@lucas.mattsson has made a new extensive report on Metacon; the report itself is in English, and this non-PDF section has been translated into Finnish by AI.

As usual, this extensive report is also available for everyone to read. ![]()

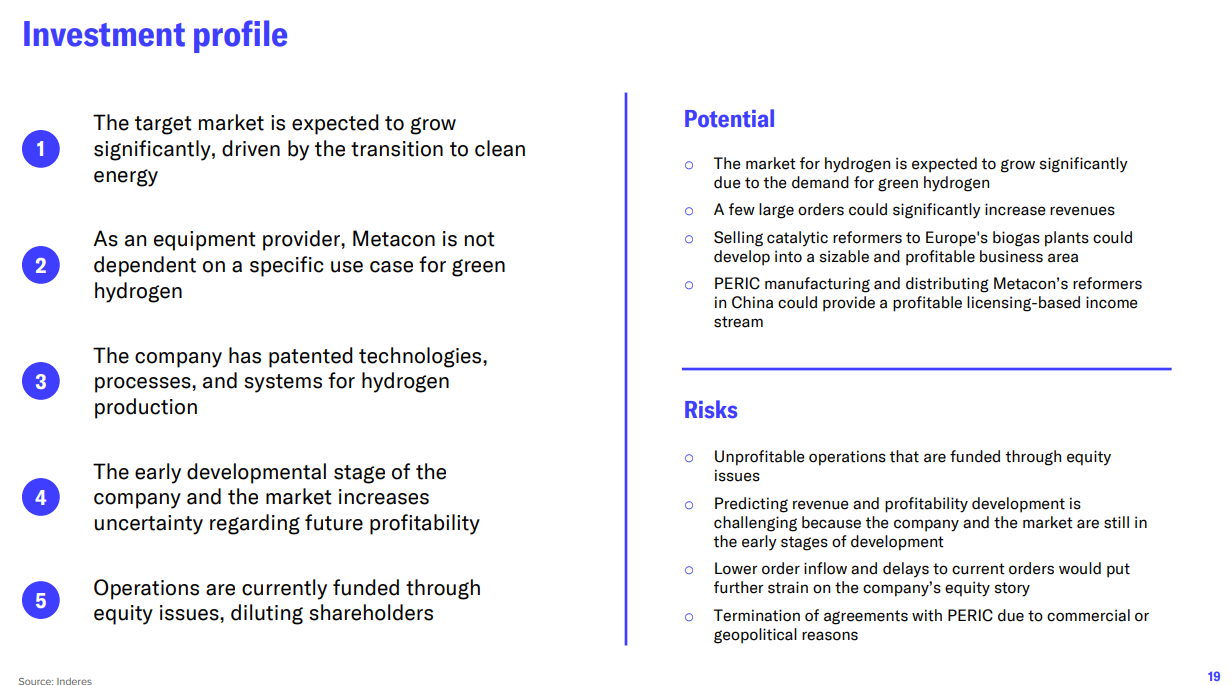

Metacon has assembled a complementary product portfolio and secured significant electrolyzer orders, which has increased revenue and brought valuable reference customers. While securing a few large orders increases the likelihood of a commercial breakthrough, it does not guarantee a steady order book. However, considering the strong long-term demand outlook for green hydrogen and Metacon’s growing market position, we see potential for continued strong revenue growth. Supported by these drivers, we assess the stock’s risk-reward ratio as attractive. We revise our target price to SEK 0.70 per share (previously SEK 0.30) and reiterate our Add recommendation.

Quoted from the report: