It’s probably not very sensible to spend time pondering this when the clear message from management is that they are still investing in them and not shutting them down.

Not for a long time. Now more services have been purchased from Inderes or Inderes has offered a free sample.

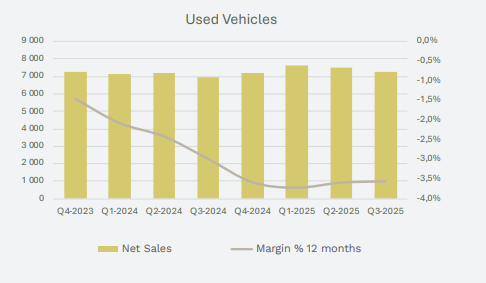

Rauli has prepared a new company report based on Q3 results. Juha Kalliokoski, who has returned as Kamux’s CEO, is bringing the company’s focus back to volume growth, which should also improve profitability. However, in our opinion, no clear actions or drivers to support growth were disclosed. The company’s profit level remains subdued, and it does not appear to have plans to divest its loss-making international operations. We slightly lowered our forecasts and reiterate our reduce recommendation and a target price of 2.0 euros.

Quoted from the report:

Forecasts Lowered

We also lowered our forecasts for 2026-27. This was influenced by a small decrease in the average car price forecast in Finland and, consequently, the forecast for integrated services. Due to Finland’s large absolute profit, their decrease weighed most heavily on the group’s forecasts. For Sweden, we raised our gross margin assumptions. However, we had previously expected store closures and thus clear cost savings, which do not seem to be materializing. Consequently, our fixed cost forecasts for Sweden increased. Overall, Sweden’s forecasts rose slightly, but the adjusted operating profit remains in the red for 2026-27. There were no significant changes to Germany’s forecasts, and we assume losses in the coming years as well.

With good luck, someone would buy the entire operation for the price of the car inventory. But if we consider a more difficult scenario, I believe the cars should be sold at roughly their book value. In this case, the problem would mainly be leased premises and employees. Germany’s fixed costs (largely these two items) are around EUR 9 million this year. I’m not familiar with German practices, but if you multiply that by 1.5-2x, I would think you could get rid of employees and premises, so roughly EUR 15 million. This is probably close to a “worst-case” scenario, as it would, of course, be smarter to gradually wind down operations in a more planned manner, so that lease agreements would be ending and there would be fewer salespeople when the doors are finally closed.

It’s good to remember, however, that even though Sweden had zero EBIT in Q3, losses are expected to continue there, at least in our forecasts. And it’s only a little over a year ago that Germany was making a small profit and seemed to be in better shape than Sweden. And, of course, even with zero EBIT, value is destroyed. So there is still quite a lot of work to be done more broadly in these international operations.

Now, at least, the analyst cannot be accused of too much optimism

Indeed, in Sweden too, some are making big money in car sales even now. It’s possible that Kamux will also start making a profit there. The economic situation in Sweden is quite different from ours in Finland.

In Finland, for example, K-Auto and J Rinta-Jouppi Oy are both likely at an ATH pace.

Of course, Kalliokoski admitted that their “problem” is within the company’s own fences..

Wasn’t the message from the company’s management in the spring that the focus would be on profitability at the expense of volume? This is, of course, not really possible, as unprofitable trade-in cars would rot in storage. But it’s erratic behavior.

Pursuing volume did not yield results, emphasizing profitability at the expense of volume did not yield results, turning Germany profitable did not yield results but it returned to a loss. Sweden has been at a loss, now with its head above water for a moment until returning to normal, changing the manager to a competent professional did not yield results, changing managers of international operations did not yield results, closing unprofitable dealerships did not yield results, a cooperation agreement with a leasing company did not yield results, updating the car fleet to match demand did not yield results, investing in ancillary services (Extended Warranty, Insurance) did not yield results, introducing ancillary products for sale did not yield results (Tires), investing in remote car sales did not yield results.

Have all possible measures already been tried, what is left, or are there any means left?

Or will we return to the starting point in implementing the measures, and repeat the same actions in the same or a different order, without results?

I think Sweden has been brought to zero by shifting more of the margin from imports to Finland there, it is of course possible to do the same for Germany, and achieve a situation where all countries are slightly in the black, but that does not change the overall picture.

Yes, in Q2-Q3 the focus was specifically on profitability at the expense of volume. That did improve the gross margin, but so much volume was lost that operating profit still weakened. Indeed, there have been quite a few management changes and various inventory “adjustments” made in recent years. As I wrote in the report, Kalliokoski did not, in my opinion, offer any new ways to achieve profitable growth now.

Now that Kamux is apparently starting to buy back its own shares today, one must be careful not to dump one’s own shares into the market when demand for the share slightly improves.

I also looked at Kamux’s Q3 materials, interviews, etc., and this is a classic case of running aground and being in a deadlock. I have encountered the exact same thing in my own professional life. That is, someone far from the customer interface decides that the margin (usually some margin percentage or unit price) will be significantly adjusted and an overly challenging target is set. The end result is that the topline suffers, and then both the margin and operating profit in euros decrease when deals are not made due to poor price competitiveness. Fixed costs continue their course, and in Kamux’s case, there are simply more of them per completed car sale.

Even in Kamux’s case, the gross margin per car had improved, but the most important thing, the bottom line, suffered badly.

Now Kalliokoski explained that Kamux needs to be steered with big movements of the wheel, well, now at least the front end crashed into the inner bank.

Pajuharju was accustomed to Harvia’s pricing power, but Kamux DOES NOT have similar.

Used car dealers sell the same products, and their prices are easy to compare.

The management roulette continues in Sweden. This time, however, it seems to be of the person’s own volition, and the reasons have been explained in the announcement, so there’s probably no need to worry about Sweden’s Q4 development based on this. Still, it certainly doesn’t make turning things around easier when managers change once a year. Kempas started at the beginning of this year.

Hedin’s Q3 figures today. Used car revenue grew by 5% and growth was seen in all markets. Profit, however, is in the red, apparently still mainly due to electric car buyback commitments and perhaps more generally due to electric car pricing.

In addition, Wetteri announced new targets yesterday, aiming to double the size of its used car business in the coming years, so competition appears to remain tough (here’s Thomas’s comment)

Given that Chinese cars are quite popular judging by export figures, Kamux also needs to seriously consider its approach to them. BYP reportedly trades well on the market, but many used Chinese cars are a bit touch-and-go… Indeed, for some brands, the import organization and spare parts service are modest.

Trump’s anguish over the poor export success of American cars is not unfounded.

Now that the “earnings warning weeks” are upon us, a small recap.

Inderes expects a slight improvement from Kamux in Q4/25 vs. Q4/24.

On Saturday, I was at an evening gathering where there were also several highly knowledgeable individuals from the car industry. They claimed that Kamux in Finland is 5-10% ahead in units compared to last year’s Q4, as is also expected.

What the entire Kamux has achieved in Q4 and what profit has been made will only be seen in February. But Kamux’s Q4/25 should be well within the expected range so far. I myself do not expect an earnings warning anymore this December…

Well, in Q4 2024, the adjusted operating profit was €0.7M, now Inderes’ expectations are €2.8M if the €8M presented in that quote for the full year is still valid.

The company’s own guidance is very loose: “adjusted operating profit decreases from the previous year,” to achieve which, any result from the last quarter is sufficient.