Tästä olen hieman eri mieltä. Kyse on sen verran tärkeästä tutkimuksesta, että yhtiön pitää julkaista tulokset viipymättä, kun saavat itse tutkimustulokset tietoonsa. Tutkimuksen tekee kolmas osapuoli, eikä Nanoformin oletettavasti pitäisi tietää tulosta ennen kuin lopullinen tutkimuksen tulos heille ilmoitetaan. Tulokset ovat toki n. kuukauden myöhässä, joku viisaampi voi kertoa kuinka tyypillisiä kuukauden myöhästymiset ovat lääketutkimuksissa.

1 tykkäys

Eikö ne tulokset viimeksikin (fastes state) tulleet q2 osarin yhteydessä? Vai muistanko väärin. Mun mielestä innostavia tuloksia on jaeltu lehdistötiedotteilla ja vähän kädenlämpöisiä kuten näitä maakohtaisia partneroitumisia osarien yhteydessä…

1 tykkäys

Totta, näinhän se oli että tuloksen yhteydessä tulokset annettiin. Ehkä on sitten mahdollista, että tulokset olisivat jo tiedossa ja ne julkaistaisiin vasta Q4 raportin yhteydessä. Pidän tuota kuitenkin vähän erikoisena sekä sääntelyn että yhtiön viestinnän kannalta, mikäli heillä olisi lopulliset tulokset mutteivät julkaisisi niitä markkinoille. 1) Kyseessä on yhtiön arvon kannalta merkittävä sisäpiiritieto, sillä onnistuessaan tutkimuksen tulos tarkoittaa hyvin suurella todennäköisyydellä, että nanoenzalutamidi todella pääsee markkinoille. Tämä myös samalla on viimeinen todiste teknologian toimivuudesta. 2) Miksi yhtiö kertoisi tulosten olevan tulossa vuoden lopulla, mikäli eivät aio julkaista niitä ennen Q4 raporttia?

Toivottavasti kysymyksiin saadaan pian vastauksia.

8 tykkäystä

“Neuvottelujen tuloksena irtisanotaan 49 työntekijää. Lisäksi osalle jäljellä olevasta henkilöstöstä Suomessa voidaan toteuttaa määräaikaisia osa-aikaisia lomautuksia 1. maaliskuuta 2026 alkaen. Lomautusten kesto voi olla enintään 6 kuukautta. Näillä toimenpiteillä yhtiö odottaa saavuttavansa noin 5–6 miljoonan euron kustannussäästöt kalenterivuodelle 2026.”

10 tykkäystä

9 tykkäystä

Nyt on muuten hyvä mini-![]() uutinen. Jos tuo SC Nanotrastuzumab antaa Herceptin HYLECTA:aa vastaavat AUC, Cmax ja Tmax arvot possuilla, lähtisin siitä oletuksesta, että myös ihmisillä on syytä odottaa vastaavia tuloksia. Nyt kai kyse on siitä, millä aikataulullla biolinja saadaan GMP tasoon ja koska ihmiskokeita päästään aloittamaan.

uutinen. Jos tuo SC Nanotrastuzumab antaa Herceptin HYLECTA:aa vastaavat AUC, Cmax ja Tmax arvot possuilla, lähtisin siitä oletuksesta, että myös ihmisillä on syytä odottaa vastaavia tuloksia. Nyt kai kyse on siitä, millä aikataulullla biolinja saadaan GMP tasoon ja koska ihmiskokeita päästään aloittamaan.

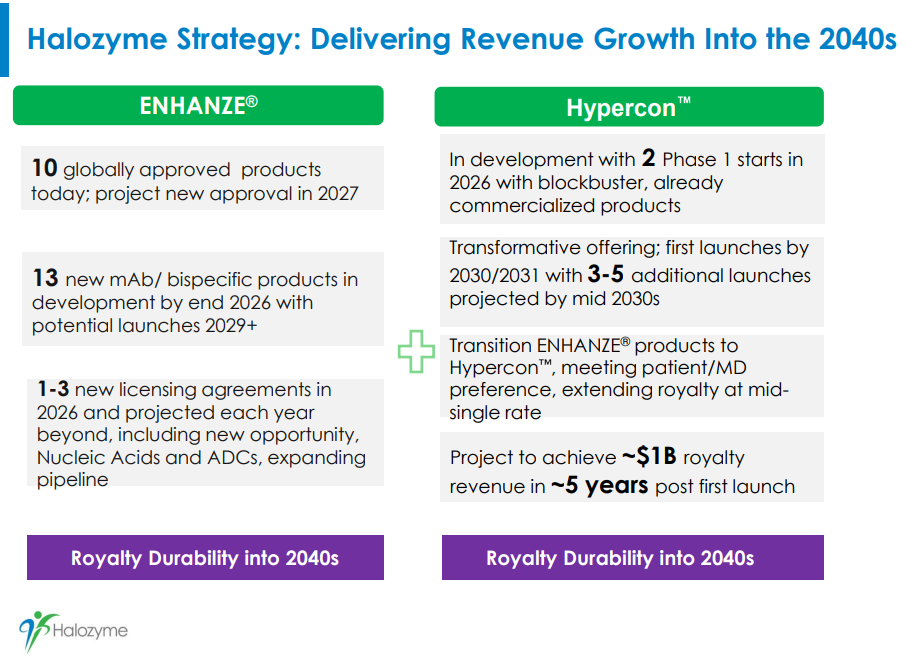

Tässä vielä viitteeksi Halozymen projektiot noiden hankkimiensa Hypercon menetelmien tuotoista (kopioitu Halozymen presentaatiosta täältä).

Kävin vielä katsomassa ketkä tätä myyvät tällä hetkellä, ja Handelsbanken, Danske ja S-Pankki olivat suurimpia myyjiä tammikuussa. S-Pankki nyt poistunut top 25 listalta.

edit: Lisään tämän vielä tähän trastuzumabin markkinaan liittyen. https://www.polarismarketresearch.com/industry-analysis/herceptin-biosimilars-market

" The Herceptin Biosimilars market size was valued at USD 2,711.22 million in 2024. The market is projected to grow from USD 3,325.31 million in 2025 to USD 21,271.43 million by 2034, exhibiting a CAGR of 22.9% during 2025–2034."

Ja tietenkin jos tämä toimii yhdellä vasta-aineella, seuraava hyvä kandidaatti voisi olla Pembrolizumab, jonka patenttien takaraja tulee vastaan 2028. Pembron vuosimyynti on tällä hetkellä luokkaa 30 Mrd USD.

15 tykkäystä

Yritys voisi kyllä kommunikoida vähän ripeämmin ja selkeämmin, miten nanoentsalutamidin asiat etenevät. Kyseessä on kuitenkin sijoittajien ajatuksissa erittäin tärkeä asia, koska lähitulevaisuuden kassavirtaoletukset ja rahoitustarpeet kytkeytyväy niin vahvasti tähän. Hiljaisuus ei auta, kurssista päätellen hiljaisuuden jatkuessa useampi ja useampi sijoittaja ei uskalla kantaa riskiä? Kommunikoisivat nyt ihmeessä, missä mennään…

8 tykkäystä

Ensiviikon torstaina varmaan lisää tietoa. Voi olla, että siihen asti valutaan hitaasti alaspäin, kun hesulin biofirmoja nyt viimeaikoina on myyty aika roimasti.

10 tykkäystä

Eipä akkiseltää isoja yllätyksiä. Juna puksuttaa etiä päin. “The fed study results support the previous fasted results and Nanoform and the ONConcept® consortium’s assessment is that the results are supportive for nanoenzalutamide to progress to the markets underpinned by an adjusted regulatory strategy.”

8 tykkäystä

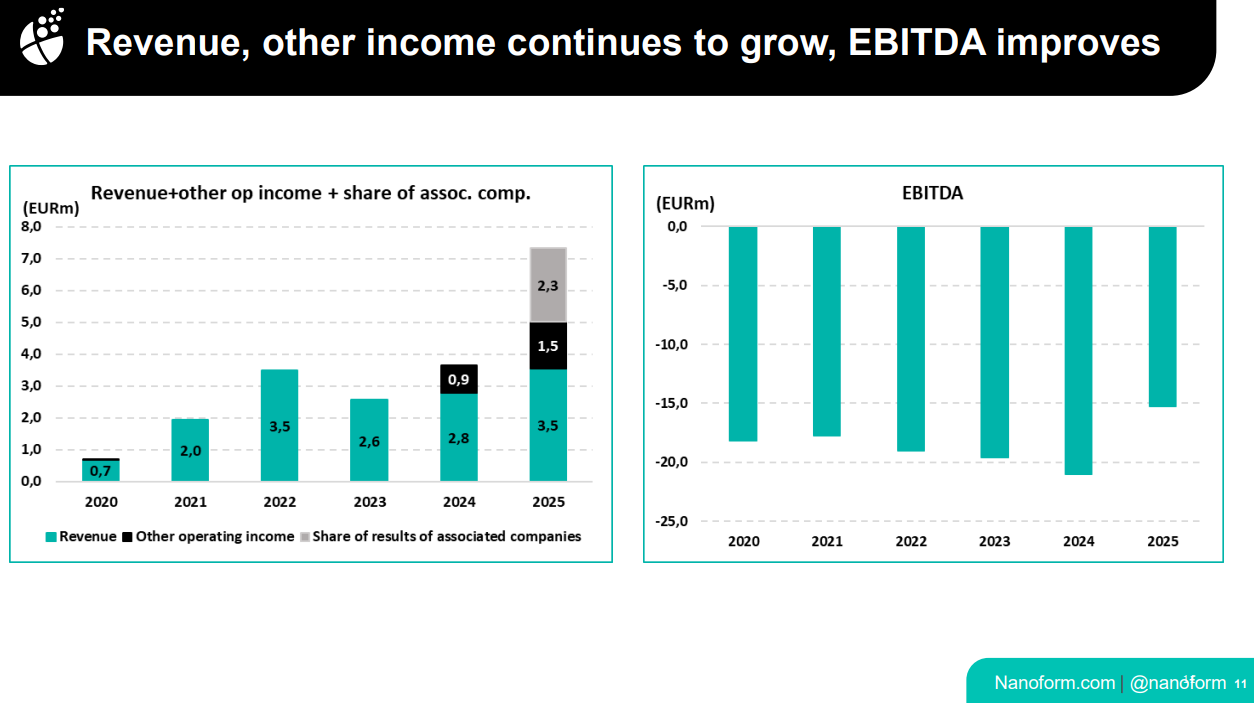

Äkkiseltään yhtiöllä on kassavirran kulutukselle asetettu taso alle 10M€ v2026 ja tavoitellaan 50% LV kasvua - mutta vain 5% kulujen kasvua. Käänne voisi tulla 2026H1, jos kulut pysyvät tasaisina, mutta LV alkaa nousta kohti 5-10M€/Q.

Kliinisen valmistukset tuovat jatkuvaa tuloa, ei tutkimustoiminta. Kärkituotteen eturauhassyöpälääkkeen markkinoilletuloa ymmärtääkseni tavoitellaan v2028, joten siihen on vielä aikaa.

Yhtiöllä on jo ikää, olisiko 2026 jo jonkinlainen läpilyöntivuos, joka näkyisi arvostuksen kasvuna? Milloin skaalautuvan liikevaihdon uskottavuuden hetki on käsillä?

4 tykkäystä

Ei kannata antaa kasvuprosenttien liiaksi hämätä. Yhtiö ei mielestäni pörssihistorian aikana ole ollut näin epävarmassa tilanteessa. 3,5milj liikevaihto muodostui 53 projektista eli pöhinää R&D puolella edelleen riittää, mutta projektit on hyvin pieniä ja mikään näistä ei ole pörssihistorian aikana vielä konvertoitunut tuotantoon saakka.

Oma käsitys pitää pitkälti muodostaa irrallisten tiedonmurusten varaan ja mielestäni irtisanomisilla on suuri informaatioarvo. Se on totta, että kovan ylösajon vaiheessa voi tulla virherekryjä ja tarvetta rakenteellisille muutoksille, mutta jokainen voi miettiä mikä startup vapaaehtoisesti irtisanoo 30% työntekijöistä ja lomauttaa loppuja jos asiat sujuu suunnitellusti (kuten firma pääasiassa on viestinyt), varsinkin kun edellisen strategian keskiössä oli työntekijämäärän kasvatus! Tilinpäätöksessä TJ syytti puolustusteollisuuden investointeja niukoista lääkekehitys investoinneista, mutta onhan noita R&D projekteja edelleen käynnissä kuten ennenkin. Miksi mikään näistä kymmenistä/sadoista prjekteista ei ole kehittynyt markkinoille asti.

Ulkopuoliselle näyttää siltä että isojen irtisanomisten jälkeen focus on entistä enemmän R&D projekteissa ja tuotanto on entistä kauempana. Voi vain kuvitella mikä on lomautettujen pysyvyys jos oletettavasti lomautukset koskevat tuotanto puolta ja sielläkin varmaan on koulutettua väkeä töissä, jolle on kilpailijoillakin kysyntää.

Propsit kuitenkin siitä, että yritetään ja tehdään vaikeita päätöksiä (YT), mutta sijoittajien on hyvä pohtia riittävää riskipreemiota tämän yrityksen kohdalla.

6 tykkäystä

Aika aikaa kutakin, sanoi pässi kun päätä leikattiin. Aiemmin taisi olla keskustelua siitä, kun jokin tuotteen tai aihion kehitystyö on edennyt riittävän pitkälle, niin silloin ei tarvita enää samaa porukkaa jatkoon vähään aikaan. Tämä kävisi hyväksi selitykseksi noille työsuhteiden päättämisille. Ovat kuitenkin olleet nähtävästi toistaiseksi olevissa työsuhteissa eivätkä prekaaria pätkätyöläisiä.

Sitä en kyllä tiennytkään, että tutkimusryhmiä ja siten Nanon sisäisiä startuppeja on noin paljon eikä firma olekaan noiden harvojen tai yhden vahvan tuotteen lanseeraamisen varassa. Jokin raja sitten tullut vastaan, jos noiden irtisanottujen osaamista ei voida hyödyntää uusissa tai varhaisemmissa kehitysvaiheissa olevissa projekteissa. Onko kysyntä ja tuon asiantuntijuuden potentiaalit siis loppuneet.

Ehdittekö Jerej ja muut katsoa/kuunnella jo investor callia?

Minä kuuntelin tänään autoa ajaessa, kalvoja en siinä voinut katsella.

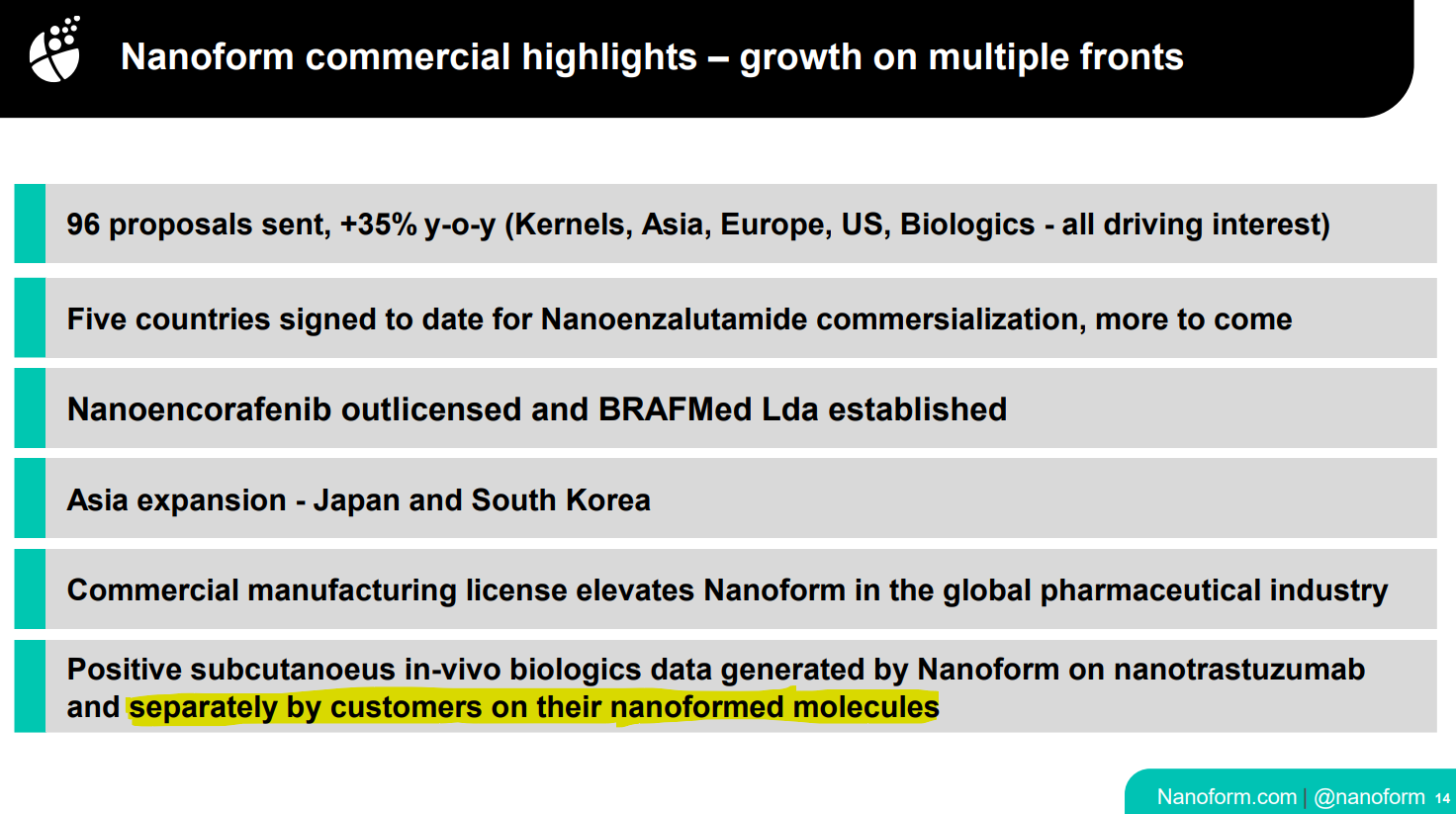

Se mikä oli innostavaa, ja minkä jerej meille kertonut aiemminkin, on tämä nanoformuloinnin mahdollisuus s.c. biologisissa lääkkeissä. Possutestin positiiviset tulokset ja Takedan kuvaukset, miten mukavasti materiaali käyttäytyy injektioneuloissa.

Mutta menikö minulta jotain ohi, vai eikö nanoentsalutamidin ihmiskokeista sanottu muuta, kun että nyt on tutkittu fasted ja fed state, työstetään myyntilupahakemuksen jättämistä (ilmeisesti vain EMA tässä vaiheessa?) q2:lla ”adjusted” strategialla (tai mikä se sanamuoto nyt olikaan) ja tähdätään myynnin alkamiseen Euroopassa kesällä 2028. Eikö USA:sta puhuta enää mitään? Muutamassa EU-maassa (oliko nyt 5?) on saatu yhteistyökumppani ja yhdessä ei-EU-maassa.

Hyvin epämääräistä ja hitaasti kehittyvää tämä nanoenzalutamide-osasto, tosi niukan kommunikaation varassa meitä pidetään.

Nanoenzalutamide kytkeytyy tässä yrityksen lähivuosien rahoitustilanteen pohdintoihin. Kassaa oli 24 vai 26 miljoonaa jäljellä. Alle 10 milj vuosipolttoon tähdätään tänä vuonna. Vieläkään ei vissiin ole tullut kernelien ulkopuolelta (liikevaihtoa tuottavaa) GMP-toimintaa? Ei-GMP tuottaa hiluja. Pysyäkseen uskottavana toimittajana, yritys ei voi kassaa nollaan, nanoenzalutamiden myyntiin on melkein 2,5 vuotta ja täällä on epäilty sen lähtevän kuitenkin hitaahkosti käyntiin.

Peter vastasi biologisten mahdollisen GMP-linjan suhteen - siitä kun päätös aloittamisesta tehdään, menee n. 24 kk tuotantoon.

Tuntuu, että yrityksen taloudellinen tilanne alkaa olla 2-3 v tähtäimellä aika huolestuttava, ja pääomaa joudutaan hakemaan ehkä nykyomistajien kannalta ikävän matalalla arvostuksella?

3 tykkäystä

Kuuntelin tuon webcastin eilen. Voin viikonlopun aikana avata omia mietteitäni. Tuossa tämän vuoden arviossa cash burnille (noin -10M€) ei toimitusjohtajan mukaan ole laskettu etappimaksuja. Johto ei varmaan halua ennustaa niitä tälle vuodelle, kun niiden ajoitus lienee epävarmaa, mutta mikäli niitä tulee tuo tulos joustanee kai lähinnä ylöspäin. Nanoenzalutamidin myyntilupahakemuksen jättö pitäisi kai olla vielä tämän vuoden puolella. Jos se viivästyy, vaikeutuu firman rahoitustilanne kyllä. Tosin nykyisellä cash burn ratella kassan pitäisi riittää vielä 2 vuotta eteenpäin. Olettaisin nanoenzalutamidin etappimaksujen olevan myös sidottuna tuohon myyntiluvan saantiin.

Tuo associated companies tulo (harmaa palkki) lienee BRAFmedin allekirjoitusmaksuista tullutta. Nämä on johdon mukaan luokkaa low single digit million, joka sopisi tuohon. Nuo mustat palkit liittynevät enimmäkseen nanoenzalutamidiin, josta Nanform omistaa 25%.

8 tykkäystä

Handelsbanken funds oli vielä viime kesänä suurin omistaja reilulla 6milj. osakkeella. Nyt jäljellä reilut 3milj.

Kysymys kuulukin. Johtuuko nämä myynnit nyt siitä että S-pankki osti handelsbankenin suomen toiminnot? Itse pähkinyt että olisi jotain suurempaa mutta sitten tuli tuo kauppa mieleen. Hiukan helpottaa ajatusta yhtiöstä ja onhan sitä kaupassakin iloinen kun saa kahvipaketin halvalla.

1 tykkäys

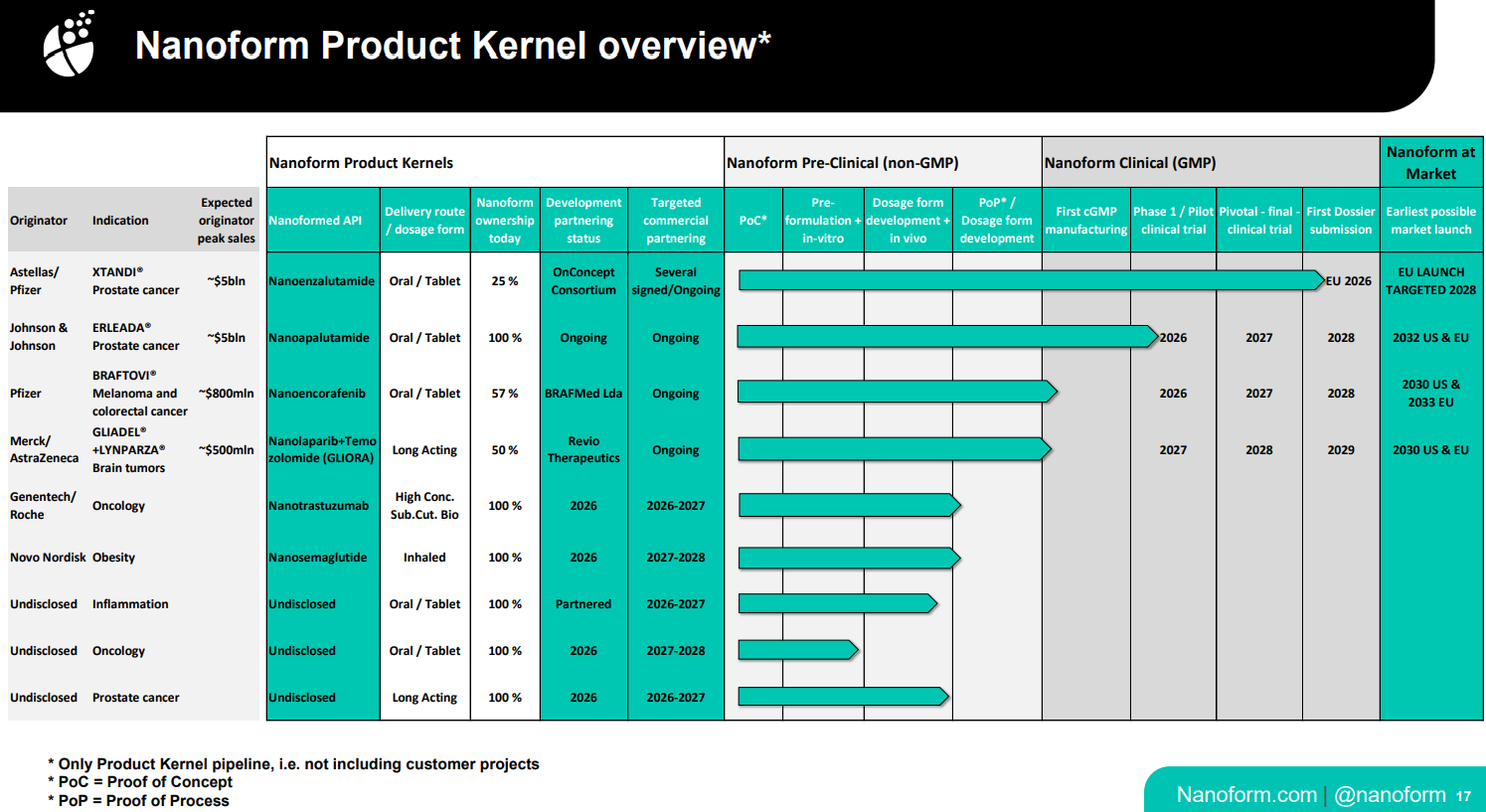

Tämä on hankala firma arvioida lyhyellä tähtäimellä, kun niin iso osa potentiaalista on riippuvaista asiakkaiden kanssa thetävistä projekteista, joista ei ymmärrettävistä syistä voida kertoa paljoa vielä ulospäin. Jos näistä olisi saatavilla esimerkiksi tietoa projektien lääkeaineiden kliinisen vaiheen jakaumasta, auttaisi se jo näiden arviointia. Prekliinisen vaiheen aihio on paljon riskisempi kuin esimerkiksi jo hyväksytty lääkeine, jonka ominaisuksia halutaan parannella nanoformuloimalla. Tällä hetkellä joudutaan menemmään arvioissa pääasiassa vain jo julkaistujen omien product kernelien mukaan, joka kuitenkin pitkällä tähtäimellä aliarvioi potentiaalia.

Tässä on tuo product kernel lista esityksen slideista:

Näistä nanoenzalutamidi on nyt pisimmällä ja sen tie eteenpäin on selvin. Tästä pitäisi jättää myyntilupahakemus tänä vuonna ja varmaan seuraavat etappimaksut liittyvät siihen. Tämä toteutuessaan jo mahdollisesti kääntää tuloksen positiiviseksi ensivuonna, mutta se vaatinee sen, että lääkeviranomaiset hyväksyvät eron Cmaxin välillä verrokkiin.

Seuraavana listalla on nanoapalutamidi, jonka ensimmäinen GMP bätchi oli tuotettu tiedotteen mukaan nyt joulukuussa. Tuossa listassa on merkitty partnering statukseen ongoing. Jos tämä diili saadaan sovittua, voisi jotain allekirjoitusmaksua odottaa jo mahdollisesti tänä vuonna, mutta ehkä parempi odottaa sen osuvan ensi vuodelle. Tässä voi tosin olla asiaa monimutkaistamassa, ja diilin sopimista hidastamassa, apalutamidin siirto Trumpin alennuslääkkeiden listalle, jolloin sen myyntipotentiaali laskee.

Nanoencorafenibin GMP tuotanto on tarkoitus myös aloittaa nyt tänä vuonna, ja tämän ja nanoapalutamidin ensimmäiset kliiniset kokeet olisi myös tarkoitus saada jo tänä vuonna liikkeelle.

Lisäksi tuolta listalta pistää silmään tuo inlfammation undisclosed kernel, jonka development partner status on merkitty partnered. Tästä voitaisiin kuulla seuraavaksi ehkä jotain.

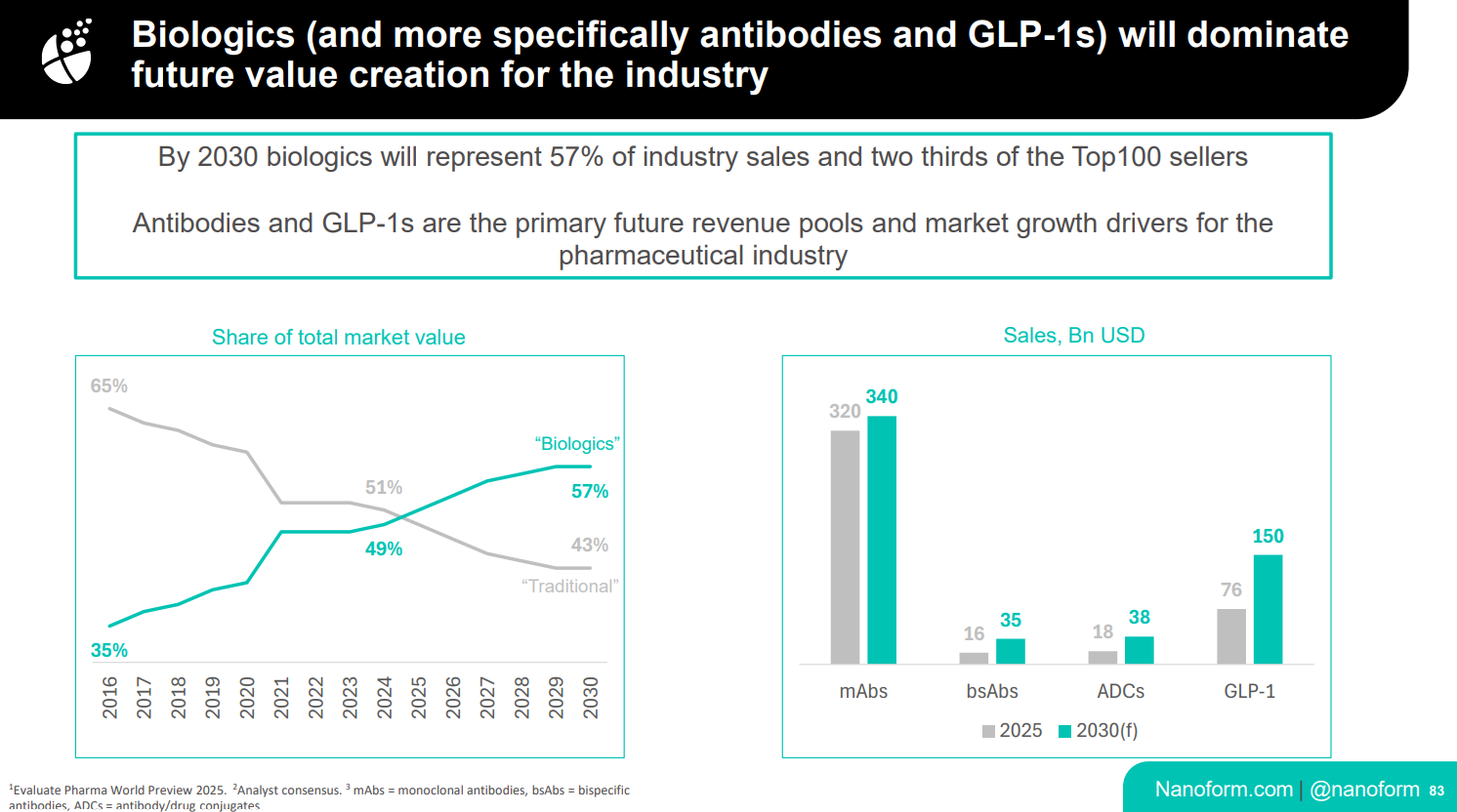

Pidemmälä tähtäimellä kysymys biologisten yhdisteiden nanoformuloinnista on erittäin kiinnostava firman potentiaalin kannalta. Tässä on kuva CMD:n slideista jossa tuo biologisten yhdisteiden osuus lääkemarkkinoista on esitetty.

Nyt ollaan siirtymässä tilanteeseen jossa biologisten yhdisteiden markkina muodostaa jo suuremman osan kuin perinteisemmät pienimolekylaariset yhdisteet. Tällöin mielestäni biolinjan / -linjojen tuotantokapasiteetti ja GMP status ovat merkittäviä ajureita tämän strategiakauden loppua kohden. Tästä syystä tulen kinnittäneeksi ehkä enemmän vielä huomiota näiden biomolekyylien kehityksen etenemiseen.

Tuohon edelliseen possukokeeseen liittyen, siinä ei oltu testattu vain nanoformin trastuzumabia in vivo oloissa, vaan lisäksi jonkin partnerin nanoformuloitua biomolekyyliä.

Paras veikkaus tässä vaiheessa lienee Takedan alfa-1 antitrypsiini, koska se on jo nimetty aiemmin muualla, mutta se voi tokin olla jokin muukin yhdiste esimerkiksi toinen monoklonaalinen vasta-aine.

Tämä lisäksi mainitsi tuossa vastauksessa, että tuo biolinjan muunto GMP tasoiseksi tullaan tekemään partnerin kustannuksella, jolloin siitä ei tule erillisiä kuluja firmalle. Tämän suhteen neuvottelut ovat tosin vielä kesken. Jos oletetaan, että neuvottelut saataisiin tämän vuoden aikana kasaan ja siitä GMP statukseen noi 24 kk, voisi GMP biolinja olla pystyssä joskus 29 paikkeilla.

Nyt ollaan siirtymässä vaiheesen, missä alun investoinnit on tehty ja kassavirta pitäisi saada käännettyä positiiviseksi. Mielestäni tuo on mahdollista 2027, mutta se tulee riippumaan vielä varmaan tämän viisivuotiskauden ajan kasvavista partnerointidiilien maksuista. Myyntiprovisiot vaikuttavat siihen todennäköisesti vielä kohtuu pienissä määrin, koska nanoenzalutamidin myynti voi aikaisintaan alkaa 2028 ja senkin potentiaalin saavuttamiseen menee vielä oma aikansa.

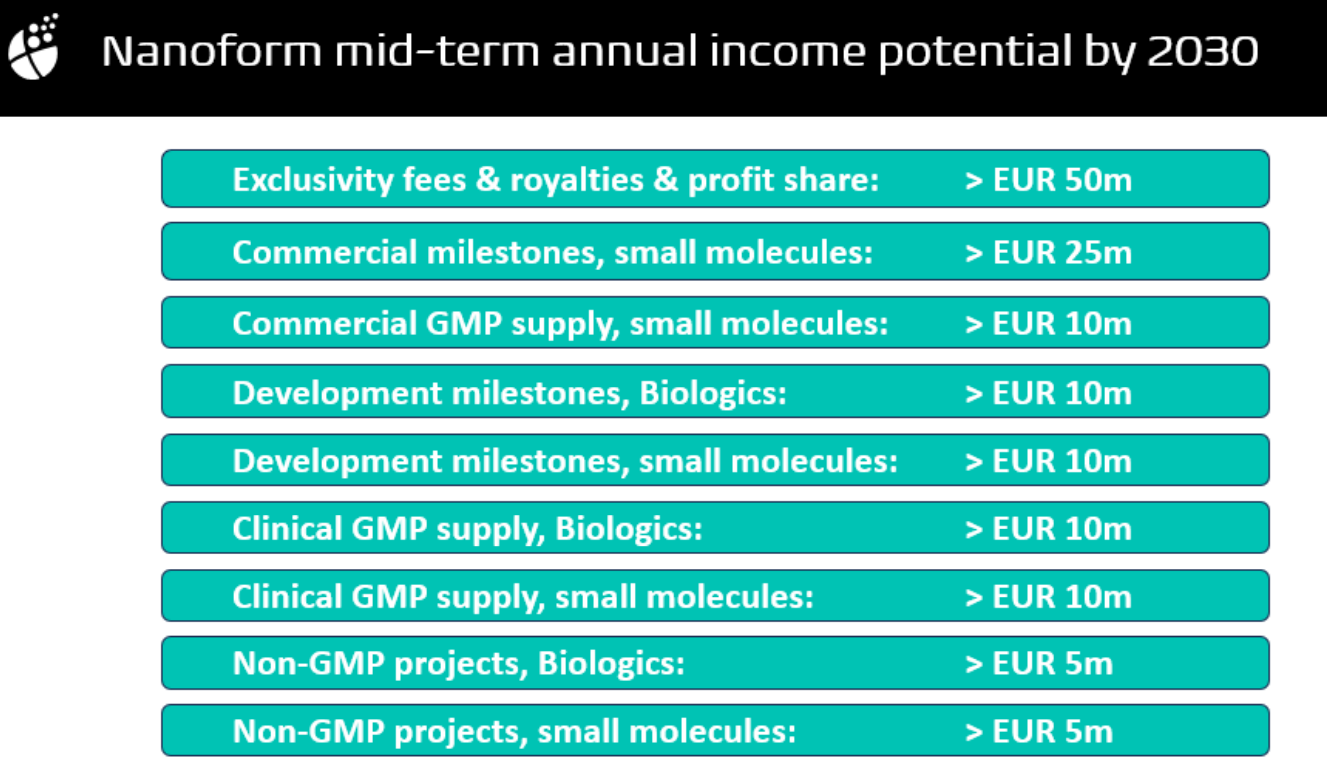

Firman omat arviot 2030 lopun potentiaalista löytyvät tuolta slaidien loppupäästä. Jos nämä toteutuvat, niin kyllähän tämä lopulta kääntyy ympäri, mutta aina tässä on pohjalla se ikuisuuskysymys kannattaako firmojen toimitusjohtajia kuunnella. ![]()

17 tykkäystä

Kiitos Jerej kattavasta ja monipuolisesti pohdiskelevasta vastauksestasi. Minun pitää lukea tämä sopivalla hetkellä ajatuksella, ja kuunnella myös webcast ihan slidet katsoen kanssa. Siellä on kuitenkin informaatiota.

Olisi niin paljon mukavampi tilanne, kun kassa olisi pullea, ja biologisten investoinnit kyettäisiin tekemään itse (tai eihän siinä ongelmaa ole jos tehdään muiden rahoilla, jos asia suht. viiveettä ja ihan oikeasti etenee.

Harmi, ettei paremmalla kurssitasolla otettu enemmän pääomaa sisään (tosin nykyinenkin kurssiluisu tuntui alkavan siitä edellisestä suunnatusta osakeannista). Mutta jälkiviisaus helppoa, yritys taisi toivoa nanoenzalutamidista helpompaa ja rahakkaampaa keissiä. Siellä kolmen euron hujakoillakin johto osteli osakkeita…

3 tykkäystä

Tämä summaa aika hyvin keissin tällä hetkellä. Itse ainakin vielä suhtaudun hyvin optimistisesti tähän. Kaikki ainakin toistaiseksi vaikuttaa etenevän, tosin ehkä se kaksi vuotta jäljessä sitä mitä alkuun on ajateltu. Ehkä moni muu on sijoittanut tähän lyhyemmällä tähtäimellä, mutta itse seuraan lähinnä miten tuo käänne kohti 2027:ää etenee. Siihen asti voin lisäillä näistä rahastojen myynneistä vähitellen. Putoavia puukkoja jne ![]()

Mielestäni nyt 2026 on hieman välivuosi ja todennäköisesti tuonne 2027 sitten osuu useampi noita etappimaksuja. Tämän vuoden aikana pitäisi tosin tulla lisää tietoa noista muista kerneleistä. Niistä aika moni on merkitty tuohon ylempään taulukkoon development partnering statukseen 2026. Nämä on niitä joiden tulisi sitten kantaa firmaa eteenpäin tuolla strategiakauden lopussa.

6 tykkäystä

Ainakin johtajien kohdalla luulisi olevan taas motivaatiota, kun juuri tuli infoa, että ovat kuitanneet ilmaiset optio-osakkeensa.

2 tykkäystä

Täähän se, mut siksi laitoinkin pelimerkit sisään kun pohjalta sitä pitää koittaa onkia.