Lately, the discussion has drifted into topics that might not be the most important things for an investor following Kamux. So perhaps more focus on matters that are a bit more significant from an investor’s perspective.

Some messages might be better suited for these threads:

So your own gut feelings and lighter comments, which don’t interest investors and analysts much, can perhaps be posted elsewhere or not at all. More messages that are more relevant to investors, genuinely bringing added value to investors. A really large number of people follow this thread, so it’s advisable to post messages thoughtfully.

Thanks for your understanding and happy discussions!

Here are Rauli’s preliminary comments as Kamux reports its results on Tuesday.

We expect revenue to have decreased slightly from the comparison period, but the result to improve from a weak comparison period. Kamux has guided for an improvement in adjusted operating profit for the full year, but our forecasts expect a weaker result. Thus, in our opinion, the risk of an earnings warning is obvious. The results can also be followed on Tuesday morning in the earnings live stream.

Arvopaperi has interviewed Tapio Pajuharju and Juha Kalliokoski. The article covers many topics, including Kalliokoski’s appointment as Chief Operating Officer. According to Pajuharju, the idea was not solely his:

“We discussed this with the whole group, even on the board. We had been looking for a person for a long time who has sensitivity, speed, and a nose for the car industry.”

They had initially looked for a suitable person outside the company but found it difficult to find one and concluded that the right person was close at hand.

They clarify the division of responsibilities as follows: Kalliokoski is responsible for car purchasing, sales, and inventory management. Pajuharju describes his own role:

“The CEO is responsible for implementing the strategy and leading the business. For ensuring that we operate as one Kamux and that the concept is implemented in the same way in all three markets.”

According to Pajuharju, they have a schedule for turning Sweden profitable, which, however, will not be disclosed to the public.

What happens if the schedule is not met?

”Then something else must be done. We have decided that this cannot continue,” says Pajuharju.

The visibility of the article is restricted to subscribers only:

Kamux tracking has been minimal, as I’ve happily been Kamux-less for quite some time.

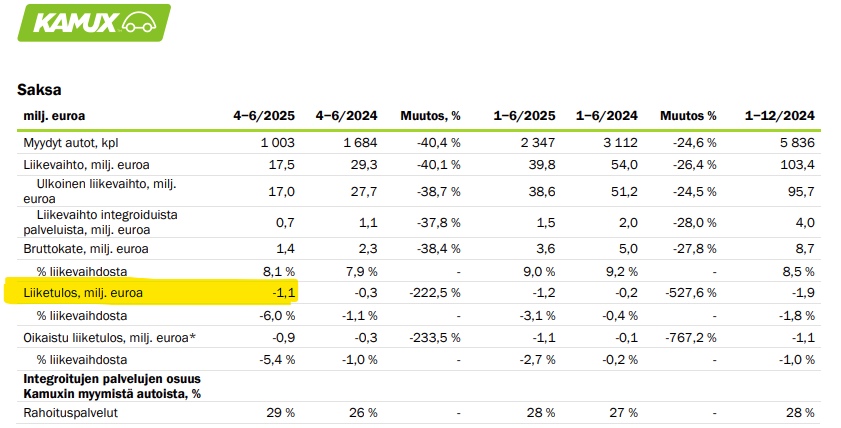

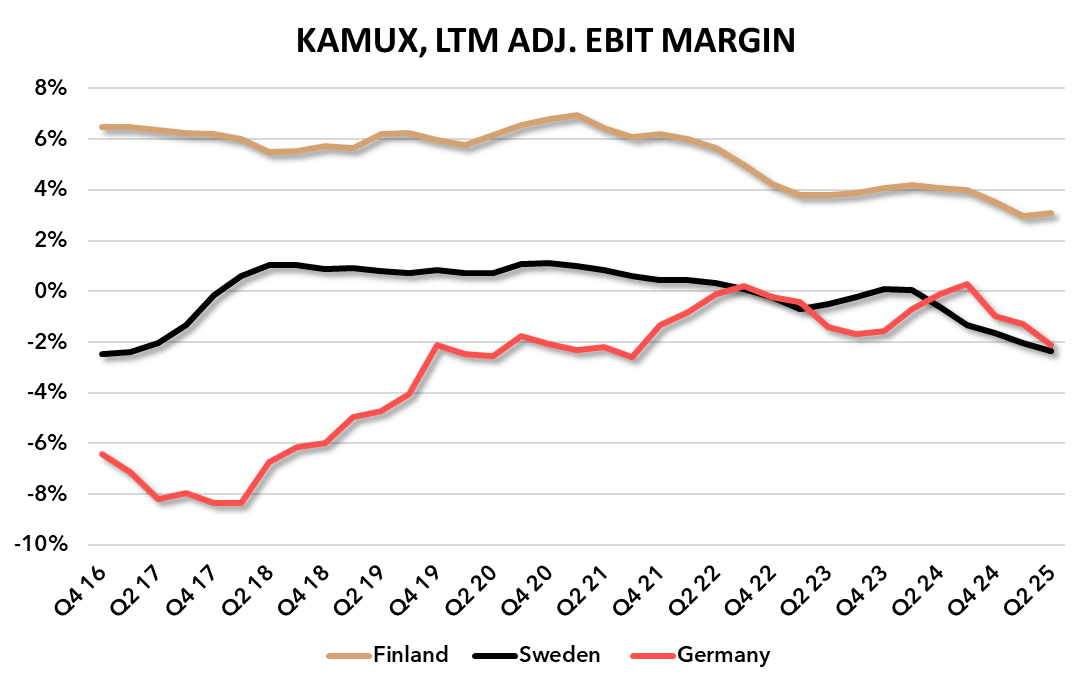

At a quick glance, it certainly looks like Sweden and Germany are being rapidly scaled down.

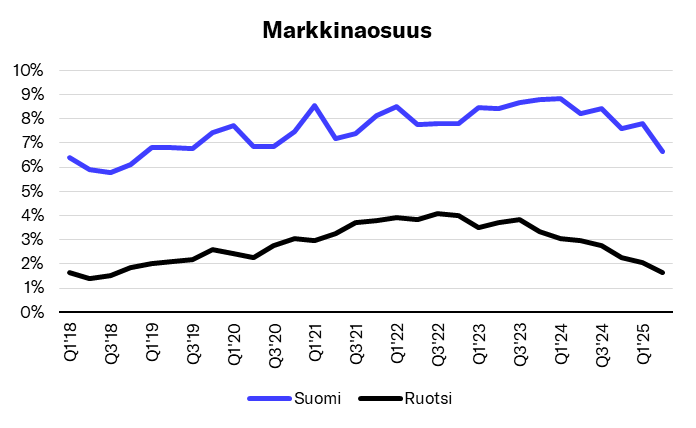

Finland’s market share is also plummeting fast.

Another observation is that profitability holds up surprisingly well with such weak volume.

So it seems that the focus is being shifted so that in the future the goal is to shut down unprofitable ventures and defend Finland’s cash cow position.

Visions and missions seem to be going into the scrap heap here, but perhaps the sinking ship can somehow be turned around within a couple of years regarding the bottom line?

This is certainly the aim. However, in the used car business, it’s a difficult combination to reduce sales and try to make a profit - while simultaneously leaving unprofitable cars to rot in storage. This will at some point mean either a large write-down or just a very unprofitable quarter/half-year.

It seems so. The funds collected for expansion were squandered and it was concluded that it didn’t succeed. My own assessment is that in Germany and Sweden, they should have expanded much larger to properly differentiate themselves from small shops, but that’s just not what happened. Did they run out of money or expertise? There was at least one blunder in Germany that surely dampened enthusiasm as well.

Not many days have passed since Kamux opened its latest new store in Germany, so that’s a bit contradictory to the notion that they would be shutting down German operations…

In Germany, a million in the red in a quarter, it’s no wonder if the boss gets fired.

But is the fault in one man…?

I wonder about opening a new business, why is such a thing done…?

Kamux has no competitive advantages. It would be advisable to exit Germany and Sweden in a controlled manner as lease agreements expire. I don’t believe these can be made profitable, or at least not profitable enough to achieve any reasonable return on equity. Come home on the milk train and set up a proper hedgehog defense in Finland. This is at least what I would hope would be done. However, it seems that this is not the direction we are heading, and more value is being destroyed abroad.

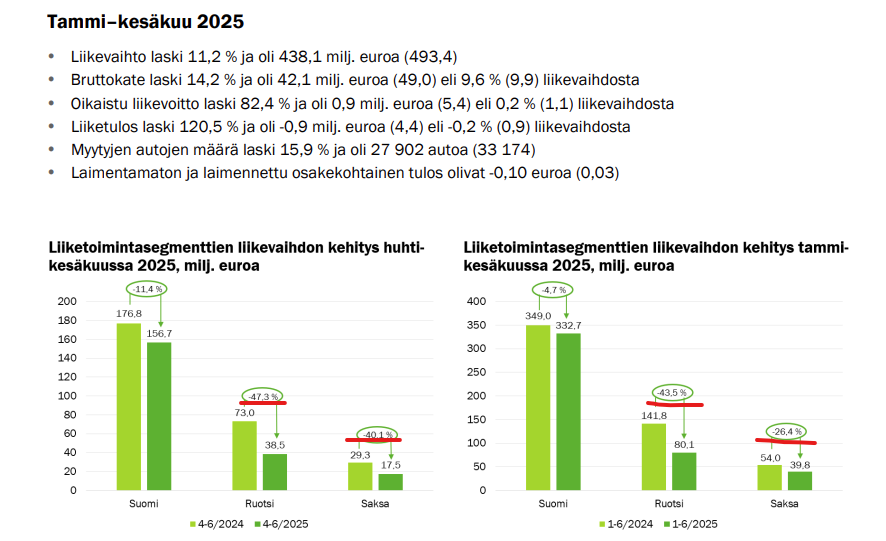

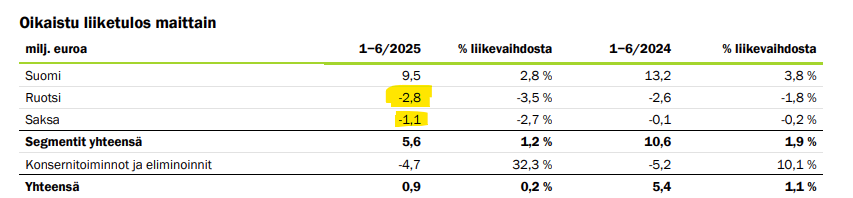

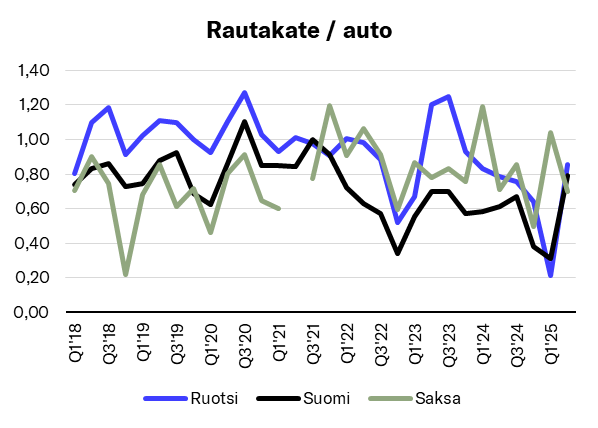

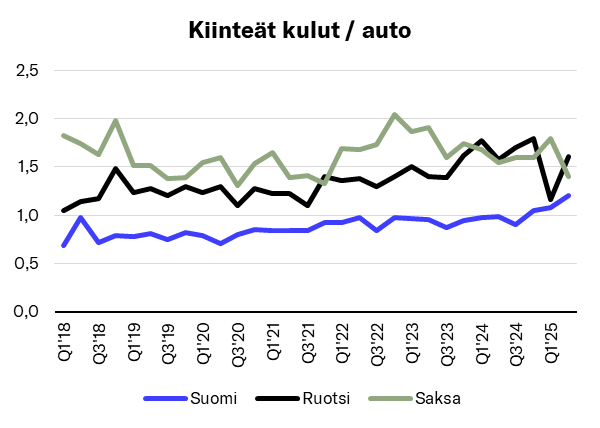

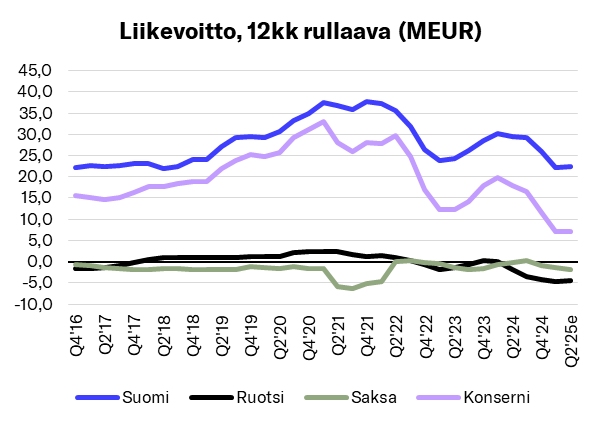

This could be a sensible direction, but I doubt it has been consciously chosen yet; these volume declines merely indicate Kamux’s difficulties in doing profitable business. Here are the figures in a table and a couple of graphs:

Sharp improvement in Finland’s and Sweden’s gross margins from the weak level of previous quarters to a somewhat normal level (at the expense of volumes, of course)

However, declining volumes are reflected in fixed costs / car increasing, especially in Finland, in a trend-like manner

The decline in adj. operating profit was interrupted for a moment, but it’s difficult to reverse the trend with the aforementioned volume/market share development

Thank God I got out of this boat. I loved the stock a bit too long, but in its defense, Kamux certainly had all the keys to conduct good business in Finland and abroad. Others succeed, and market growth provides support. The reason is simply the company itself, and at least to my eye, it’s starting to look like it might never get out of this spiral.

The rest of the year presents challenges. There is no revenue guidance; I assume it’s the same as 2024. The adjusted EBITA guidance is that it’s slightly better than last year; I assume 5% growth.

Apparently, low-margin and negative-margin deals have been forbidden? If I understood correctly from the recent webcast… If so, there is a big risk that it will still be found later. For those cars taken into inventory at too high a price, such a thing can easily just be kicking the can down the road, but of course, it makes the average margin look better temporarily.

How the hell would I know. No one is forced to have any sustainable competitive advantage based on which they can be better than other competitors. If I were to buy a car myself, I wouldn’t pay more for the same car just because of the seller’s logo.

However, I suppose the biggest players in Sweden and Germany can achieve some kind of scale advantage. Fixed costs are relatively smaller. Certainly, some operators are better at buying cars, negotiating lease agreements, and get a better margin from a car of the same price. Kamux, however, has no competitive advantages, at least not in Germany or Sweden. Or if it does, I’d like to hear more about them. In Finland, there is probably a small scale advantage compared to smaller competitors, but hardly compared to, for example, Saka.

It was once believed that Kamux’s competitive advantage was better data utilization, but recent results do not, in my opinion, support this.

In my opinion, it was said that they have gotten rid of them or something similar, which I understood to mean that purchases have been made at a more reasonable price… but of course, one quarter is still so short that an outsider cannot see if weaker goods have been hidden in the inventory. However, the inventory did decrease, as it should with lower volumes.

EDIT: let’s correct that Q2 inventory actually grew by 11 MEUR, in Q1 it went down sharply, which means that during H1, total inventory decreased by 8 MEUR: