En kyllä näe että miten tuo lisäisi realismia? Vuonna 2025 tiedotettiin 13kpl NBS 5 yhdistelmälaitteen kauppaa ja 3kpl NBS 6 yhdistelmälaitteen kauppaa. Uskoisin että tuon lisäksi Brainlabin alueelle on voitu tehdä lisää NBS 6 yhdistelmälaitteiden kauppoja joita ei ole tiedotettu.

Brainlabin myyntipumppu pääsee tänä vuonna jylläämään oikein kunnolla, sillä nyt syksyllä Brainlabin myynti on jo päässyt vaikuttamaan asiakkaiden vuoden 2026 budjetteihin. Uskoisin että tälle vuodelle laitehankintoja on budjetoitu jo useassa suunnassa, mutta tietoa clousaamisesta saadaan jäädä vielä odottelemaan.

Tarkoitin että yhdistelmälaitteiden myyntimäärän pois ottamalla esimerkiksi vuoden 2026 laitteistomyynnin kokonaismäärä olisi 41kpl. Vuonna 2027 44kpl ja 2028 55kpl.

Tällöin -5 - +12 laitetta toteutuneesta tarkottaisi vuonna 2026 36-53 laitetta. Vuonna 2027 39-56 laitetta.

Se mihin todelliset kauppamäärät asettuva tarkentuvat tulevaisuudessa. Ja mielläni päivitän myös omia näkemyksiä

Kiitos @Blindfolded_Monkey ideoista ja avusta taulukon stiliosoinnissa. Luettavuutta on parannettu ja lisäksi on lisätty CAGR-laskentaa oleellisiin kohtiin. Tuo CAGR havainnollistaa kyllä hyvin sen että aika maltillisella myynnin kasvulla tulosrivi kasvaa mukavaa vauhtia.

Tuo toistuva liikevaihto on kyllä hyvä tuottava ja vakauttava komponentti Nexstimissä.

Miljoonat ihmiset ja perheet elävät Alzheimerin taudin kanssa, menettäen arvokkaita muistoja ja yhteistä aikaa. Uusien hoitomenetelmien tarve ei ole koskaan ollut suurempi.

Sinaptica Therapeuticsilla kehitämme uudenlaista hoitomuotoa: ei-invasiivista, tarkkaa #neuromodulation on suunniteltu kohdistamaan ja palauttamaan häiriintynyt aivoverkosto, joka vastaa muistista, sekä parantamaan merkittävästi potilaiden elämää.

Tämä on tieteestä, jolla on tarkoitus. Teknologia, joka on rakennettu mittakaavaa varten. Ja syvä sitoutuminen muuttaa sitä, mikä Alzheimerin tautia sairastavien ihmisten mahdollisuuksia on.

Katso ja opi, miksi rakennamme Sinapticaa – ja minne olemme seuraavaksi menossa.

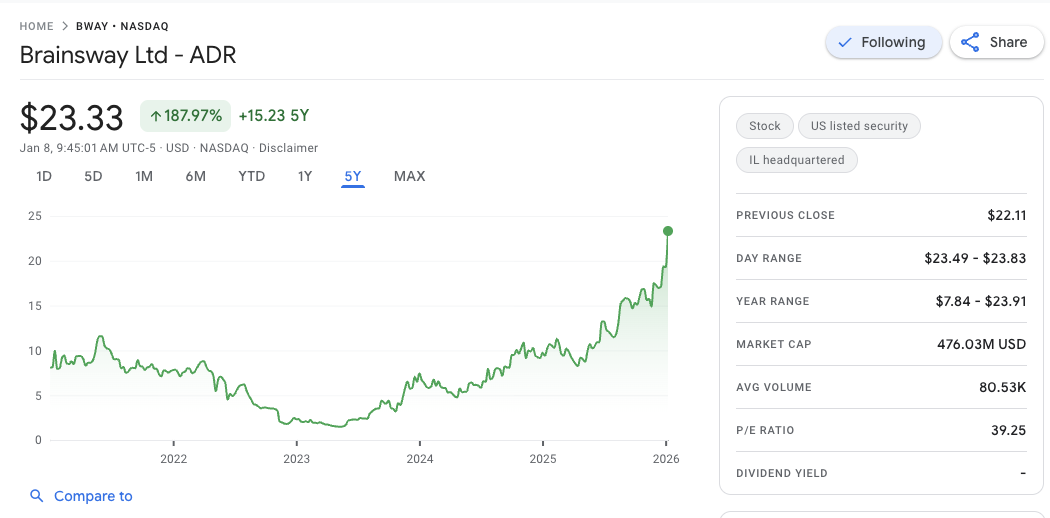

Update: Nyt kolkutellaan jo 500 miljoonan dollarin rajapyykkiä. Nexstimin alennusmyynnit jatkuu ja markkina-arvo pyörii vieläkin siellä 100 miljoonan kieppeillä.