Toimitusjohtaja Yrjö Trögin mietteet Paulin haastattelussa

Norrhydron liikevaihdon kehitys säilyi heikkona, vaikean kysyntäympäristön vallitessa. Epävarmuudesta huolimatta yhtiö odottaa liikevaihdon ja raportoidun käyttökatteen kasvavan tänä vuonna.

Aiheet:

00:00 Aloitus

00:17 Loppuvuoden yhteenveto

01:27 Nykyisen kulurakenteen kestävyys

02:34 Nykyinen rahoitusasema

04:14 Ohjeistuksen taustaa

05:31 ”Kilpailu on erittäin kovaa”

06:55 NorrDigin keskeiset kasvuajurit

08:43 NorrDigi EMA:n tilanne

09:13 Strategiset kumppanit

Ilmeisesti vaiwereissa ei ole mitään teknisiä ehtoja, mutta uskon rahoittajilla olevan tässä kohtaa valtaa, mikäli suorasanaisesti haluaisivat, että yhtiötä tulisi pääomittaa lisää. Kuulosti että kasvun ja kannattavuuden näkymä vuoteen 2025 on asiakaskohtaisten tilausnäkymien myötä positiivinen ja parempi kuin 24 loppuvuosi. Mm. Ponssen vahvat tilaukset Q4:llä mahdollisesti vaikuttavat näkymään positiivisesti, vaikka Norrhydro ei tätä erikseen nimeltä maininnut.

Jo H2:lla liiketoiminnan rahavirta oli positiivinen, mutta investoinnit vetivät vapaan rahavirran nollaan. Kassan pienentyminen syntyi lähinnä velkojen takaisinmaksusta. En siis näkisi osakeantia väistämättömänä, jos tässä ollaan siirtymässä neutraalista vapaasta rahavirrasta lievästi positiiviseen (olettaen että positiivinen ohjeistus pitää). Yhtiön omien sanojen mukaan erilaisia rahoitusratkaisuja voitaisiin harkita, jotta uusien tuotteiden kasvua voitaisiin kiihdyttää (käyttökohteita esim. myynti ja asiakaskohtaisten prototyyppien rakentaminen nyt olemassa olevien lisäksi).

Minulle jäi sellainen kuva, että uusien tuotteiden myynti on kyllä lähdössä käyntiin, mutta sen vaikutus kokonaiskasvuun on lähiaikoina aika pieni ja alkuvaiheessa kannattavuuskaan ei ole erityisen hyvä, kun täytyy ramp-upata uudentyyppistä tuotantoa. 2025 näkymät ovat siis pääosin perinteisen liiketoiminnan varassa.

Pauli on tehnyt uuden yhtiöraportin Norrhydrosta heti H2:n jälkeen.

H2-raportti jäi vaisun kysynnän vuoksi odotuksia heikommaksi, vaikka toisaalta kulurakenteen tehostuminen nostaa lyhyen aikavälin tulosnäkymää, jos kysyntä vain kääntyy. Korkea velkaisuus vahvistaa tulosodotusten muutosten heijastumista osakekurssiin ja toisaalta nostaa riskitasoa. Huomioiden NorrDigin kasvuennusteiden siirtyminen pidemmälle tulevaisuuteen sekä lyhyen aikavälin rahoitusasemaan liittyvät epävarmuustekijät, laskemme suosituksen tasolle vähennä (aik. lisää) ja tavoitehinnan 1,50 euroon (aik. 2,1 €).

Kova on leikkuri ollut liikevaihdon kehityksen osalta 2025e -vuodelle jos oikeasti “vain” 10,6% LV kasvaa. Asiakkailla tilauskertymät: Ponsse +12%, Metso +13%, Cargotec +3% Kalmar +20%, jotenka pohja on nyt lienee kuitenkin takana (ainakin toistaiseksi ). Noh toivotaan, että liikevaihto nyt kasvaisi kuitenkin reilut 15%.

En usko, että osinkoa tullaan maksamaan 2027 alkaen, enkä myöskään tätä toivo. Jos jotakin toivon, niin osakkeenomistajien äänestävän tätä vastaan ainakin muutaman vuoden. Jos kauppa käy niin panoksia nyt sitten siihen kasvuun. Jos taas kauppa ei käy niin korkea korkoisia lainoja pitää keskittyä makselemaan pois. Ei näytä järkevältä tällä vuosikymmenellä maksella osinkoja oikeastaan missään tilanteessa. Myyköön keittiöremonttimiehet lappujaan, ja jättäköön liiketoiminnan rauhaan.

Loppuun kysymys: onko Volvon kaivuriyksinoikeus nyt sitten päättynyt? Eikös se alunperin ollut 2024 loppuun asti.

Kyllä nuo mainitsemasi asiakkaiden tilauskertymät tarjoavat tukea kasvuun. Toki meidän ennusteemme ei ole kovin kaukana mainitsemiesi yhtiöiden tilauskehitysten keskiarvosta. Samalla tärkeimmän asiakkaan Ponssen (arviolta noin 25 % osuus liikevaihdosta) liikevaihto-ohjeistus vuoteen 2025 on varsin varovainen (Inderes ennustaa 3 % kasvua), mikä vaikuttaa ennusteeseemme Norrhydrolle.

Vuoden 2027 osingon arviointi on vielä haastavaa eikä minulla ole siihen vahvaa näkemystä. Yhtiö maksoi vuodelta 2022 osinkoa (0,06 euroa), vaikka velkaisuus oli jo silloin koholla. Olisin taipuvainen samalle kannalle kanssasi, että osingon maksamisen lykkääminen voisi olla perusteltua vielä vuonna 2027, mikäli nettovelkaisuus on yli 2x suhteessa käyttökatteeseen (ennusteemme 2,1x 2027e).

Minulla ei ole uutta tietoa mahdollisista muutoksista Volvon kaivuriyksinoikeuteen. Erkin laatimassa laajassa raportissa oli maininta, että kaupallistamiseen saakka. Voisin jutella tästä yhtiön kanssa, kun todennäköisesti käyn heitä kevään aikana tapaamassa Rovaniemellä. Toisaalta, yksinoikeuden päättyminen tuskin tarkoittaisi välittömiä uusia kehitysprojekteja kilpailevien valmistajien kanssa. Tähän vaikuttaa mm. Norrhydron niukat taloudelliset resurssit, joita uudet kehitysprojektit vaativat sekä toisaalta edelleen suhteellisen aikaisessa vaiheessa oleva kaupallistamistyö Volvon kanssa.

Vähän tuossa kirjanpidosta mitään ymmärtämättömänä lueskelin tuota tänään tullutta vuosikertomusta ja siellä pomppasi silmään vuokran määrä joka noussut aika huimasti tuossa vuoden aikana aikana. Vai nousee vasta ensi vuonna? koska tuossahan sanotaan, että seuraavalla tilikaudella maksettava vuokran määrä?

Ja onkohan tuo “Vuokrasopimuksen mukainen kokonaisvastuu” mikä tilinpäätöksessä mainitaan kokonaismäärä joka maksetaan koko vuokrasopimuksen ajalta eli 15v?

Nuo Inderesin aikaisemmat julkaisut kasvuloikan kynnyksellä ja lähitulevaisuus turvattu (Norrhydro Group) näyttävät nyt huolimattomilta julkaisuilta piensijoittajan kannalta ja ovat käymässä kalliiksi?

Voisitko hieman tarkemmin avata että mihin viittaat huolimattomuudella ja mikä tässä on käymässä kalliiksi?

Kävin katsomassa analyytikon kommentit noista julkaisuista ja “Kasvuloikan kynnyksellä” julkaisussa suositus oli myy kun kurssi oli 4,14 EUR ja tässä lainaus analyytikon perusteluista:

“Koska Norrhydro koostuu kahdesta näkymiltään hyvin erilaisesta liiketoiminnasta (perinteiset hydraulisylinterit ja NorrDigi), arvotamme yhtiötä etupäässä osien summa -mallin mutta lisäksi myös DCF-mallin avulla. Osien summa –mallimme antaa osakkeen arvoksi noin 3,5-3,6 euroa keskiarvon ollessa 3,6 euroa/osake. Osien summasta reilu 80 % kuuluu perinteiselle hydraulisylinteriliiketoiminnalle, joka on helpommin arvotettava. DCF-mallimme indikoi osakkeelle noin 3,6 euron käypää arvoa. Osakkeen tuotto/riskiprofiili on lyhyemmällä aikavälillä epäsuotuisa, sillä tuotto-odotuksen nousu tuottovaatimuksen yli edellyttäisi selvästi odotuksia parempaa tuloskehitystä 2022-2024.”

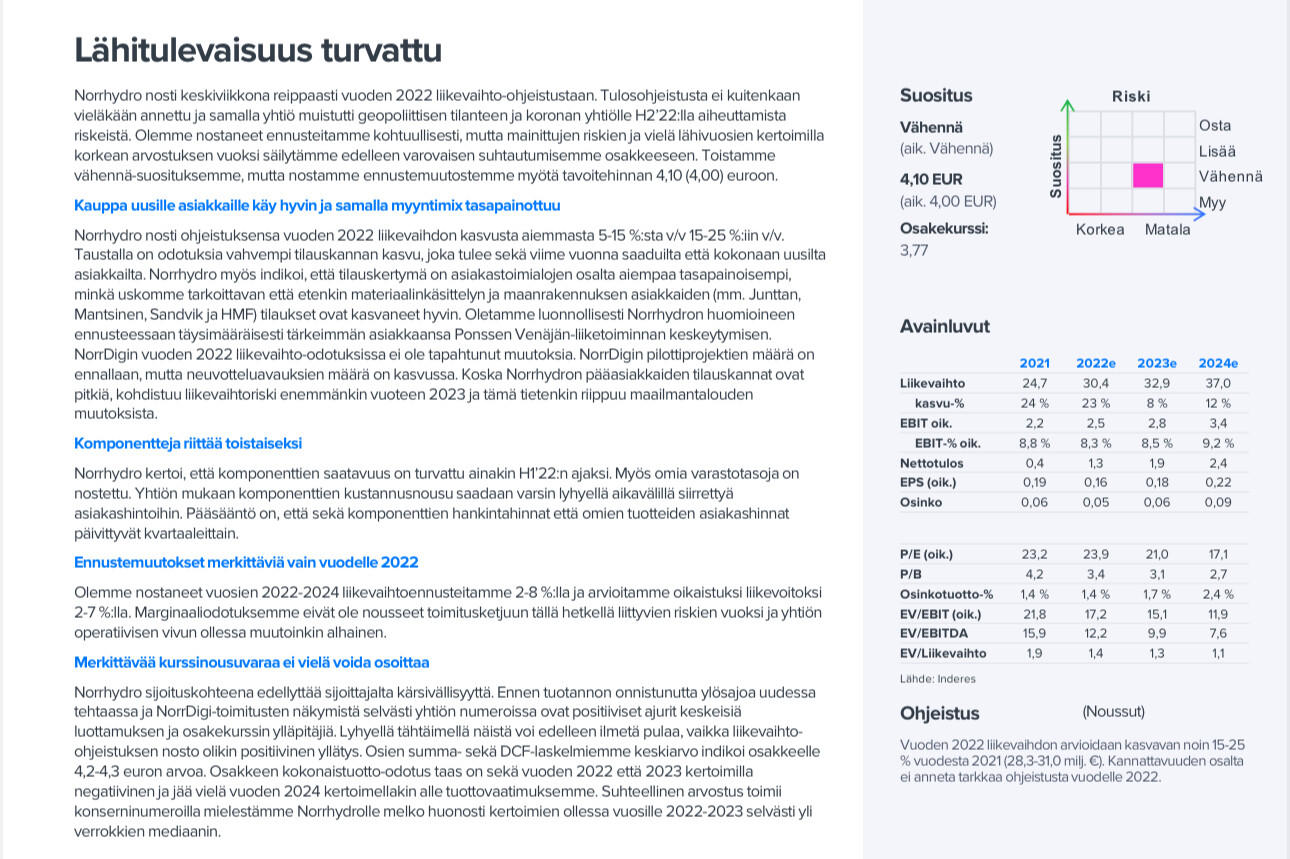

“Lähitulevaisuus turvattu” julkaisussa suositus oli vähennä kurssin ollessa 3,77 EUR ja tässä taas lainaus analyytikon perusteluista:

“Norrhydro sijoituskohteena edellyttää sijoittajalta kärsivällisyyttä. Ennen tuotannon onnistunutta ylösajoa uudessa tehtaassa ja NorrDigi-toimitusten näkymistä selvästi yhtiön numeroissa ovat positiiviset ajurit keskeisiä luottamuksen ja osakekurssin ylläpitäjiä. Lyhyellä tähtäimellä näistä voi edelleen ilmetä pulaa, vaikka liikevaihto-ohjeistuksen nosto olikin positiivinen yllätys. Osien summa- sekä DCF-laskelmiemme keskiarvo indikoi osakkeelle 4,2-4,3 euron arvoa. Osakkeen kokonaistuotto-odotus taas on sekä vuoden 2022 että 2023 kertoimilla negatiivinen ja jää vielä vuoden 2024 kertoimellakin alle tuottovaatimuksemme. Suhteellinen arvostus toimii konserninumeroilla mielestämme Norrhydrolle melko huonosti kertoimien ollessa vuosille 2022-2023 selvästi yli verrokkien mediaanin.”

Mielestäni Erkki oli kyllä noissa suosituksissa näin jälkikäteen viisastellessa ihan oikeassa sen suhteen että riski-tuottosuhde ei ollut houkutteleva, ja yhtiön kohdalla riskit realisoituivat sylinterimarkkinan sulaessa alta samalla kun uusi tehdas saatiin tuotantovalmiuteen.

Jotenkin vain tulee mieleen, kun lukee nuo taustatiedot, mihin viittaan: savolaisten jutut, joissa vastuu jää aina ”kuulijalle” siitä kyllä jossakin vähän varoitettiin.

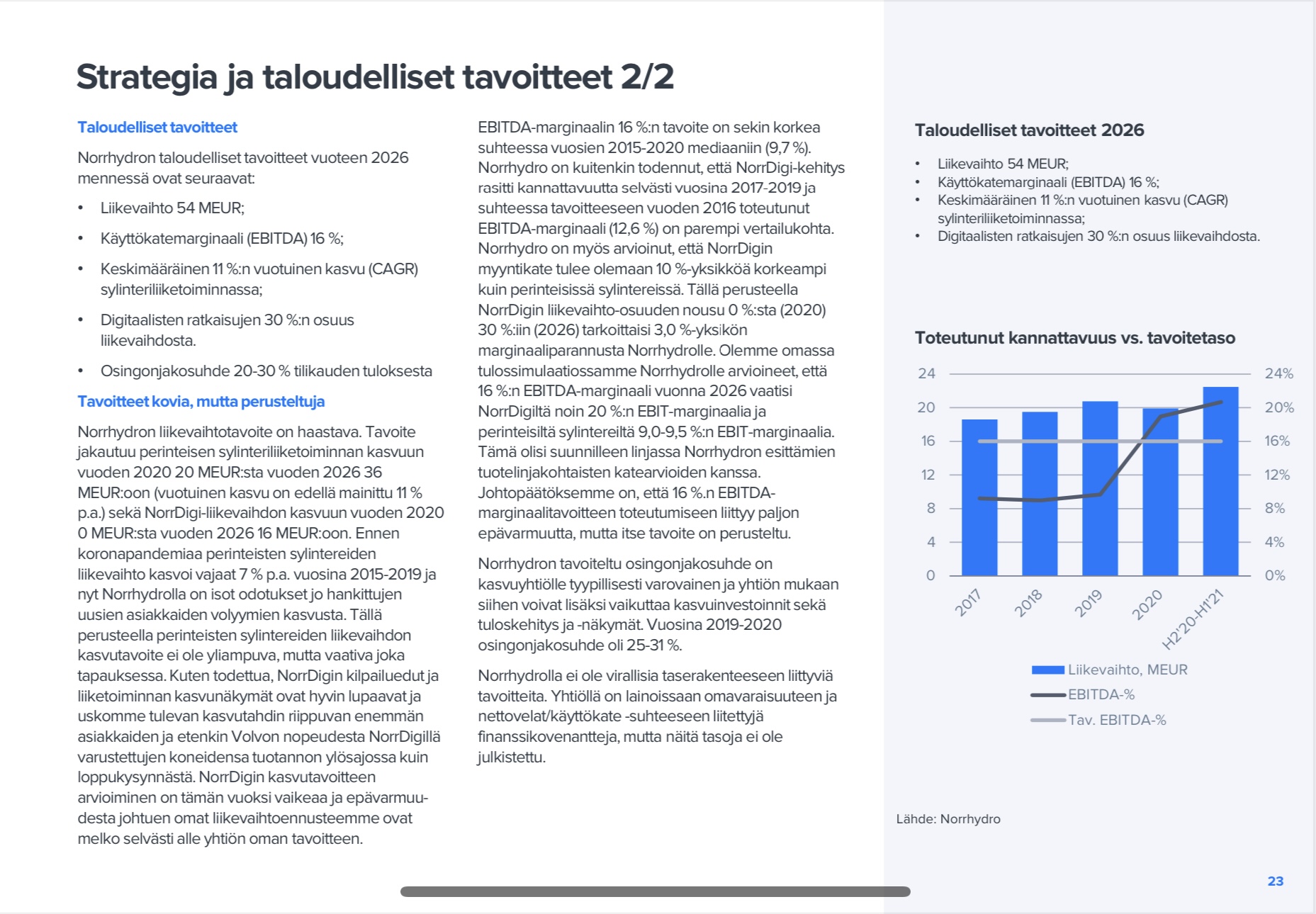

54 meur lv 2026 niin voishan sen vielä ehkä lisärahoituksella/jollakin yritysjärjestelyillä junailla kasaan?

Hyvä bongaus! Tiedustelin asiaa yhtiöltä. Ilmeisesti vuokrasopimuksessa on vuosille 2025-26 korkeampi vuokra, minkä jälkeen palaa alemmas. En ollut tästä korotuksesta tietoinen viimeisimpiä ennusteita tehdessä. Meidän mallissa liiketoiminnan muiden kulujen sekä henkilöstökulujen kasvu on yhteensä 0,4 MEUR vuonna 2025 ja 0,9 MEUR vuonna 2026, mihin on oletettu mukaan kasvua henkilöstökuluissa tuotannon volyymien kasvun myötä. Voidaan siten päätellä, että ennusteidemme saavuttaminen on nykyisen tiedon valossa haastavampaa vuokrakulun nousun myötä. Suurin muuttuja kulupuolella on kuitenkin bruttokate, jonka “normalisoituminen” lähemmäs 50 %:n tasoa riittäisi suotuisassa skenaariossa selvästi kattamaan tuon vuokrakulun nousun. Meillä on ennusteissa varovaisempi, mutta kuitenkin nousujohteinen 47,5-47,9 % vuosille 2025-26 (2024: 45,8 %).

Lisäyksenä vielä, että vuokravastuissa on mukana koko jäljellä olevan vuokrakauden maksut (15v miinus jotain).

Eli kyllä ne toteutuneet riskit: syklisen markkinan sulaminen alta ja uuden tehtaan investoinnin jälkeinen velkataakka ja hankala rahoitusasema on siellä näkyvästi minusta mainittu.

Helpottaisi tässäkin jos sanoisit että missä raportissa tämä 54 meur lv on vuodelle 2026 on mainittu? Vilkaisin vanhoja laajoja raportteja ja ainakin 30.5.2023 julkaistussa laajassa raportissa vuodelle 2026 oli ennustettu 55 meur liikevaihtoa. Jos en väärin muista niin tuohon aikaan sylinterimarkkinan kysyntänäkymät olivat vielä ihan hyvät. Onko sinulla jotain perusteluja tuohon että miksi sen ajan näkymillä tuo liikevaihtoennuste olisi ollut huolimaton? Mielestäni hyvän keskustelukulttuurin ylläpitämiseksi analyysin kritisointia esim. huolimattomuudesta olisi hyvä perustella jollain muullakin kuin mutulla. Erityisesti syklisessä kasvuyhtiössä olisi myös hyvä muistaa että liikevaihtoennusteiden tekeminen monen vuoden päähän on aikalailla arpapeliä, ei analyytikot mitään selvännäkijöitä ole ja sellaisen odottaminen analyytikoilta on mielestäni kohtuutonta. Siksi peräänkuulutan sitä että jos analyysin laatua kommentoidaan niin siihen olisi hyvä olla perusteet ja varsinkin sen ajan näkymillä kun analyysi on tehty.

Eikö tämä 54m liikevaihtoa vuonna 2026 ole yhtiön oma tavoite, eikä sillä ole mitään tekemistä Inderesin raportin laadun kanssa?

Kuten laittamassasi kuvassa todetaan,

NorrDigin kasvutavoitteet arvioiminen on tämän vuoksi vaikeaa ja epävarmuudesta johtuen omat liikevaihtoennusteemme ovat melko selvästi alle yhtiön oman tavoitteen.

Kukaan ei ole ennustaja, mutta ihan hyvinhän tuolla on oltu pallon päällä markkinan haasteista (riskit, jotka ylempänä linkattu).

Niin ei kai noita voi Inderesin syyksi laittaa, mutta hiukan harhaanjohtavia ovat joka tapauksessa. Kukahan noiden raporttien/markkinointimateriaalien sisällön laadusta vastaa? Sijoittaja, jonka pitää ymmärtää ja suodattaa sisältöä riittävästi tehdäkseen oikeita johtopäätöksiä. Seurataan tilannetta😊

Perinteisen sylinteriliiketoiminnan markkinat on rajalliset ja keneltä tuo markkinaosuus otetaan ja millä keinoin. Raudan koneistus ja materiaalit ei anna paljoa liikkumatilaa olla ylivertainen. Velaton yritys voi painaa hintatasoa, mutta muutoin ainakin suomessa valmistajat ovat lienee samalla viivalla: Hydroline, Wipro, Hydoring, Norrhydro,…

Kun noita yhtiöraporttien arvostustaulukoita selailee ja jos niissä Inderes veikkaa osakkeen arvostuksen (20.4.2022) 3,77 eur vuodelle 2025 ja nyt korjatussa raportissa (21.2.2025) 1,48 eur niin onhan niissä huikea heitto. Ainakin näin maallikosta.

”Vastuuvapauslauseke sitten takaa raportille syyntakeettomuuden”

Hyviä analyyseja, mutta onkohan analyytikkoa vietyn noissa lähtötiedoissa/ennusteissa Norrhydron puolelta niin kuin litran mittaa jossakin mielessä🤔

Onhan tässä matkanvarrella ollut aika paljon vastatuulta talous- ja maailmatilanteessa. Tuotteiden kaupallistaminen on ollut yllättävän hidasta. Nyt kun asiat eivät ole menneet lähellekkään niin kuin vuonna 2022 suunniteltiin yhtiö on joutunut rahoitustilanteeseen, jossa on hyvin vähän liikkumavaraa. Tuo tiukkarahoitustilannehan tuon pörssikurssin painaa alas, koska kohta sitä osaketta dilutoidaan jos tuo rahoitustilanne ei kohta parane. En tiedä minkälainen oraakkeli olisi pitäny olla että olisi kaiken tämän voinut ennustaa? Yllätykset kuuluvat sijoittamiseen.

Kurssimuutosten ihmettely ei varsinaisesti ketjuun kuulu, mutta onko tiedossa jotain mikä on viime päivinä kurssia vahvasti nostanut? Vai onko taustalla vaan Saksan investointipaketti ja Norrhydro mahdollisena hyötyjänä? Ihmetellyt mikä tätä nyt nostaa.