

Katselen välillä Traders Clubin jaksoi ja tässä Lepiköltä keskuspankkeihin nojaavaa argumentaatiota, miksi voitaisiin tehdä uudet huiput pörsseissä (SP500 oli varmaankin mielessä…) tänä vuonna, kun korkoraha valuu osakkeisiin ja printterit laulaa.

Sinänsä huvittavan paljon samoja pointteja näissä ja Melkein minuutissa jaksoissa on, sillä erolla etten itse puhu TA:sta eikä Melkein minuuttissa videoissa oteta varsinaisesti mitään markkinanäkemystä, vaan tuomaan esiin eri kulmia mistä sijoittaja voi sitten itse pureskella omansa.

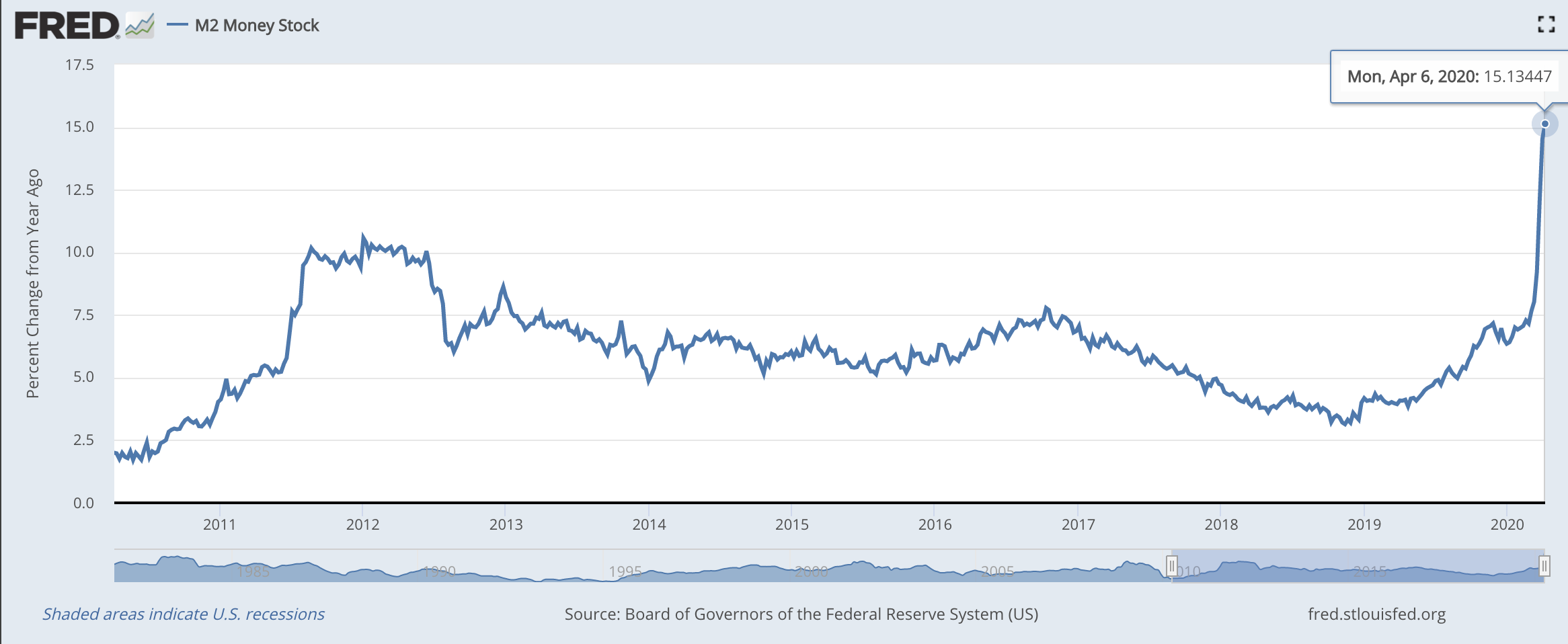

Päivän poimintoja:

M2-rahan paisuminen jatkuu jenkeissä:

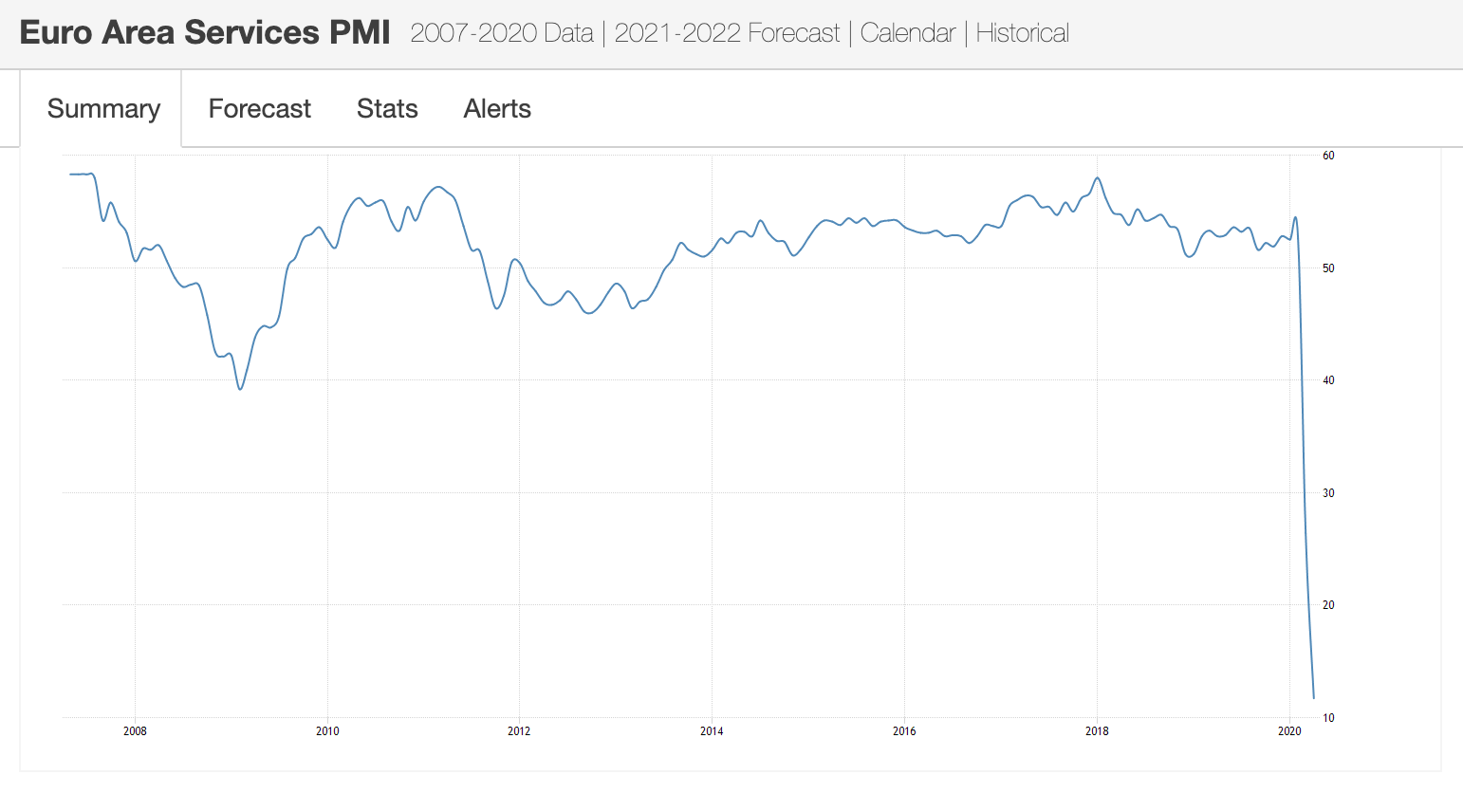

Euroopan palvelut is no more:

31 tykkäystä