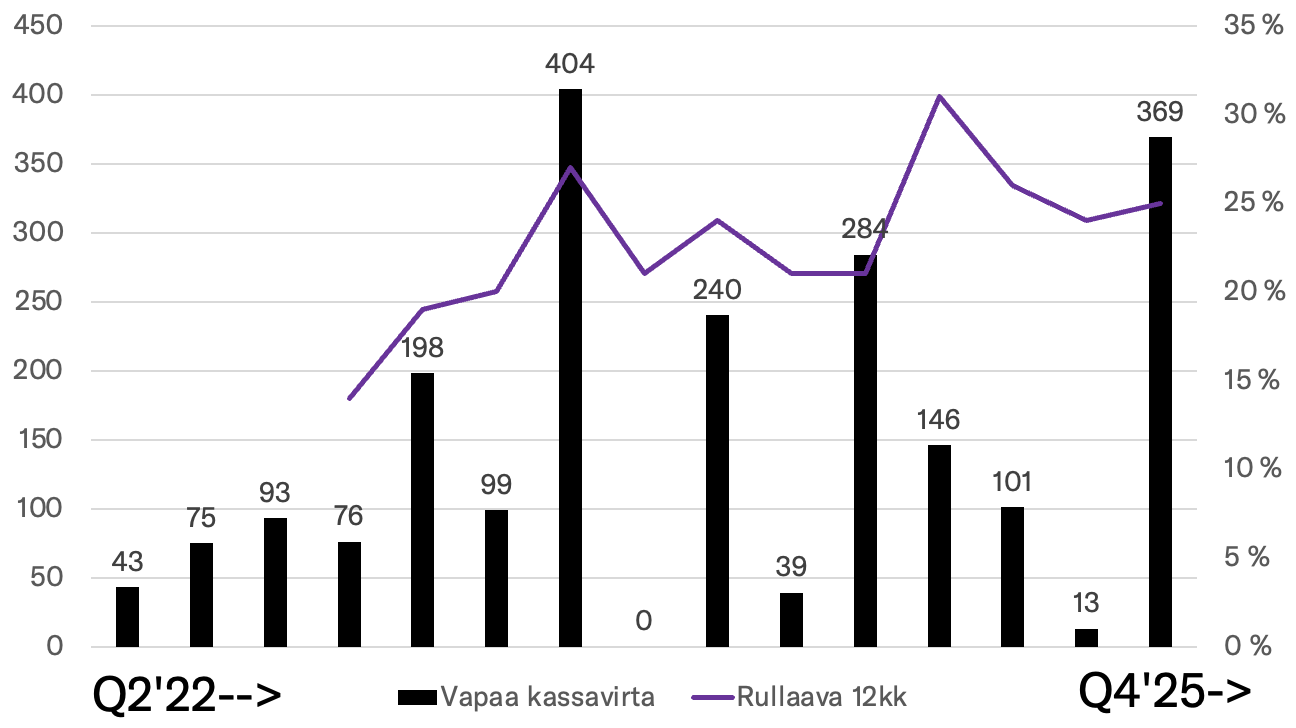

Here is Paradox’s free cash flow from my own records, calculated as operating cash flow minus game development investments. To save time, I didn’t include hardware investments because they only amounted to 3 MSEK (about 300,000 euros) last year, so the impact is negligible. Additionally, the company spent 100 MSEK on studio acquisitions last year, which I excluded as I wanted to examine the core business’s ability to generate free cash flow.

This is the cash flow left over from business operations after growth projects, which can be distributed as dividends or stashed in the bank.

The % figure is the rolling four-quarter free cash flow relative to revenue. Since the company has no debt and its balance sheet (currently 2.6 billion SEK) is only slightly larger than its revenue (2.2 billion SEK), this also serves as a good proxy for return on capital employed (ROCE) at the same time.

25% is a pretty good level, I’d say. Or rather, a very rare level.

In yesterday’s earnings call on YouTube, the CFO speculated that the current investment level of ~150 MSEK per quarter is the “new norm.” In fact, last year and the year before, the figure was 600 MSEK annually. Before that, it was much higher when the company was still funding, for example, the extremely expensive development of Life by You in California.

If the company does not grow and ceteris paribus, the stock trades:

Number of shares 106M * share price 130 = 13.8 billion

minus net cash ~1000 MSEK

= Enterprise Value (EV) 12.8 billion / free cash flow 0.63 billion = EV/FCF ~20x.

That equals a 5% cash flow yield.

Presumably, if one believes in this, free cash flow will grow in the coming years as the core portfolio expands, while the investment level will likely grow more slowly than before.

Of course, if the firm doesn’t grow and faith in growth is completely lost, the stock will start drifting toward the required rate of return. If that is, for example, 10%, the cash flow yield should be 10%. In that case, the stock should cost roughly 60 kronor per share, which would be quite a long way down.

Usually, companies’ free cash flow yields are in the low single digits because firms have to invest heavily just to stay in place, and investors believe in the “salvation” of growth.

What I’m trying to do here is justify to myself why the stock looks dirt cheap after yesterday’s tumble, even with relatively moderate growth expectations. It is, on the other hand, justified—especially if one doesn’t believe in the sustainable growth of the core portfolio or doesn’t believe the company’s investment discipline will hold after the recent years.

Paradox does look bad optically, as Fredrik has been talking about a “new focus on the core” for three years now, yet Bloodlines 2 has hit the windshield. At least Life by You was cut during development. Perhaps the company calculated that it’s better to throw new money after old and finish BL2, for better or worse, rather than cancel the whole project and receive no returns at all.

It’s also worth reminding everyone that a large portion of sales is in USD, while the firm’s expenses are in SEK (except for marketing, which is in USD). The company doesn’t waste money on currency hedging. The krona strengthened (or the dollar weakened against it) by over 10% compared to Q4’24. To put it simply, revenue would have been 10% higher in kronor without this movement. ![]()

Perhaps I’m thinking about this wrong, but I see Paradox as very interesting right now. For example, the thread has mentioned rising PC prices, but in the big picture, these factors come and go. The reception for EU V softened, but we can probably agree that it’s a good platform to build the next 10–12 years of DLC on. And as noted in the thread, retention has been good compared to previous releases.

Finally, some cash flow assumptions. Historically, the company has grown ~15% per annum with its core portfolio. If we assume that:

The company’s free cash flow grows 10% per annum (slightly faster than revenue due to improving profitability) for the next 5 years, reaching about a billion kronor, followed by 3% terminal growth and a required return of as much as 10%, then the current price would be roughly justified (EV = 12 billion, currently 12 billion).

10% is a fairly high requirement because Paradox owns game brands that have proven their longevity, it has a strong position in its own niche, and it is very profitable and relatively stable. But 10% is a good conservative rule of thumb, while others might calculate with 8–9% requirements. ![]()