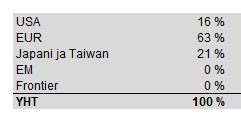

Europe’s large share is largely due to Harvia’s significant weighting. Emerging and frontier markets are pure zeros intentionally; the world is heading in such a direction that I’m not entirely sure about asset protection in those markets.

Finland and Helsinki over 99%. Sweden under 1%, as platform economy companies are not sold in Helsinki, but from Sweden, you can get a couple of dozen of them in the same package.

So Finland is over 99%, but calculated according to the stock exchange. The Finnish share of revenue is quite small, for example, for global players like Nokia. And as tax competition intensifies, Nordea might also become Swedish again at some point.

But right now, Juurikki only operates in Helsinki and regrets that there isn’t enough time to properly follow even a dozen Helsinki companies. The key figure-based screening seems to leave mostly the same companies for closer examination year after year. Boring. Boring.

When considering geographical diversification, it’s worth remembering that investments create economic activity, jobs, profits, and if there happens to be a supporting social order, also well-being.

We vote with our investments on where in the world we want good to be. Juurikki, for reasons of principle, does not support Russia’s war economy by investing in Russia, nor does Juurikki support communist China by investing in China. Guess if Juurikki supports far-right Trumpland in his/her investments. Hell no.

Mostly agree. I only invest in companies whose domicile is in at least a somewhat democratic country. This excludes Russia, China, Vietnam, etc. I disagree about Trump-land. There, however, the centuries-old system is stable enough that it won’t collapse because of one Trump, even if things sometimes look wild.

Otherwise, it’s entirely based on where the economy is predicted to grow in the future, for example, based on demographic development. That’s why Europe’s weight will still decrease somewhat in my portfolio.

I, on the other hand, leave such philosophizing out when making investment decisions. I aim for returns and well-being for myself, not for society. Furthermore, my tracksuit rustles so loudly that its societal significance is negligibly insignificant.

I operate in the same areas. One big reason not to invest in communist and/or dictatorial countries is that, in a so-called tight spot, ownerships can disappear overnight due to a political decision (socialization of foreign investors’ assets, etc.). Of course, there might be some warning signs beforehand, but at that point, when everyone rushes for the door, the stock prices collapse, leaving nothing.

I trust the property rights protection in so-called Western democracies, and I agree about the US that the system is ultimately stable, and especially property rights protection is one of the fundamental pillars of their system; I don’t believe it will be significantly undermined.

Securities account:

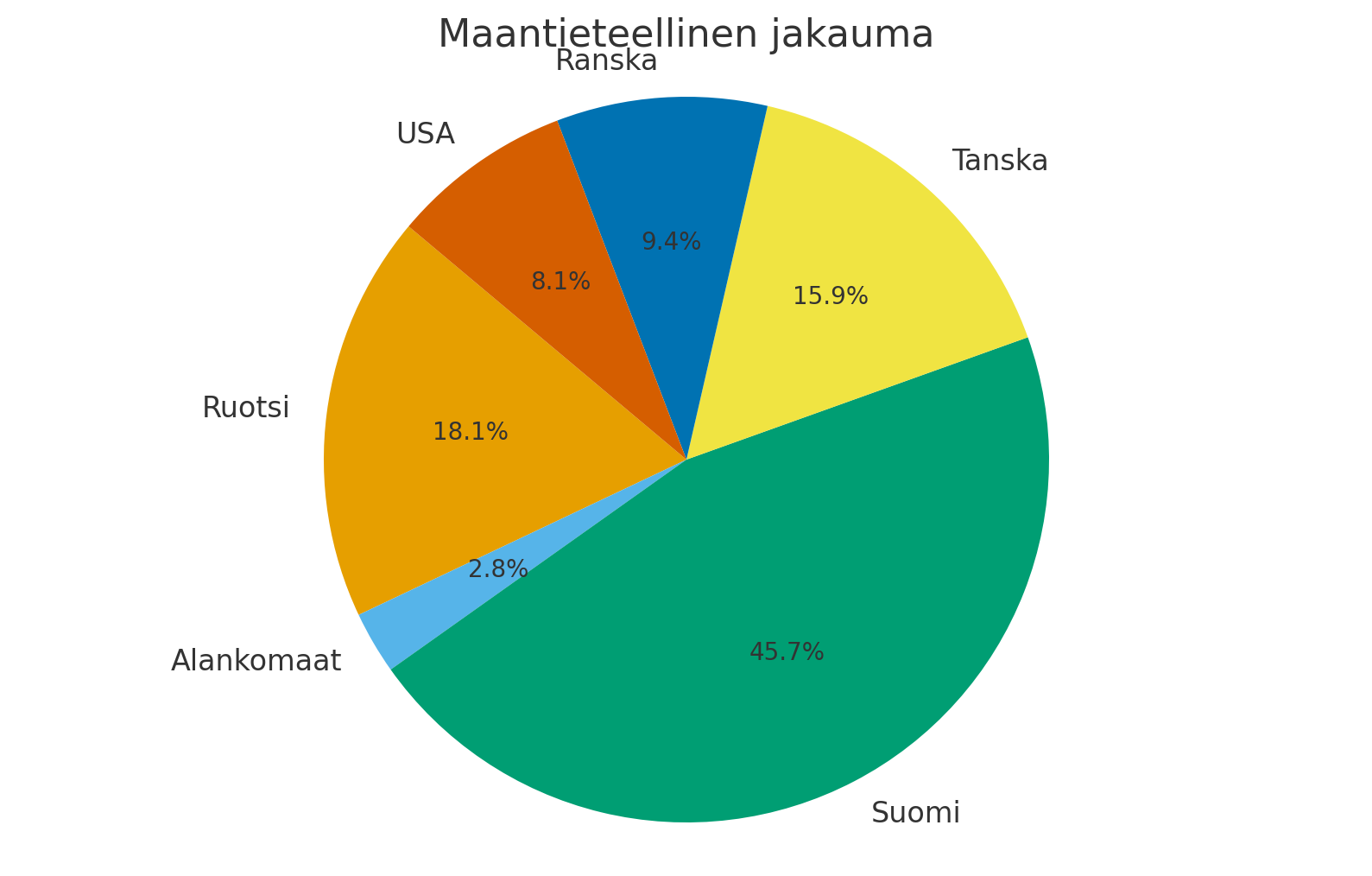

Finland 51.15%

World 30.03%

Europe 2.62%

Asia 16.2%

Share savings account:

Finland 100%

Overall:

Finland 69.37%

World 18.83%

Europe 1.64%

Asia 10.16%

The share of World, Europe, and Asia has grown systematically by a few percentage points and will continue to grow; automated monthly savings into all three index funds will ensure this. The current nearly 70% in direct Finnish stocks will decrease over time despite additional investments, as the wonder of compound interest accelerates.

The Finnish dividend payers in the share savings account are and will remain, with continued additions.

In my portfolio, I have 2 finance, 1 engineering company (main markets global, also part of production), 2 diversified (one global, one Finland, Baltics, Europe), 1 logistics (Finland - Baltic Sea), 1 purely domestic (service).

Portfolio construction continues. The domestic market should not be underestimated, as Finland lags behind in the economic cycle, and construction activity is likely to recover in late 2026. Part of the portfolio will consist of large domestic companies via an index fund. Through the fund, it has been observed that the returns of European funds have lagged behind even Finnish funds, and are very far behind US funds.

Big question: which companies will benefit most from the dollar’s future strengthening?

Completely agree. In my portfolio, the only concession towards Trumpland is still one ETF (Shares Nasdaq-100 UCITS ETF EUR Hedged), for which I have started looking for a replacement non-USA-weighted ETF (perhaps some Europe or Nordic index instead?)

There is already a huge overrepresentation for Finland, the Nordic countries, and Europe, if the intention is specifically to decentralize and not to centralize further.

Otherwise, owning a company’s operations does not support it in any way (unless it’s already an amount that influences decision-making); the only “support” one can give is participating in potential offerings. Of course, an investor may have other reasons to own or not to own something, but for the company itself, it doesn’t matter who holds the shares (of course, if its employees hold them, it fosters commitment, etc.).

In my own stock portfolio, geographical diversification is currently around 70% USA, 25% Sweden, and 5% Finland. If we expand the concept of geographical diversification to cover one’s entire life and assets, I’ve reasoned that since my entire life is otherwise in Finland, it’s good to keep investments mostly elsewhere in the world.

I don’t own an apartment yet, but at some point, I do intend to acquire one - at that point, the lion’s share of the total portfolio’s diversification will be in Finnish real estate. Why would I want to own any more Finnish risk in the form of stock investments at that point?

Finland risk can also be influenced in other ways than with a stock portfolio.

You can get a job in an export company where the domestic share of sales is small. In this case, Finnish economic cycles do not significantly affect it, but those of, for example, China, Germany, and the USA do.

You can acquire domestic assets whose value is determined by global end-product demand (e.g., forest).

You can acquire domestic assets whose value is determined by, for example, EU-level decisions (e.g., agricultural land, whose price is mainly based on EU-level agricultural subsidies).

Real estate investments in Finland are problematic in my opinion for these reasons. Apartment values and rent levels are mainly determined by Finland’s economic development, which does not promise very strong growth in the future. That’s why it’s enough for me to own my own apartment at some point. And even this is only sensible nowadays in certain parts of the country, i.e., in the largest urban areas. I personally do not intend to acquire investment apartments in Finland for the reasons mentioned above, although for someone else it might be a good business.