A good summary that it’s about risk management. One perspective that I haven’t noticed mentioned yet is the cyclicality of earnings. Share buybacks are a catastrophic way to distribute profits for cyclical companies or companies whose markets undergo significant changes. A company’s earnings and share price often correlate, so buybacks often occur at a high price. Often, dividends from cyclical companies are a good way to perform sector rotation. Also, investing solely in business growth is risky because speed blindness often strikes during good times. There was even an article about this effect in Salkunrakentaja.

1 Like

Exactly. For example, the cyclical construction company NVR. Ruined its returns with share buybacks. If only the owners and management were from Finland, we would get dividends.

14 Likes

Quite true, US stocks are certainly a different story. There are probably few cyclical companies in the US that wouldn’t have benefited from putting all their money into buybacks because the multiples are now right. Replace them with an average European builder, and the picture is a bit different. Mainly, I wanted to raise the idea that owners of European and especially Finnish cyclical companies wouldn’t be any happier if they had bought back their own shares with peak-cycle profits. Neste, UPM, YIT, etc. In the US, it has certainly worked well and may well continue to do so.

1 Like

@Mirko_Sampo_IR, @Pohjolan_Eka and @Verneri_Pulkkinen

“Fundamentals, TA, and dividends, but the greatest of these is dividends”

7 Likes

Although I believe that share buybacks are a categorically better way to distribute profits, it must, of course, be admitted that dividend distribution also has certain undeniable advantages, at least three of them:

-

Tax advantages, which have been discussed so many times that they hardly need repeating.

-

A certain subgroup of investors benefits from the fact that company management, without asking and without taking any stance on the investor’s current life situation, goals, or liquidity needs, regularly forces the realization of capital tied up in shares. The more psychological stress selling shares causes, the better the alternative becomes where company management forcibly distributes capital to the account.

-

The most important reason why all discussion about dividends and buybacks ultimately turns into bickering over preferences. For a large part of people, dividends simply feel so good that they want them to continue. It often provides a considerable dopamine rush when dividends pour into the account, as if one had found a hugely valuable banknote on the street. Even though the money hasn’t come from nowhere, it feels like it. It’s no use saying that in the long run, buybacks could earn more money or give investors more decision-making power from management, because research into gambling has also repeatedly shown that small and regular wins directly impact human psychology and hook people into continuing the activity.

Dividend investors often build these kinds of mythological counterparts for themselves, like geese laying golden eggs, and generally convince themselves that they are wiser, more long-term, and better at managing risk than other investors. When you discuss enough, the core reason for dividends usually turns out to be the same as for people who order a pizza from Foodora to their home instead of walking 100 meters to the restaurant to pick up the same pizza cheaper themselves: “Because I want to.” Hard to argue with ![]()

16 Likes

AI summary of dividends and buybacks🙂

Dividends

Advantages

- Clear and stable income for investors

- Many investors, especially retirees and conservative investors, value regular and predictable dividends.

- Signal of financial strength

- A stable and growing dividend can signal that the company’s cash flow is strong and its business is on a sustainable footing.

- Equal benefit for all owners

- All shareholders receive their dividends directly and do not have to sell their shares separately to benefit.

Disadvantages

- Tax disadvantages

- Dividends are often taxed immediately, making them a less efficient way to return capital compared to buybacks.

- Less flexibility for the company

- A company must keep dividends stable or growing, as cutting a dividend is seen as a negative signal by the market. This can limit the company’s financial flexibility during difficult times.

- May limit growth investments

- Paying large dividends can prevent a company from investing in growth or reducing debt.

Share Buybacks

Advantages

- Tax efficiency

- Buybacks can be more tax-efficient than dividends because investors do not pay taxes unless they sell their shares.

- Flexibility for the company

- Buybacks are one-off events and do not create the same permanent expectation as dividends. A company can adjust the amount of buybacks according to its financial situation.

- Increasing share value

- Buybacks can increase the share price as the number of shares decreases. This particularly benefits investors who do not sell their shares.

- Signal of undervaluation

- If a company buys back shares, it can signal that management believes the stock is undervalued.

Disadvantages

- Uncertain benefit for investors

- Not all investors may benefit from buybacks in the same way as from dividends. The benefit depends on the share price development.

- Poor timing

- If a company buys back its shares at a high price, it can be a bad investment and reduce shareholder value.

- May mask problems

- Buybacks can temporarily beautify key figures, such as earnings per share (EPS), but do not solve fundamental business problems.

- Uneven distribution of benefits

- Buybacks benefit investors who hold their shares more, while dividends are distributed equally to all.

Which is better?

- Dividends are better:

- If an investor wants regular and stable income.

- When taxation is not a significant factor or the investor values direct cash flow.

- Buybacks are better:

- If the company’s stock is clearly undervalued.

- When investors prefer tax efficiency and expect the share price to rise.

- When the company does not have sufficient profitable investment opportunities but wants to maintain its flexibility.

Summary:

- For an investor who values income and predictability, dividends may be a better option.

- For a company and investors who value tax efficiency, buybacks are often a better choice.

- The best approach depends on the investor’s goals, the company’s situation, and market conditions. Often, a combination of both can also be an effective solution.

4 Likes

These practically go hand in hand. Statistics already show that buybacks are accelerated at the peak of a business cycle, when valuation levels are understandably tight. As uncertainty grows and the price comes down, buybacks freeze.

Timing truly requires evidence and discipline from management. Few companies have a track record of this.

5 Likes

What dividend-paying dividend aristocrat ETF would you recommend?

Agreed.. Additionally, if management’s compensation is strongly tied to a bonus model whose realization is boosted by share buybacks regardless of price.. Those management bonuses are the biggest risk in the whole setup… They pursue their own interest to make the metrics sufficient for hefty bonuses..

In some companies, shares are even bought back with leverage.

Those management compensation models/options should definitely be read carefully.

3 Likes

Let’s emphasize again that the tax benefit is almost always in share buybacks, not dividends, as has been discussed many times. Even when one wants those dividends in hand every year. Let alone if one doesn’t. Taxation is not, in most cases, a reason to hope for dividends. In a couple of quite artificial extreme cases, it might be different.

I agree with you on points 2 and 3. And that is the biggest reason for this (at least to some extent Finnish) phenomenon. Poor people are not the best at calculating returns and the consequences of sales and changes in ownership, and they start getting euros appearing from nowhere into their account. People get excited by less. Add a couple of “investor gurus” spreading misinformation, and the cult is ready. Almost every time I’ve attended shareholder meetings, some poor soul asks in their speech, “but could we also get a little more of those extra dividends?”

7 Likes

Well, that’s how it is sometimes in (investment) life, that what is artificial for some is just normal/genuine (investment) life for others.

Certainly, but in about 100% of the cases when this topic has been discussed, not a single writer has had such a special situation in mind or experienced it themselves. So, I would again seek relevance for that discussion. I don’t believe that any counter-argument or repeater of those erroneous claims understands those special situations any better if they don’t understand normal situations or can’t calculate them.

4 Likes

However, it’s not a special situation, but a completely normal (personal) situation for a low-income investor.

1 Like

Well, I’d say that less than a fraction of a per mille of dividends received by Finns are taxed as earned income. So yes, it is a marginal situation in every way.

However, we are on a discussion forum where it’s impossible to list all special situations related to this in every message. That’s not the point, and usually, the context clarifies whether we are talking about Bermuda and a low-income investor or not.

And even in that case, it might be more sensible for many to receive profit distribution as share repurchases + sales rather than as earned income.

3 Likes

Well, I don’t have statistics available, so I can’t say how marginal a group it is.

But since we are on a discussion forum, I think it’s relevant to bring up different perspectives.

Even if that perspective isn’t relevant for the average investor.

Surely those marginal / minority investor groups also have the right to be heard ![]()

![]()

![]()

2 Likes

Well, I completely agree with this. And that is, of course, a good thing. And marginal cases are not in conflict with more general cases in themselves. It is essential to understand how taxation and pricing work in different profit distribution methods.

Well, of course they do. I don’t disagree with that. But then it’s good to state what it’s about and what the specific circumstances are in which, for example, dividends become lighter from a tax perspective, and why that is.

1 Like

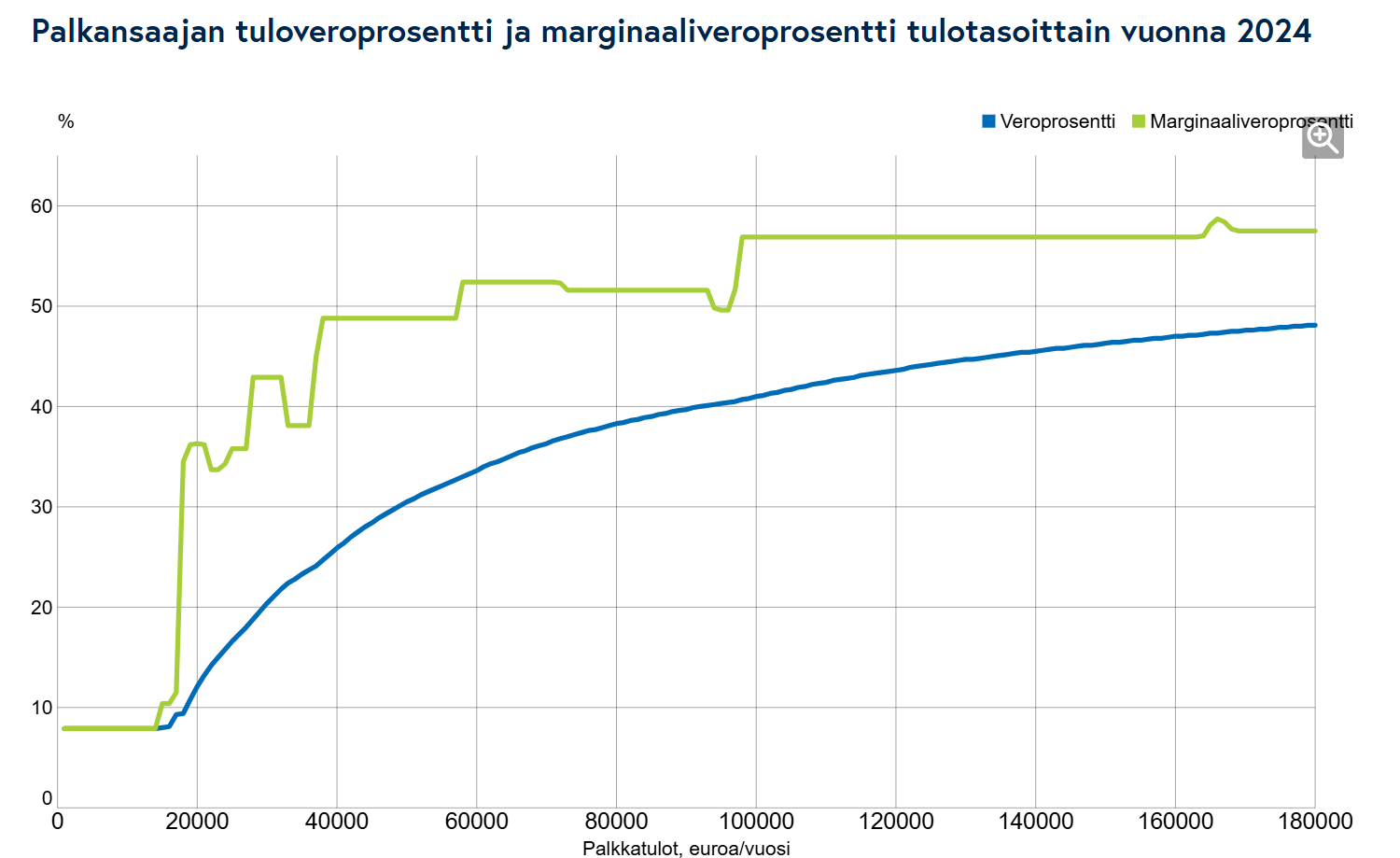

Have you remembered to use marginal tax in the comparison? Income must be a maximum of 17k€ for dividends taxed as earned income to be moderately taxed.

3 Likes

Yeah, in this case, a “lower-income investor” had an income level of less than €15,000/year.

Good to know that limit.

It hasn’t really become clear to me why those (without tax treaties) dividends are taxed differently. It’s still the exact same type of income as dividends received from elsewhere. In my opinion, it unnecessarily complicates taxation.

3 Likes

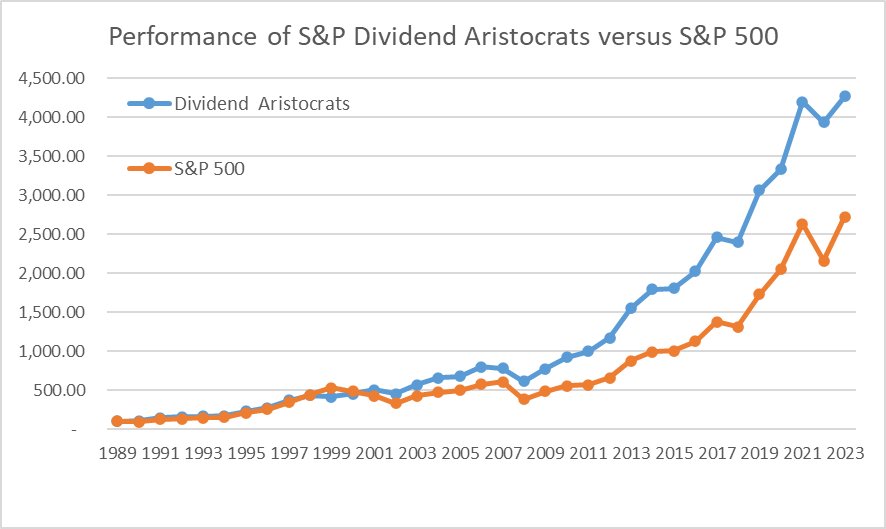

For that comparison of dividend aristocrats versus S&P to make sense, it would have to include all the aristocrats from the comparison’s starting year and only them. Without any additions or omissions. So, the successful ones from the last 25 years would be taken for comparison, and we would see if they continue to succeed, meaning if history would indeed be a guarantee of the future.

2 Likes

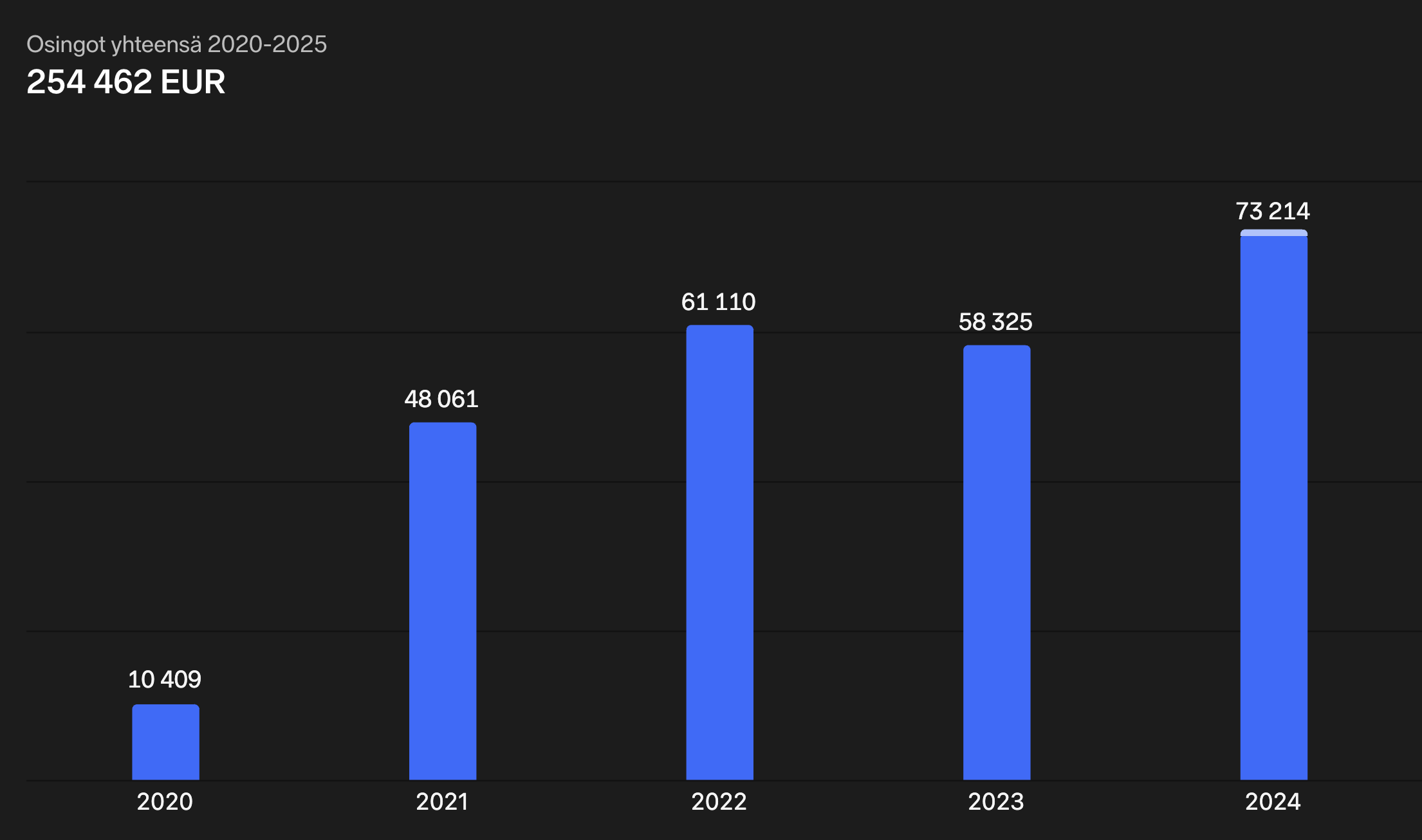

The last dividends of the year arrived in the account, reaching a new record in the dividend sum. As a lifestyle unemployed person, one appreciates the regular cash flow used for living it up.

75 Likes