Tuntui vajaa vuosi sitten hankalalta valita korkorahasto pitkästä listasta. Poimin sitte melko hataralla tietopohjalla menneen tuoton perusteella tommosen:

Aktia European High Yield Bond+ B

Aika mukavasti mielestäni puksuttaa. 12 kk tuotto on yli 7 %, mut hallinnointi on aika kallis tämmöseksi 0,8%

Omassa potissa on kohta 6% tuotto. Koroista saa sitte nopsaan lisäpaukkua osakepuolelle jos kyykätään. Ennen oli kaikki vararahat Nordnetin tilillä mut ny koroista näkyis saavan iha mukavan tuoton. Tyytyväinen olen tohon.

Tämä hajautushyöty pätee yleisellä tasolla lähinnä valtionlainoihin, joiden korrelaatio osakemarkkinoiden kanssa on yleensä negatiivinen. Yksi syy negatiivisen korrelaation taustalla on se, että kun taloudella menee huonosti, laskevat paitsi osakemarkkinat myös korkotaso, mikä nostaa lainapaperien arvoa.

Yritys- ja erityisesti riskiyrityslainoista (High Yield) saa valtionlainoihin verrattuna korkeampaa korkoa, koska niissä on suurempi riski. Tästä käytetään nimitystä riskimarginaali. Kun taloudessa menee huonosti tai on riskejä ilmassa, tämä riskimarginaali yleensä levenee, eli korko nousee, mikä taasen laskee näiden lainapaperien arvoa.

= High Yield yrityslainat ja osakemarkkinat liikkuvat yleensä samaan suuntaan. Siksi ne eivät ole paras paikka säilyttää lisäpaukkuja osakemarkkinan laskun varalta. Muuten toki varsin varteenotettavia sijoituskohteita joita on rahastojen kautta itsellänikin.

19 tykkäystä

Jep, olen havainnut että osaa kyl laskeakin ![]() Mut kun liikkeet ovat rauhallisempia kuin osakemarkkinoilla, ehtii paremmin reagoida vrs. kuin" kaikki kiinni AI:ssä". Metsän ostokin kiinnostaisi mut siellä puolella on hinnat katossa.

Mut kun liikkeet ovat rauhallisempia kuin osakemarkkinoilla, ehtii paremmin reagoida vrs. kuin" kaikki kiinni AI:ssä". Metsän ostokin kiinnostaisi mut siellä puolella on hinnat katossa.

Itsellä myös pohdinnassa, että ryhtyisin rakentamaan pitkään salkkuun korkokomponenttia. Haluaisin mukaan sekä yrityslainoja että valtioiden papereita. Tarkoitus olisi ostaa hiljalleen kk-säästössä pitkän aikaa pienillä summilla, horisontti yli 10 vuotta. Tavoite on, että lopulta koroissa olisi n. 15 % pörssisijoitusten määrästä.

Tällä hetkellä olisin päätymässä tähän rahastoon.

Olen käynyt läpi Nordnetin ja parin muunkin kivijalan tarjonnan ja en ole osannut löytää vastaavaa tai parempaa tuotetta halvemmalla.

Mitä ajatuksia tämä rahasto herättää?

Samaa opiskelua itselle menossa myös. Tosin toimenpiteitä tulossa vasta noin 10 vuoden sisällä, koska jossain vaiheessa alan muuttamaan vähitellen osaa sijoitusvakuutuksen sisällä olevia osakerahastoja/ETF:iä korkopuolelle.

1 tykkäys

Yksi ajatus ainakin herää noista hallinnointipalkkioista. Rahasto sijoittaa muihin rahastoihin, eli rahaston säännöistä kaivettava, maksaako se näistä sijoituksista hallinnointipalkkiota kohderahastoon. Todennäköisesti maksaa, jolloin todelliset efektiiviset kulut lienee yli kaksinkertaiset ilmoitettuun nähden.

Toinen ajatus on valtionlainat noin pitkällä sijoitushorisontilla (10 vuotta - useita kymmeniä vuosia). Itsekin tätä pohdin vastaavalla horisontilla ja päädyin kasaamaan korkojen osuuden salkkuun (n. 20%) yrityslainoista, riskiyrityslainoista ja kehittyvien markkinoiden valtionlainoista.

Paljon vaikeampi näitä rahastoja oli itselle vertailla kuin osakerahastoja. Maturiteetti ja YTM luvut lähinnä ymmärsin vertailla ja lopulta päädyin oman kivijalkapankin rahastoihin, jottai voin käyttää osuuksia lainojen vakuutena.

5 tykkäystä

Kuten tuossa jo mainittiinkin, kyseessä on rahastojen rahasto, joten kannattaa tsekata mitkä ovat todelliset kulut kun ”alla olevat” rahastotkin sisältävät hallinnointipalkkiot.

Lisäksi linkkaamasi rahasto on W-merkinnällä. Muistaakseni tätä sarjaa voi ostaa vain varainhoitosopimusasiakkaat tms. ja sen takia hallari on 0,45%. Normaali Kompassi Korko veloittaa 0,90%. Kannattaa varmistaa tuo asia.

Kulut mietinnässä itselläkin.

Säännöt sanovat että

4 § Palkkiot

Rahastoyhtiö saa korvauksena toiminnastaan hallinnointipalkkion, joka vaihtelee rahasto-osuussarjoittain. Hallinnointipalkkion enimmäismäärä on 2 prosenttia vuodessa laskettuna Rahaston arvosta. Tieto kulloinkin veloitettavasta hallinnointi palkkiosta sekä tieto Rahaston merkintä- ja lunastuspalkkion enimmäismäärästä on Rahaston kulloinkin voimassa olevassa avaintietoesitteessä sekä rahastoesitteessä. Rahastojen palkkioista löytyy myös tietoa Rahastojen yhteisten sääntöjen kohdista 13 ja 14 §.

Sitten yhteisistä säännöistä:

14 § Rahaston varoista maksettavat korvaukset

Rahastojen sijoituskohteina olevista rahastoista ja yhteissijoitusyrityksistä peritään hallinnointi- ja säilytyspalkkioita näiden rahastojen ja yhteissijoitusyritysten sääntöjen mukaisesti.

Avaintietoesitteen mukaan tuo 0,45 % on arvio ja perustuu viime vuosien toteutuneisiin kuluihin.

Luenko edes oikeita kohtia näistä papereista?

EDIT Säännöt näyttävät olevan tismalleen samat kaikille rahastoille. Pitääkö tässä nyt sitten luottaa tuohon avaintietoesitteen lukemaan, jonka sanotaan olevan toteutuneisiin kuluihin perustuva arvio?

Moi!

Kertokaas nyt mulle paljonko korkorahastoista kannattaa maksaa hallinnointikuluja? Mitkä ovat siis vielä järkevät kulut? Ja otetaan esimerkkinä vaikka Evllin ko rahastot? Onko nämä kalliita/järkeviä vai onko tämmöiset järkevämpi ostaa jostain muualta?

Evli Nordic High Yield B

Evli High Yield Yrityslaina B

Evli Pohjoismaat Yrityslaina B

Evli Lyhyt Yrityslaina B

1 tykkäys

Järkevä on suhteellinen käsite ja korkorahastoihin sijoittaminen on lähtökohtaisesti omasta mielestäni riskin karttamista. Itse ainakin ajattelen, että olen korkorahastotoihin sijoittaessani hyväksynyt alemman tuoton pienemmän riskin tai oikeastaan heilunnan perusteella. Riski on vähän vaikea käsite. Jos sijoitat Konkurssi Oy Ab:hen ja se menee konkurssiin niin mikä on ero, että sijoituksesi on osakeissa vai yrityslainassa. Ero on lopulta aika pieni. Voit myydä osakkeesi pörssissä yleensä kun keikahtaminen on aikalailla näkyvissä ja yleensä vielä konkurssi menettelyn käynnistyttyä. Saat jotakin, esimekkinä 1000€ sijoitus joitan kymmeniä euroja. No yrityslainassa saat velkojan järjestelyn kautta ehkä jotakin. Etukäteen on mahdotonta sanoa kummasta saat paremmin. Riski on käytännössä voit “menettää kaikki rahasi”.

Jos voidaan rinnastaa lopputulos on pahimmassa tapauksessa “sama” niin miksi sitten sijoittaa korkorahastoon? Vastaus on mielestäni pitkälle se, että hinta ei vaihtele ja saat varmemmin “omasi takaisin” eli ei missään vaiheessa ole tarvetta myydä suurella tappiolla. Suuren tappion mahdollisuus on sitten korkorahastossa tavallan merkittävämpi kuin osakeessa. Velkakirjoissa siun on hankala saada suurta tuottoa yrityksen tilanteen paranemisesta, joten “pommeihin” sijoittaminen ei ole niin high risk high reward tyyppistä ja noita high reward on aika harvoin tarjolla. Tämä tarkoittaa siis sitten, että vähäisempi heilunta tarkoittaa vähäisempää heiluntaa ylöspäin eli mahdollista suurinta tuottoa, jonka jo viestin alussa mainitsin eli on hyväksynyt ettei sijoitus tuo huipputuottoa 100% yms pidemmmällä aikajänteellä vaan tasaista puksutusta ylös hitaasti.

Kysymyksessä oli nyt sitten järkevä kustannus. Tehdään vertaus vaikkapa kahvikuuppiin. Huoltoasemalla nyt voi järkevä kahvin hinta olla milestäsi 2,5€,. Jos menet johonkin tueisti kohteeseen, vaikkapa Pariisiin sama järkevä kustannus voi olla 4€ ja kahvi useissa paikoissa maksaa jopa 7€. Tämä on verratvissa hyvin sijoittamiseen. Järkevä hinta on suhteutettava mitä on saatvissa. Korkosijoitusten osalta mitä sillä hinnalla saat. Nyt mainittujen EVLi rahastojen osalta on katsottava mitä niillä oikeastaan halutaan? Olet sijoittanut esimerkkinä Pohjoismaisiin yrityslainoihin. Vatsavaa tuotetta on varmasti hankala saada mekrittävästi halvemmalla. Mutta heti herää kysymys onko se tarpeen. Vilkaisemalla rahaston kehitys suhteessa vertailuindeksiin näkee, että rahasto pessyt indeksin ja tuottonut varsin hyvin, joten omasta mielestäni perusteltua sijoittaa siihen. Toisaalta rahaston korkotaso oli 4,1%, joka on mielestäni “keskikertainen” ja kertoo tulevasta tuotto odotuksesta jotakin eli tuota tasoa voi odotella tuotoksi. No jos palkkio 0,75%/4,1%*100%=18% eli käytänössä palkkio vie tuotosta 18%. Minusta se plajon, mutta tässä tapauksessa perusteltavissa, koska salkunhoitaja pystynyt tekemään parempaa tuottoa kuin indeksi. Hirvittävän suurta osuutta sijoituksista itse en laittaisi kyseiseen rahastoon. Vaatii jatkuvaa onnistumista salkunhoitaalta. Toisaalta voi olla, että pohjoismaiden pienillä syrjäsillä yrityslainamarkkinoilla on mahdollisuuksia ja voi hankala löytää parempaa vaihtoehtoa sijoittaa niihin. No kirjoituksen voi aika suoraan monistaa suoraan EVLi high yriled yrityslainoihin. Siellä tuo huonon paperin riski nousee, mutta vastapainona pienillä markkinoilla voi olla noita helmiapaikkoja eri tavalla. Lyhyt yrtyslaina on samoin tuottanut erinomaisesti suhteessa indeksiin. Vastavaa rahastoa voi olla hankala löytää.

Mielestäni kyseenlaisin rahasto on EVLi High Yield Yrityslaina. Se ei ole pärjännyt indeksille ja korkeat kulut. Tässä toki voi olla nyt hyvät mahdollisuudet. Kokonaisuutena mielestäni paketti on ihan ok. Sinulla on hyvä mahdollisuus saada indeksiä parempia korkotuottoja ja vastinetta korkeille palkkioille.

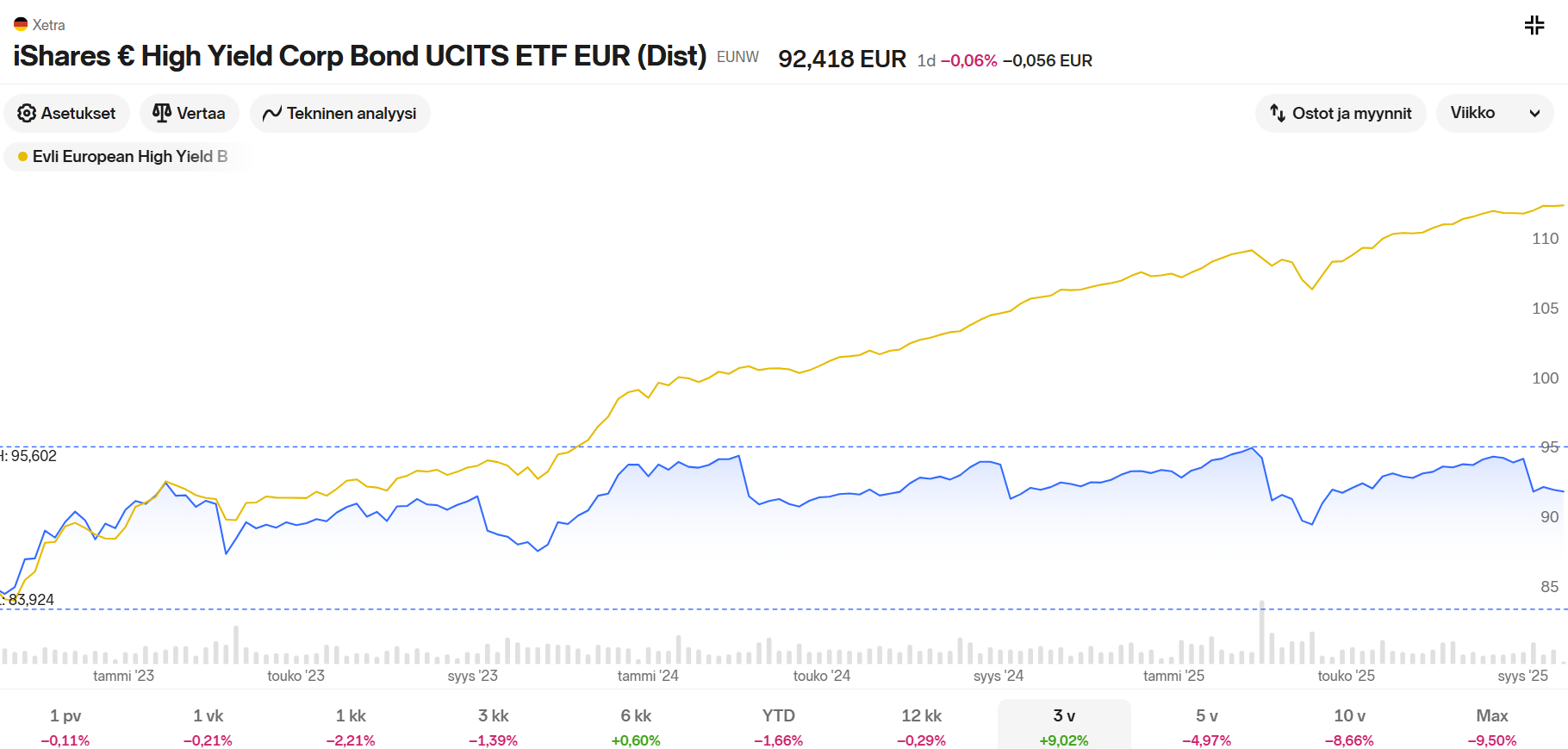

Katsoin hilajttain Sijoituskästissä Reima Salmisen haastattelun ja siinä itsellä jäi mieleen hänen kommnetinsa, että korkorahastoissa aktiivinen salkunhoito on kannatavampaa ja löytyy hyviä rahastoja. Nuo EVLI:n rahastot näyttävät yhdeltä esimerkiltä ja olen erittain kiinnostunut muiden mielipiteistä ja näkemyksistä tästä asiasta, jonka vuoksi itse tähän vastailin ja aloittelin keskustelua. Vimeiseksi laitan tähän vertailun "hiukan parjaamastani EVLI:n High Yieldistä verratuna Nordnet kuukausisäästön iShares € High Yield Corporate Bondiin

Ainakin itsellä pistää ajattelemaan. Olen kiinnostunut muiden ajatuksista.

4 tykkäystä

On korkosijoituksilla oma paikkansa hajautetussa sijoitussalkussa, mahdollisesti myös korkorahastoilla.

Jokaisen sijoittajan on hyvä pitää ainakin osa salkusta hyvin likvidissä muodossa. Tähän käyttötarkoitukseen soveltuu pankkitalletukset, rahamarkkinarahastot ja lyhyen koron rahastot. Kaikilla näillä hieman erilaiset riski- sekä tuottoprofiilit erityisesti silloin kun mennään talletussuojarajan ylitse.

Vakuudettomissa lainoissa on juuri noin kuin sanot, eli tappioriski on sama kuin osakkeissa, mutta tuottopotentiaali on cäpätty. Kokonaisuus muuttuu korkosijoittajan näkökulmasta aivan erilaiseksi kun aletaan puhumaan vakuudellisista seniorilainoista (senior secured). Näitä ei velkasaneerauksessa leikata ja vakuudella on yleensä sellainen arvo, että konkurssitilanteessakin voi saada omansa pois. Tuottoprosentti näissä yksinumeroinen, mutta vähäriskisenä voi hyvinkin sopia osaksi sijoitussalkkua.

Pitkät korkopaperit ja niiden rahastot ovat erityisen mielenkiintoinen sijoituskohde laskevien korkojen aikana. Evlin korkorahastoista sai 2023-2024 karkeasti 10% vuosituottoja korkojen laskiessa.

Korkorahastot sijoittavat käytännössä vain isompien yhtiöiden korkopapereihin. Kun mennään pienempien yhtiöiden lainoihin on korkotasot käytännössä aina kaksinumeroisia. Tällä private debt markkinalla voi päästä myös erinomaisiin tuottoihin suorilla sijoituksilla tai rahastoilla.

Kulut ovat monessa korkorahastossa korkeat ja ne tekevät rahastosijoittajan toiminnan hankalammaksi. Minulla oli salkussa yhtä Evlin korkorahastoa josta maksoin 0,75% vuotuista hallinnointipalkkiota mutta tienasin vajaan 10% noin vuoden sijoitukselle kulujen jälkeen. En tiedä mitä vaihtoehtoja olisi ollut, kun sijoituksen tarkoitusksena oli nimenomaan päästä hyötymään pitkien korkopaperien arvonnoususta korkojen laskiessa.

Kannattaa käydä itsensä kanssa keskustelua esimerkiksi aiheista miksi haluan sijoittaa rahastoon/instrumenttiin X, mikä on sijoituksen tuotto/riskiprofiili, mikä on sijoituksen pitoaika ja mitkä ovat triggerit sijoituksen realisoimiseksi. Sijoitushorisontti korkorahastoihin tuskin voi olla ikuinen, sillä markkinat voivat mennä sijoittajan kannalta sellaiseksi ettei siellä kannata olla mukana. Tällä hetkellä esimerkiksi pitkissä valtionlainoissa yieldit ovat noin 3%, enkä ole keksinyt syytä miksi tuossa markkinassa kannattaisi olla mukana nykyisellä tuottotasolla.

6 tykkäystä

Vuohensillan sijoitusnurkasta olen saanut tähän mennessä ytimekkäimmän ja ymmärrettävimmän tiivistyksen korkorahastojen eroista.

Eli jos ajatellaan olevamme nyt korkopohjassa ja korot (mitä ne tässä tapauksessa olisikaan) lähtisi nousemaan, niin duraation perusteella korkorahastot tulisivat vastaavasti alas.

Ymmärtääkseni se siis tarkoittaa myös noissa VGEA, VAGF ja VDTE, että kun niissä on kaikissa yli 5 duraatio, niin ne eivät ole ihan niitä turvallisimpia sijoituksia korkojen noustessa.

3 tykkäystä

Ovatko inflaatiosuojatut korkorahastot / linkkerit tarpeellisia osana piensijoittajan hajautettua korkosalkkua? Omaan tutkaan ei ole tullut havaintoa että niistä ainakaan Suomessa mitään puhuttaisiin. Ei tässä itsellä näkemystä kiihtyvästä inflaatiosta ole, mutta tekoälypalvelut noitakin suosittelee ikään kuin vakuutuksena yhtenä osana koko sijoitussalkkua.

1 tykkäys

Tätä olen itsekin miettinyt, varsinkin kun suunnittelen 10-20 vuoden päähän eri sijoituslajien allokaatiota siihen vaiheeseen, kun jään viimeistään eläkkeelle.

Koska valtiolainoista ei juuri tuottoa saa ja IG yrityslainojen riskitaso on samaa luokkaan, olen itsekin miettinyt esim seuraavaa yhdistelmää + jotain lyhyttä korkoa. Korkosalkut yhteispainotus olisi ehkäpä noin 30%

-Nordea Corporate Bond

-iShares Euro Inflation Linked Government Bond UCITS ETF

Mutta aikaa on vielä pohdiskella tilannetta. Mielenkiintoista on, että korkorahastoissa moni aktiivisesti hoidettu korkorahasto on pessyt tuotoissa matalakuluiset vastaavat ETF:t, jos tarkastelee esim viimestä 5 tai 10 vuotta.

1 tykkäys

Luottovakuudellisissa obligaatioissa (CLO) on sisäänrakennettu inflaatiosuoja. Kannattaa googlata.

Itsellä kanssa lähelle tuo haarukka eläköitymiseen. Mitä itse olen opiskellut korkosijoituksista ja ihan viime aikoina vahvasti tekoälyn opastamana, niin hyvin hajautetussa korkosalkussa on useaa erilaista komponenttia ja jokaisella on enemmän tai vähemmän oma erilainen tehtävänsä.

Opetettiin niin että et osta valtiolainalla pelkästään tuottoa, vaan vakuutuksen / suojan sellaisessa taantumassa jolloin talous hyytyy, osakkeet ja korot laskee ja valtiolainan pitkä duraatio tuo kovat tuotot vastapainoksi osakkeiden laskulle. Yrityslainat ei niin käy tähän tehtävään, koska luottoriskillisinä laskevat osakkeiden mukana.

Linkkerit kai käyttäytyy vastaavassa kriisissä hiukan poikkeavasti vaikka valtiolainoja ovatkin, mutta ne ovatkin vakuutus taas toisenlaiseen ympäristöön. Niiden tuotto riippuu useasta tekijästä ja tällainen tuulipuku ainakaan ei ihan heti sisäistä niitä mekanismeja. Toteutuva inflaatio kuitenkin vaikuttaa tuottoon ja tekoäly laski että vaimeahkolla 2,0% euroalueen inflaatiolla esim. LYQ7 tuotto jää 0,4% vertailussa olleesta valtiolainan tuotosta. 2,4%→ suuremmalla inflaatiolla tuottaisi sitten paremmin tässä skenaariossa. Liian isosti ei kannata vakuuttaa, mutta pieni määrä taas ei tunnu missään. Itselle tulee suht maltillinen määrä ja eihän ne rivit salkussa kesken lopu.

Mistäpä näitä tietää ja 2022 kriisissä laski osakkeet, pitkät valtiolainat ja linkkerit.

Jossakin korkopodissa oli 2-3 vuotta sitten selitetty että indeksi ei korkopuolella välttämättä niin toimikaan kuin osakepuolella. Tehokkaimmilla markkinoilla ja matala tuottoisissa kohteissa salkunhoitajan on ilmeisesti kuitenkin vaikea kuroa edes palkkiota kiinni, kuten valtiolainoissa ja isoissa yrityslainoissa. Itsellä on ennestään vähän aktiivista valtiorahastoa ja harkinnassa vaihtaisiko indeksiin. IG luokassa indeksituotot ovat menneet aika alas ja aktiivisista voisi löytyä jotain vaikkapa Evliltä.

Tekoälystä vielä että itse olen vasta viime aikoina alkanut enemmän käyttämään ja on kyllä huikeeta settiä. Huomannut kuitenkin että tekee virheitä ja ei kannata suhtautua ihan varauksetta. Oikeiden tickereiden hakeminenkin xetraan on ihmeen haastavaa.

4 tykkäystä

Kiitos tästä ilmeisesti sitten hyvästä vinkistä.

Vaikka tännekin näpyttelen, niin en ole jaksanut vielä selvittää mitä nämä ovat. Jos veikkaa, niin mahtaako päästä kuin isommalla panostuksella mukaan ja mistä näitä edes saa. Olikos semmoinen vanha totuus, että älä sijoita mihinkään mitä et ymmärrä ![]()

Bank of America:

”’Kaikkea muuta paitsi joukkovelkakirjoja’ on vuosikymmenen jälkipuoliskon teema, ja sijoittajien tulisi suunnata katseensa kansainvälisiin osakkeisiin, pienyhtiöihin, keskisuuriin yhtiöihin sekä kultaan, Bank of America sanoo”

https://www.marketwatch.com/story/now-is-not-the-time-to-own-bonds-says-bank-of-america-these-are-safer-bets-3e3967e5?mod=home_lead

6 tykkäystä

OP:n Saari sanoi Valtiolainoista yllättävän vahvan, oliko sitten enemmän henkilökohtaisen näkemyksen tähän suuntaan, että ei houkutteleva edes hajautus tai turvasatama mielessä, koska kestämättömästä valtioiden velkaantumisesta johtuen korot hiipiivät ylöspäin. Jos sentimentti maailmalla on tämmöinen, niin toteuttaako se itseään ja onhan se kullan hinta raketoinutkin.

5 tykkäystä

Mitä mieltä tästä kommentista muut korkopäät?

Itse haluaisin kuulla tähän muiden mielipiteitä, koska itse olen ainakin Likvidi B:tä pitänyt varakassana. Jos vaihtoehtona on Likvidi B tai käteinen tilille, tuntuu Likvidi lähes ilmaiselta lounaalta, kun näitä kahta vertaa.

Ainoana miinuksena toki, että rahasto-osuuden myynnin toteuttamisessa on pieni viive eikä rahaa saa heti sieltä pois, mutta toisaalta, kun rahan nostamisessa on pieni viive, ei hyppää FOMO-kelkkaan ja jokaiseen uuteen ideaan niin herkästi mukaan. Lisäksi Likvidi B:ssä olen pitänyt siitä, että lähdeveroa ei makseta suoraan niin kuin säästötilitalletuksien koroista eikä tietyn korkotason saaminen vaadi sitä, että rahat ovat x ajan kiinni tilillä.

2 tykkäystä