Tuli tällainen uusi analyysi vastaan.

But Nokia isn’t just a telecom equipment vendor anymore—it’s building an end-to-end AI infrastructure platform that could dominate the network equipment market for hyperscalers and service providers over the next decade.

With Infinera integration progressing ahead of schedule, the NVIDIA partnership announced in Q4, and a backlog approaching EUR 1.1 billion, Nokia is positioning itself as the critical infrastructure provider for the AI supercycle.

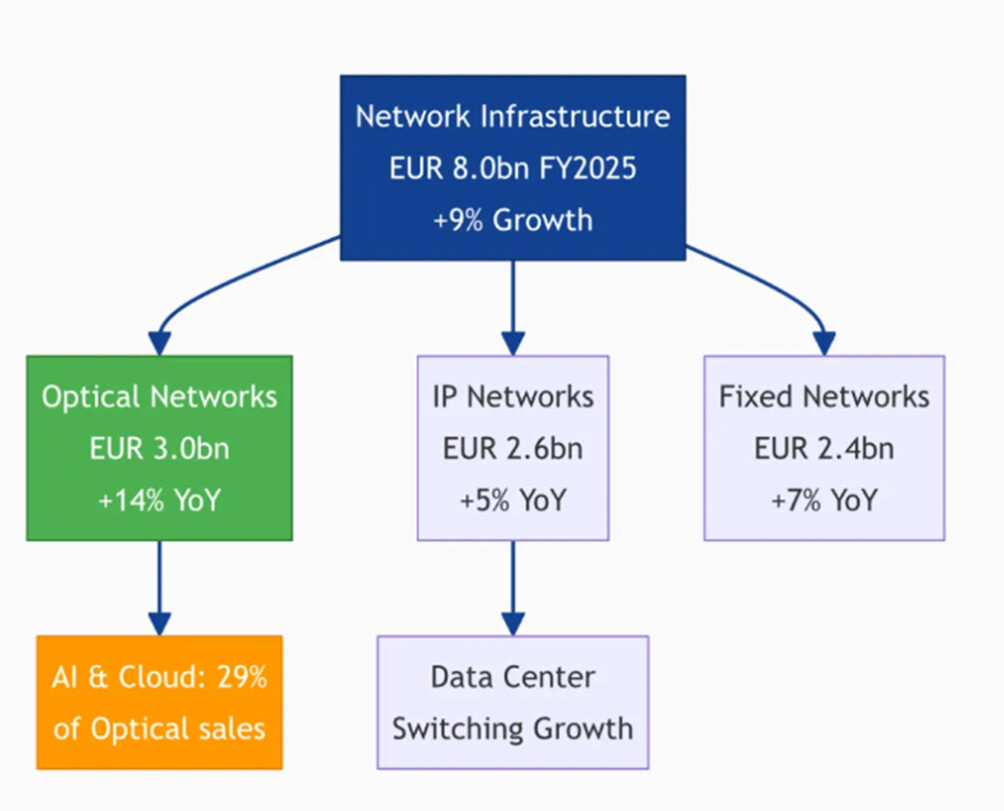

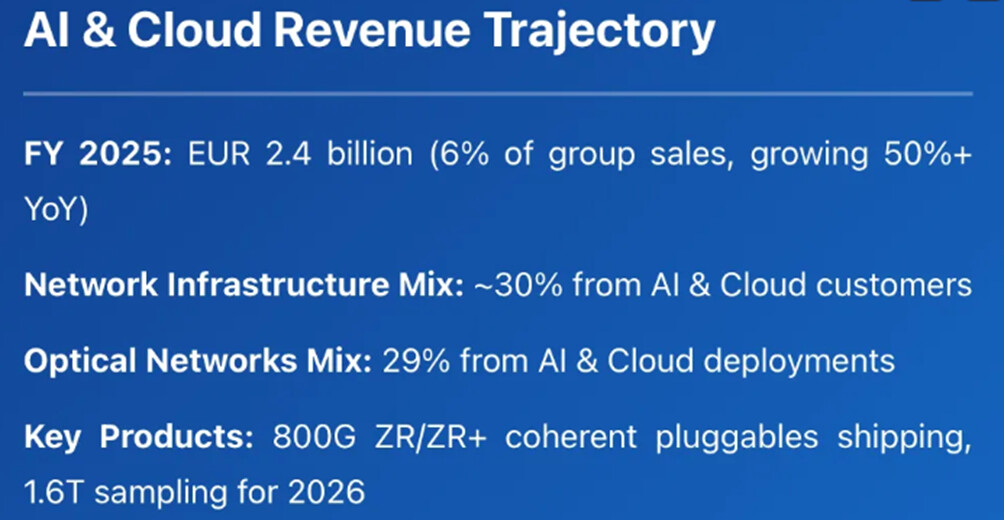

The AI & Cloud revenue story is the key unlock. Nokia generated EUR 2.4 billion from AI & Cloud customers in 2025 , representing roughly 30% of Network Infrastructure revenue. This is growing 50%+ annually as hyperscalers build out AI data centers and need optical transport to connect GPU clusters. The gross margins on these deals are superior to traditional telecom sales because hyperscalers value performance and reliability over absolute lowest cost.

Edit: @ruuki en alkanut tsekkaamaan onko luvut oikein. Ihan oikeista teemoista kuitenkin kirjoittelee.