Those active owners have sold shares in block trades.. I wonder if the old owners from the Privanet era sold them there?

Kim Vaio has at least bought (it). Do you have any facts or just an assumption about the matter?

Interesting information. Where did you find the information about who made the block trades? Could you provide a link?

1 Like

Magnus Granljung sold 6.62 million shares in the construction company Nyab, where he is vice president, on March 21. The shares were sold at a price of 5.20 kronor per share, a transaction worth 34.4 million kronor. This is evident from Finansinspektionen’s insider register.

Granljung subsequently holds 12.76 million shares, corresponding to 1.79 percent of the shares in Nyab, according to an update from the ownership service Holdings.

What kind of game is this? From pocket to pocket and the market in panic on Friday and today.

1 Like

Didn’t you read the news? The same person bought over 12 million shares right after.

Only sold 6.62 million shares.

Thanks for the translation. I don’t understand a single thing in Swedish ![]() Okay. Even fewer answers to this whole thing.

Okay. Even fewer answers to this whole thing.

1 Like

The word ‘äger’ is missing from that last paragraph. So, [they] sold 6.62 million shares and still own 12.76 million shares after that.

4 Likes

Yes, you are right. Thank you for the correction.

Is the man changing jobs or is a pipe renovation coming?

An encouraging comprehensive analysis of NYAB from Inderes. A concise summary is attached, and below it, a link to the analysis itself.

Inderes reiterates its buy recommendation for NYAB and raises the target price to SEK 7.0 (previously SEK 6.8). The company has successfully navigated a challenging market and is expected to continue its strong growth and profitability development through expansion into the Norwegian markets and strategic investments. NYAB has a unique market position that supports strong growth and industry-leading profitability.

https://www.inderes.fi/files/61b2bfa7-c67c-4a34-9bb9-c4eda9288259

3 Likes

Christoffer Jennel has commented on NYAB’s new order. ![]()

3 Likes

Christoffer Jennelin and Aapeli’s preliminary comments regarding NYAB’s Q1 to be published on Wednesday. ![]()

EDIT: I changed this to the Finnish version ![]()

NYAB will publish its Q1 report on Wednesday. We expect strong revenue growth (Q1’25e: +55% y/y) mainly due to corporate acquisitions and favorable market conditions in Sweden. We also expect the operating profit margin to improve, supported by a favorable project portfolio, reduced seasonality, and sustainable cost efficiency. In addition to the figures, the report will be particularly interesting for management’s comments on market outlook, Dovre’s integration, and strategic direction.

3 Likes

A new extensive report has been made on NYAB, or well, newish:

“Translation: Original published in English on 03.04.2025 at 8:16***”

We reiterate our buy recommendation for NYAB and raise our target price to SEK 7.0 (previously SEK 6.8) in connection with the update of our extensive report. NYAB, a specialist contractor for complex and challenging construction projects, has skillfully navigated the challenges of the broader construction market in recent years. Although the company is not immune to weaker macroeconomic conditions (see depressed margins 2023–2024), it remains a leader in the industry in terms of growth and profitability. With recent acquisitions providing access to the Norwegian market and significant investments made in the company’s target markets, we expect NYAB to continue its strong growth and profitability development in the coming years.

3 Likes

Here are Christoffer Jennel’s preliminary comments as NYAB publishes its results on Wednesday. ![]()

The company has started 2025 strongly with robust revenue growth, and we expect this development to continue in Q2. Key drivers include favorable market conditions in Sweden, a gradually improving outlook in Finland, and the M&A effects of the Dovre acquisition. We expect operating profit margins to remain fairly stable, with Dovre’s consolidation anticipated to slightly weigh on the group’s profitability. Beyond the main headlines, management’s comments on market outlook, Dovre’s integration, and strategic direction will be key areas of focus.

3 Likes

Here are Christoffer Jennel’s comments on NYAB’s results. ![]()

NYAB’s Q2 revenue was stronger than expected, and operating profit was in line with forecasts. Organic revenue growth was primarily due to high production volumes in both the energy and infrastructure sectors. The order book continued to grow, reaching a new record level, supporting strong growth momentum for the rest of the year. Dovre’s integration is progressing as planned, and management’s comments do not indicate significant changes in market outlook.

3 Likes

Christoffer haastatteli englanniksi NYABin toimaria Johan Larssonia. ![]()

NYAB has released its Q2 report, showing continued growth in revenue. In this interview, CEO Johan Larsson shares his insights on the current market conditions, ongoing developments across the company’s key markets, and the factors investors should watch closely in the months ahead.

1 Like

Aapeli and Christoffer have prepared a new company report on NYAB after Q2. ![]()

NYAB’s Q2 revenue rose above expected levels, and operating profit was in line with forecasts. The market situation in Sweden remained favorable, while the demand situation in Finland is still relatively soft. The order book reached a new record high, and a strong order-to-billing ratio indicated continued strong demand. Management emphasized that the company has not encountered capacity constraints and that the organization has been proactively scaled to meet anticipated growth. Following the Q2 report, we have raised our revenue forecasts and only slightly lowered our margin assumptions. Therefore, we still see attractive risk-adjusted upside potential in the stock, driven by estimated earnings growth for the coming years. Due to the recent strong share price increase, we lower our recommendation to ‘add’ (previously ‘buy’) while raising our target price to SEK 8.25 (previously SEK 7.2).

https://www.inderes.fi/research/nyab-q225-voimakkaan-kysynnan-tehokasta-toteutusta

Pleasing YTD for NYAB

3 Likes

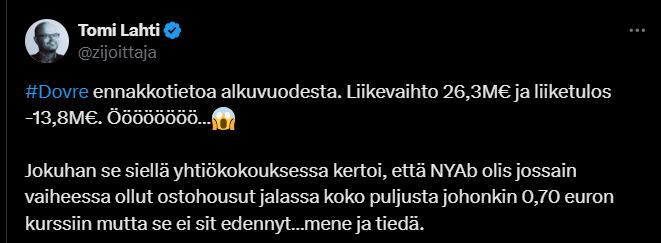

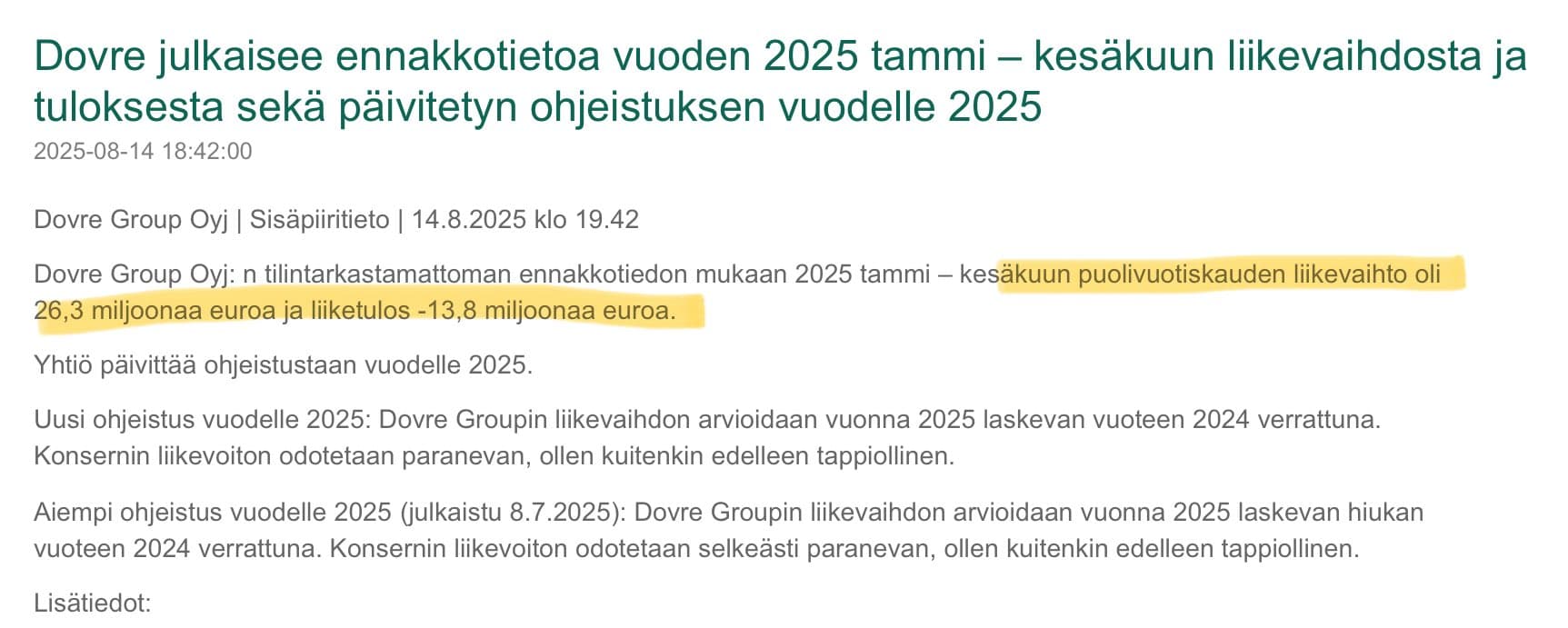

Tomi Lahti & Dovren negari

2 Likes

Here are Aapeli Pursimo’s comments on how NYAB has signed a couple of new contracts. ![]()

3 Likes

ABG’s comments on how GRK Infra’s raised guidance strengthens the view that the Finnish infrastructure market is picking up.

According to ABG, this also supports NYAB, which benefits from a strong order book and continues to grow by double digits in Nordic energy and infrastructure projects.

Based on our estimates, the NYAB share is valued at 10-9x EBITA in 2025-2026, in line with key infra/construction peers that we expect will deliver slower growth and lower margins than NYAB.

1 Like

Hi everyone! My name is Christoffer Jennel and I cover analysis at NYAB. Since our forum has now switched to multilingual mode, you can ask me questions and I will participate in the discussion here.

10 Likes