On Epiphany, I did some stock research and as a result, I opened a new position in my portfolio:

- Buy Coffee Stain Group 1050 shares @ 22.55 SEK

I haven’t seen much talk about the company on the forum, just a few messages here and there, and I couldn’t find a thread for the company, so I’ll open my own investment thesis here.

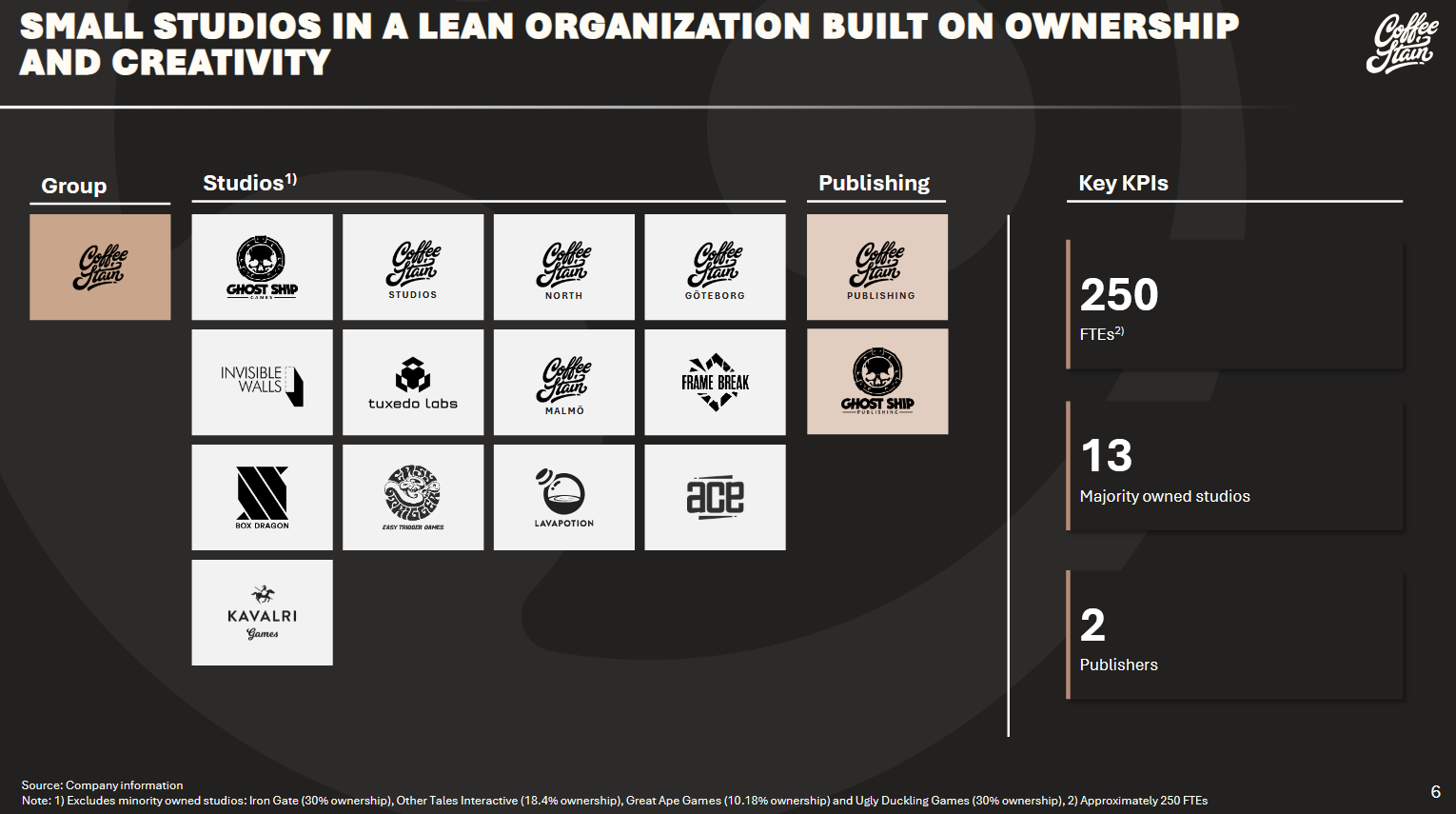

Coffee Stain is a company spun off from Embracer Group, founded in 2010. The company develops and publishes games. As I understand it, the games are mostly “Indie” type, i.e., lower-budget and smaller-scale A or AA games (e.g., Remedy makes larger-budget and larger-scale AAA games). The company’s best-known IPs are below:

Coffee Stain consists of 13 smaller, independent studios that Coffee Stain Group owns either fully or partially. In addition, the company includes 2 publishing studios:

The company has a moderate number of employees relative to the whole, around 250 employees divided among 13 studios. Coffee Stain’s goal is for “small teams to make big games for a huge audience.” The studios are located in Scandinavia, and the company operates on a “decentralized” model with small teams of 5–30 people. This structure should enable a capital-efficient ecosystem where autonomous studios are fully responsible for developing and updating games, and a small core organization provides both strategic and publishing support. The company considers employees its most important asset.

Coffee Stain develops and publishes games on PC, consoles, and mobile devices, combining internal development with selective partnerships on promising projects. The company’s philosophy is to prioritize gameplay quality and long-term cooperation with the player community. In practice, this means early access (early feedback from players), enabling user-generated content (“mods”), and continuous updating. This should allow for sustainable IPs with a committed player base.

In addition to its own game development, the company seeks strategic partnerships and tries to identify high-potential external projects at an early stage, aiming to grow and nurture long-term business relationships with them.

According to my research, the biggest upcoming releases are Valheim 1.0, as well as the PS5 release, and Deep Rock Galactic: Rogue Core, but I haven’t found any more detailed information about upcoming releases or the pipeline.

The company’s flagship IPs have also received very good reviews, and although I haven’t played all the games myself, virtually everyone in my social circle who has played them has praised at least Satisfactory, Valheim, and Deep Rock Galactic. I think this is a good sign. I believe there might also be a lot of “junk” within the studios and portfolios, but I didn’t start investigating deeply enough to go through the past output of all the studios. In the big picture, I think it’s even a good thing that they experiment with all sorts of things with a low cost structure, which of course results in a lot of unproductive junk, but in the case of big successes, the low cost structure allows the business to scale very efficiently.

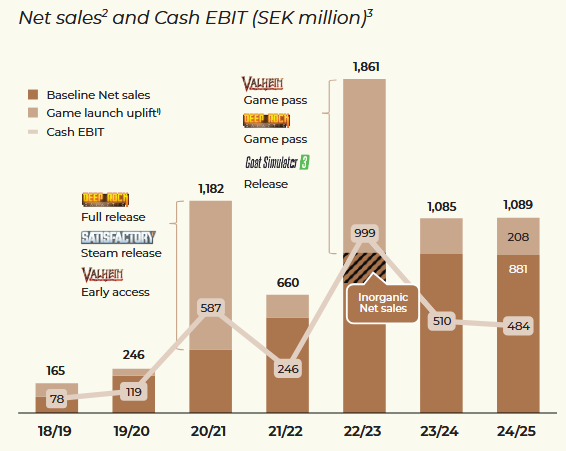

Historically, the company has been able to grow very profitably, although they have been treading water for the last couple of years:

The company’s fiscal year is from April to March, which is why the annual division is presented that way. In this case, Cash EBIT refers to adjusted operating profit excluding depreciation and amortization, less gross investments and lease liability payments. I’m not very skilled with accounting, but my conclusion is as follows: in practice, this is EBIT minus investments, and according to my digging, it has been a smaller figure than adjusted EBIT, and generally, this is well in line with the free cash flow reported by the company.

As can be seen above, even though the company can generate revenue and carve out substantial cash flow with its old IPs (according to my calculations, EBIT% has historically been around 30–50% of revenue), revenue and earnings are typically very volatile for a gaming company, and peaks occur around successful releases.

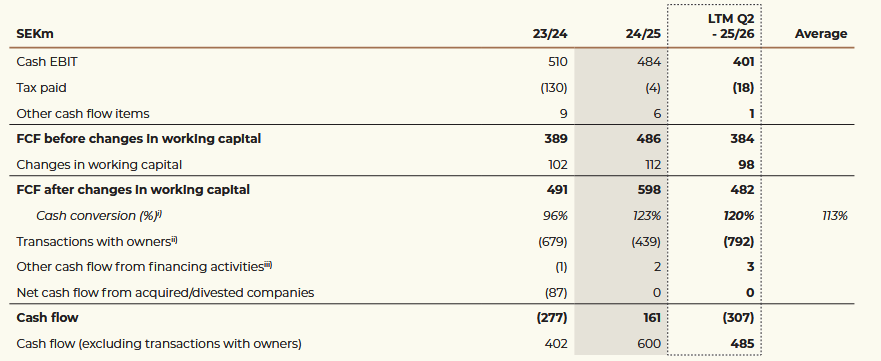

The company’s market cap is currently 4.85 billion SEK. The company has no debt and has 269m SEK in cash, meaning the EV is 4,581m SEK. LTM free cash flow excluding working capital is 384m SEK.

Using simple math, I get an EV/FCF figure of 12.6 or a cash flow yield of ~7.9%. If working capital is taken into account, this looks even better, but I’ll conservatively use that 8% cash flow yield. At this valuation, I don’t think much growth is baked into the stock price; I assume the market is pricing this now so that the revenue/cash flow generated by the company doesn’t grow much, but stays at the current level—the level that can be milked from the current portfolio and DLCs. Thus, I see that no future hit games have been priced into the stock to increase revenue and cash flow.

- Focus and strong expertise in its own niche, which is always a plus.

- From a player’s perspective, it’s a good strategic combination: focusing on games with great playability while operating with low-cost, small teams on low-budget A and AA-level games. These games still have high revenue potential upon success, and thanks to the low costs, the business should scale well.

- Since the creators are key in these types of games, it’s good to see that the company considers its employees its greatest asset, at least based on their rhetoric.

- The current valuation is very low in my opinion, and I don’t believe any growth has been priced in.

- If the company could achieve a performance similar to the 22/23 financial year (which was a very strong year due to the Valheim and Deep Rock Galactic Game Pass deals and the launch of Goat Simulator 3), the firm would be priced at an EV/EBIT of ~4.6 with an EBIT of 999m SEK.

- In a favorable scenario, I see the company’s cash flow growing significantly from current levels, alongside a significant expansion in valuation multiples.

- The risk I see is the possibility of the company becoming a “value trap”—meaning they fail to release successful games in the future, causing revenue and cash flow to wither over time, with the share price following suit. However, with the current strong cash flow generation, I don’t see the valuation multiples dropping much further, so I believe it’s unlikely to lose much money in the long run.

- Based on the above, I see an excellent risk-reward ratio here; if the positive development continues, the business could at least double on a 5–10 year horizon, and there is room for multiples to expand, while the downside seems limited.

- Aki Pyysing has also written a column about the firm which is definitely worth reading: Coffee Stain – digisauruksen hyppy tuntemattomaan | Sijoitustieto.fi I haven’t read other analyses of the stock, but I noticed that insiders have apparently been buying. According to the article, the main owner has bought shares for 11.3m SEK, the CEO for 8m SEK, and the CFO for 2m SEK. I tried to verify this myself but couldn’t find the information anywhere; regardless, if management is buying heavily, it’s a positive signal—they wouldn’t buy if they didn’t see value in the business.

- I believe the market is currently underpricing the company because nobody knows about it. This is a company worth about 450 million euros, which was spun off in December from the widely disliked Embracer Group, so I assume that’s why no one is interested yet.

- The starting position size is a modest 3% of the portfolio, mainly because I don’t have any more spare cash at the moment and I don’t want to sell anything from my portfolio right now.