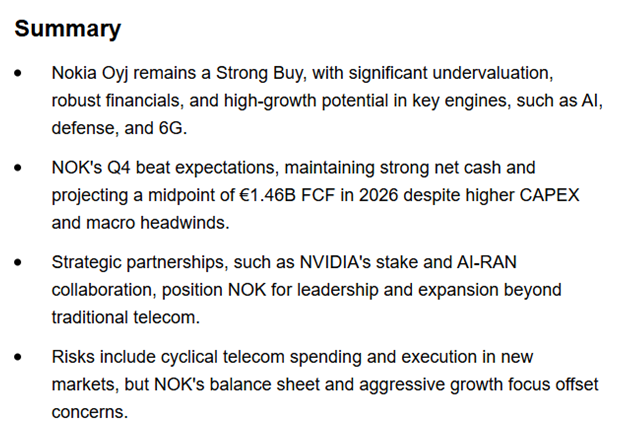

I’ve had some time to digest the results and guidance, and to think and connect the dots. Based on that, I’ve run old discussions through AI to find common threads, looked at what competitors have said, and how everything ties together. I’m writing a bit based on that.

My main focus is naturally on optical and IP networks, where major changes will occur in the coming years. This is a business with massive potential, which is why all the analysts were asking so many questions. But the pieces haven’t quite fit together yet – and I believe some insights have been missed.

First of all, the starting point is that 2026 is more of an investment year, where future profits won’t be fully realized yet. The schedule is somewhat flexible, however, and Q4/2026 is already a possible quarter for new revenue. Nokia has stated several times that component production won’t be at 2026 levels yet – and here lies one possibility for a positive scenario. Of course, one quarter isn’t the biggest thing in the world. However, what I think is likely is that in 2027, the 2028 target figures will already be reached – and this is not yet in analyst forecasts. This is based on component production.

Below is a neutral summary compiled by AI of what Nokia shared during the 11/2025 CMD (Capital Markets Day).

1. AI and Data Center Optical Business

- Nokia is developing intra-data center optical components aimed at achieving up to 80% lower power consumption in GPU-to-GPU traffic.

- This is in a very early stage:

- Not included in 2026 forecasts

- Test chips and design are underway

- A completely new SAM (Serviceable Addressable Market)

- Volume potential: 5–10 million units per year, a significantly larger scale than traditional optics.

- Nokia utilizes vertical integration: in-house chip and component manufacturing.

2. Indium Phosphide (InP) and Manufacturing Capacity

- Nokia (as part of the Infinera heritage) owns an InP laser fab in Sunnyvale.

- A second fab in San Jose:

- Construction started ~2.5 years ago

- Capacity will increase 25-fold

- Operational use at the start of 2026 (though there was talk in the Q4/2025 earnings call about later in 2026 or towards the end of the year) – I wonder why the timeline has been stretched a bit?

- Investments: Hundreds of millions of dollars, not billion-dollar fabs.

- The project has received support from the U.S. CHIPS Act.

- The fab is suitable for:

- High-power lasers

- Optical array solutions

- CPO (Co-packaged Optics) and LPO (Linear-drive Pluggable Optics) applications

- Fab utilization rates are rising, but figures are not reported.

3. Photonic Integrated Circuits and Packaging

- Nokia, or rather Infinera, invented the Photonic Integrated Circuit (PIC).

- PICs are packaged into Tx/Rx optical modules:

- 800G packaging in Allentown, Pennsylvania

- Optical packaging is seen as strategically critical, especially for managing supply chain risks.

4. DSP Expertise and R&D

- The Nokia-Infinera combination now has:

- The world’s largest and strongest coherent DSP (Digital Signal Processor) teams

- Hyperscalers require:

- New DSP generations every 2 years

- Previously in the telco market, the cycle was 4–5 years

- Targets: better dollar/bit and watt/bit.

5. Optical Systems and Pluggables

- Traditional optical system market: 3–4% growth.

- Nokia’s faster growth:

- In optical systems sold to hyperscalers

- In the coherent pluggable module market

- Pluggables:

- Co-developed with two hyperscalers

- Support probabilistic constellation shaping

- Range up to ~1,700 km

6. Component Business in Data Centers

- Opportunity to sell stand-alone PIC components (not the entire system).

- Application: e.g., 1.6 Tb/s GPU interconnects inside data centers.

- Advantages:

- Smaller inventories

- High margin

- Supports NI’s (Network Infrastructure) 300–700 bp margin expansion target

- Not yet included in forecasts.

7. IP Networks and Switching

- Nokia emphasizes the synergy between IP and optics:

- In-house IP chipset (FP, FPCX)

- Aggregation, BNG (Broadband Network Gateway), and cell site routing

- In data center switching:

- Still many 800G ports, transition to 1.6T is only just beginning

- Extremely high port densities (e.g., 576 x 800G)

- Nokia offers both the switch and the pluggable in the same solution.

8. Status of the Infinera Acquisition

- Combined roadmap is ready, customer feedback is very positive.

- No observed dyssynergies; delivered more than expected.

- North American backlog: +40% YoY.

- Synergies:

- Ahead of schedule

- Investments are being directed toward growth areas

This is what was stated then, and now we have received a lot of new information.

Here is a summary of the new information:

- The new InP fab (California, CHIPS Act support) will come online in late 2026, with the volume ramp mostly in 2027, and some already earlier.

- Current factory capacity is insufficient; the 25x capacity of the new factory is needed.

- 2026 CapEx is €900–1000M, which is nearly double previous levels, and this isn’t expected to be a “one-year spike.” This relates to optical networks, in-house photonics (PIC/InP), and scaling manufacturing.

“We think we’re favorably positioned with our indium phosphide technology and manufacturing facility.”

This is how you act when you already know you’re a critical part of the future architecture but can’t say it directly. The new info from the earnings call doesn’t change my views; it gave the impression that things have progressed favorably. Heard’s previous technical and strategic framework regarding InP, PIC, and the AI-optical market is now supported by: the 2027 timeframe, a concrete CapEx level, and the recognition of the InP competitive advantage. But indeed, 2026 is not yet the year for the bottom line – it could, however, be the year for the stock price if this development becomes clear earlier.

Most likely, Nvidia is Nokia’s partner in this matter, so now we wait for when more will be revealed. If Nokia is involved with optical components in the Rubin architecture, millions of components will go there.

David Heard said at the CMD, holding an ICE-D component in his hand:

“I know you can really see this, right? There is a chip in my hand to lower power 80% inside the data centers.”

Meanwhile, Nvidia announced that the new Spectrum-X Ethernet Photonics switches (which are based on the Spectrum-6 chip and use CPO technology) offer a 5-fold (i.e., 80%) improvement in network energy efficiency compared to traditional Ethernet. As far as I know, none of the competitors have spoken about such a percentage – Broadcom, for example, has apparently mentioned 65%.

At the CMD, Heard promised a 300–700 basis point (3–7%) margin improvement for the NI unit for 2028, stating it would come from components. The exact words were as follows:> David Heard (President of Network Infrastructure, Nokia): They wanted to be able to have certain software parameters on their pluggable. We deliver these pluggables can go kind of up to 1,700 km, so they can be used for all different applications depending on distance. Again, each win you do here is a couple of hundred million annually. The ability for us to get into components, this is not a win. This is a design example of using our component for 1.6 Tb inside the data center to lower the cost, to lower the power of the GPUs. Each deal like that could be, again, hundreds of millions annually. What Marco really likes about this is that when we’re selling that, we’re selling just the photonically integrated circuit.

David Heard (President of Network Infrastructure, Nokia): In terms of inventories and ease, this is a great business, all accretive to the margins for the company, which helps us with that 300 basis points-700 basis points expansion in network infrastructure. In IP, I’m so excited because the next thing you plug a pluggable into is IP. On the access edge, this is a company that has the aggregation switching, the BNGs, number one, and cell site routing that, again, this platform is rock solid. Like in the optical domain where we have our own silicon, or in that case, indium phosphide, we have our own chipsets here too. Again, the FP series, the FPCX that helps power a huge amount of applications required as you get closer to the edge. Again, they tend to be very, very quality sensitive, very, very sensitive on the feature sets required. We then bring that into the IP edge and core.

To me, it sounds like they are talking about at least Nvidia’s Rubin platform. And it seems Nokia has these components included in its 2028 forecasts – but they might break through significantly as early as 2027. Nokia’s own guidance for NI (Network Infrastructure) states that the 9.8% operating profit in 2025 will grow to a 13–17% operating profit by 2028. With growing revenue, this means the 780 million operating profit will double – perhaps even more.

When you put the pieces together, I think the situation is truly compelling. In my opinion, Nokia is on track for an adjusted operating profit of about 3 billion as early as 2027. Consensus is currently forecasting around 2.5–2.6 billion.