Eilen myytiin poikkeuksellisen paljon call optioita joka viittaa siihen että tietoa markkinoilla oli, mutta ei kaikilla

11 tykkäystä

13 tykkäystä

Tuleeko tulos ennen nysen aukeamista vai jälkeen? Tänään kai toi pitäs tulla ulos.

Taitaapi olla pörssin sulkemisen jälkeen, muistaakseni luin viime viikolla jostain, että 00:00 Suomen aikaa.

3 tykkäystä

Onnea kaikille omistajille!!!

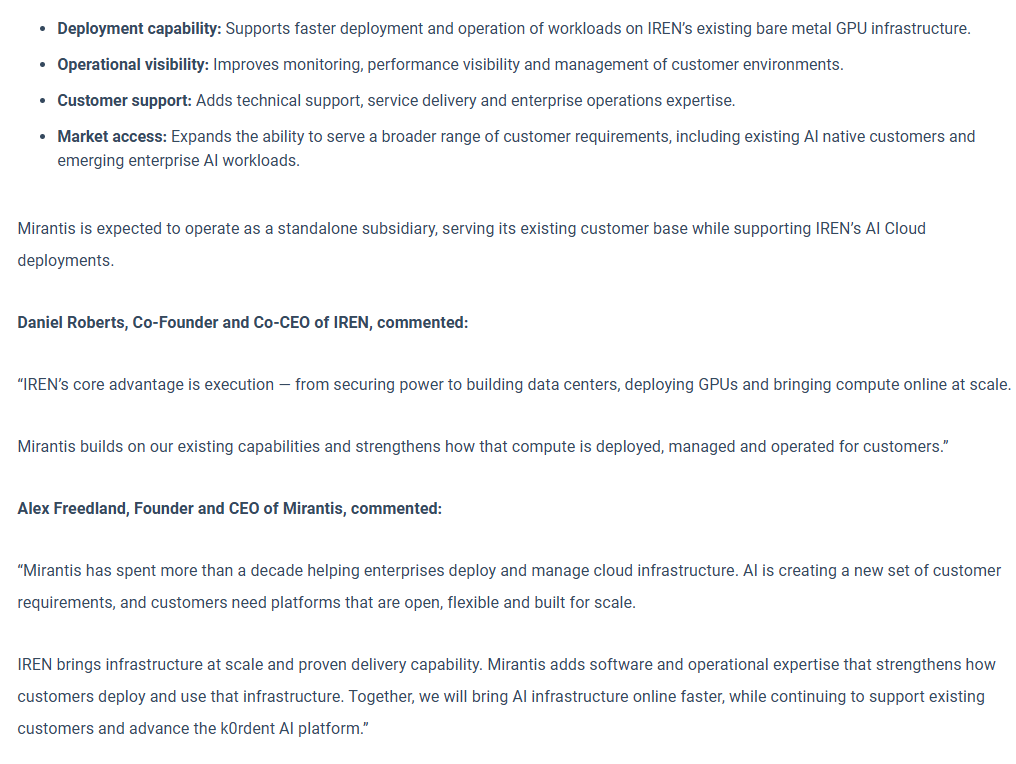

Osana kumppanuutta:

-

NVIDIA ja IREN aikovat tukea jopa 5 gigawatin NVIDIA DSX -yhteensopivan tekoälyinfrastruktuurin käyttöönottoa IRENin maailmanlaajuisessa konesaliverkostossa ajan myötä.

-

NVIDIA ja IREN tekevät yhteistyötä NVIDIA:n kiihdytetyn laskennan käyttöönotossa DSX AI -tehtaissa laajentaakseen pääsyä tekoälypohjaisille (AI-native), startup- ja yritysasiakkaille.

-

Osana kumppanuutta IREN on myöntänyt NVIDIA:lle viisivuotisen oikeuden ostaa enintään 30 miljoonaa kantaosaketta 70 dollarin merkintähintaan osakkeelta, mikä mahdollistaa jopa 2,1 miljardin dollarin sijoituksen tiettyjen ehtojen, mukaan lukien viranomaishyväksyntöjen, täyttyessä.

IREN Expands AI Cloud Platform to Europe with Acquisition of Nostrum Group

Yrityskauppa merkitsee IRENin tuloa Euroopan markkinoille ja kasvattaa sen tehoportfolion 5 gigawattiin (GW). Se tuo noin 490 megawattia (MW) varmistettua, sähköverkkoon kytkettyä tehoa Espanjassa sekä täydentävän kehityshankkeiden putken, mikä parantaa IRENin kykyä vastata havaittuun asiakaskysyntään Euroopassa.

33 tykkäystä

Ei herramajestas, tää ei ollut omalla bingokortilla.

TORILLE

10 tykkäystä

Ensimmäinen IREN-ostoni oli lokakuussa 2024, jonka jälkeen olen keskittänyt salkkua vahvasti Ireniin, etenkin viime vuoden tariffidipissä. Nyt täytyy sanoa, että on aika validoitu olo. Onnea muillekin omistajille!

19 tykkäystä

Mukana ollaan mut pakko kyl kysyä et onks tää joku kaikkien aikojen vivutus? Tiskiin laitetaa kaikki vanhat tuotot ja osakkeenomistajien taskunpohjalliset (6MRD ATM), toimittajien rahat (NVIDIA) ja asiakkaiden ennakkomaksut (Microsoft) ja sit kattellaan et miten äijien käy. ![]()

![]()

![]()

![]()

Tais olla jollain kalvolla että 3,7 jaardin ARR tahtiin -26 lopussa on jo sopimukset. Vai ymmärsinkö ihan väärin. On se hurja joka tapauksessa.

Kunhan AI kysyntä ei petä ni kai täs sit tulee rahaa ihan hyperscale-vauhdilla.

11 tykkäystä

Pakko myöntää ettei mulla enää ole oikein hajua mihinkä tällä kertaa on rahansa työntänyt (lol ihan ku joskus olisi). Pitää vaan luottaa että Nvidia on tehnyt DD Irenin osalta.

Tulevaisuus sen näyttää. Nyt vaan sormet ja varpaat ristiin.

15 tykkäystä

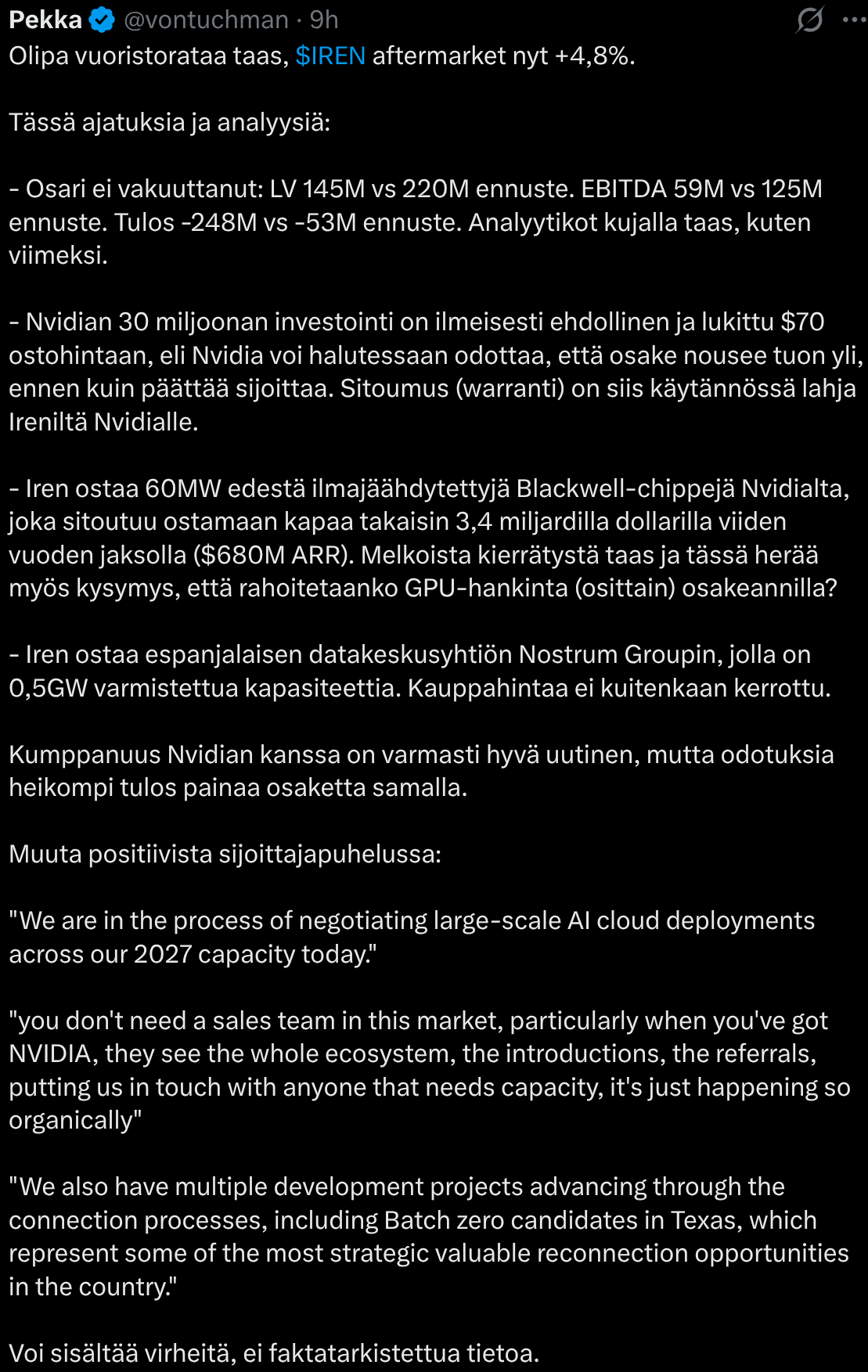

Pekan kommentti tuloksesta ja tuoreista uutisista.

https://x.com/vontuchman/status/2052527367017369624

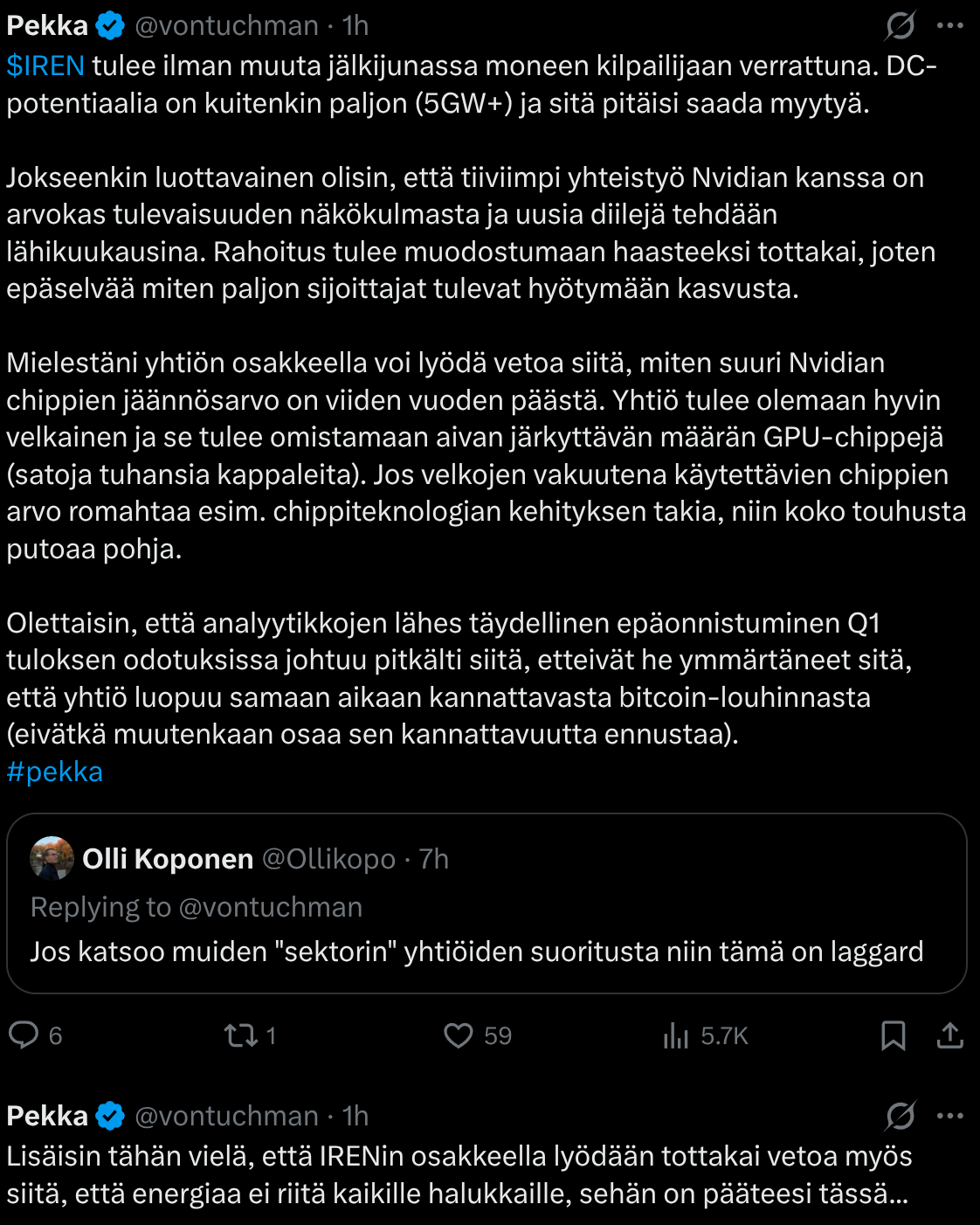

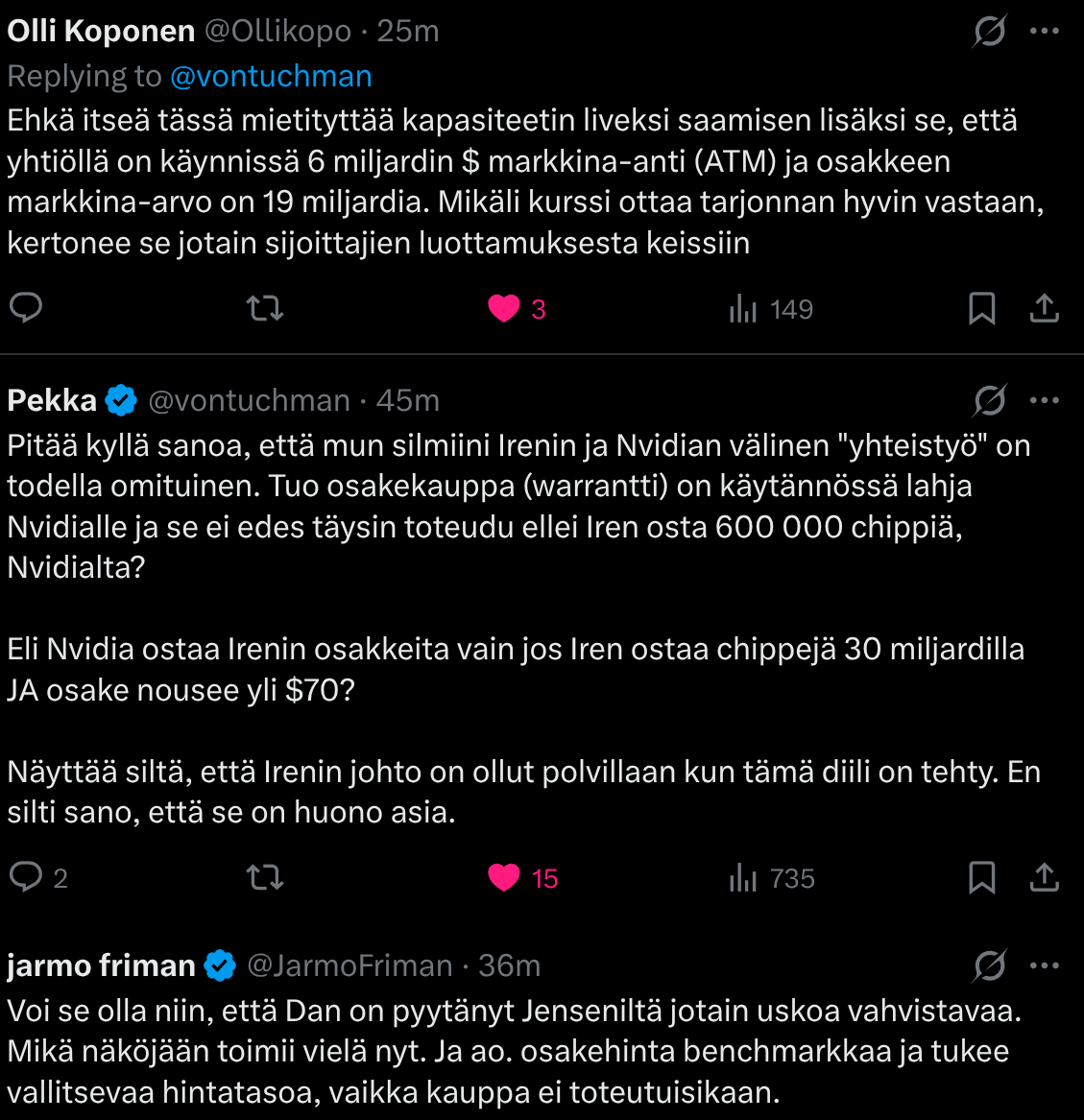

Edit. Lisätääs vielä nämä.

Ja lisäyksenä se että härkäisempiäkin analyysejä tuntuu tilanteesta löytyvän, mutta en lähde sokkona pumppauksia kopioimaan, kun en tiedä lähteiden uskottavuutta.

17 tykkäystä

Omaan silmään tämä uutinen vie IRENiä selvästi enemmän oikean AI-infratoimijan suuntaan eikä enää vain “Bitcoin-miner AI-slideilla” -kategoriaan. NVIDIA ei yleensä lähde tämän tason yhteistyöhön täysin kevyillä perusteilla, joten kyllä tämä lisää keissin uskottavuutta.

Samalla kiinnitin ehkä eniten huomiota itse rahoitusrakenteeseen. NVIDIA warrant-diili näyttää omaan silmään enemmän heidän erittäin vahvalta neuvotteluasemaltaan kuin miltään “ilmaiselta validoinnilta” IRENille. Käytännössä paljon nojaa siihen, että osakekurssi ja AI-execution kehittyvät oikeaan suuntaan myös jatkossa.

Eli vaikka puhutaan todella isoista summista ja potentiaalista, tämä on edelleen erittäin pääomaintensiivinen ja korkean riskin execution-keissi. Mutta samalla huomattavasti uskottavampi AI-infratarina kuin vielä jokin aika sitten.

12 tykkäystä

Viitaten edellä lainattuun influensseriin; ongelma näissä on se että tarve puhua paljon ja nopeasti on suuri.

Kyllä sieltä varmasti ihan hyviä näkemyksiä tulee sitten aikanaan jos hän jaksaa paneutua.

Minä lähestyisin asiaa Mungermaisesti insentiivien kautta.

Jos Nvidia tukee Ireniä nousukiidossa, ehkä jopa vähän mainostaa ja kehuu markkinoille, etsii sopivia kumppaneita ja yleisesti öljyää rattaita kaikkialla, se voi myydä GPUita en masse tähän valtavaan kapaan ja siitä kiitoksena printata rahaa warranteilla (aina 100k gpu toimituksen jälkeen).

Lisätään vielä että Irenin suurin ongelma eli gpu-saatavuus korjaantuu heti ja noustaan etusijalle (jos nvidia siis tykkää menestyksestä ja rahasta).

Siitä sitten vetoa lyömään, kuka minkäkin lopputuleman puolesta.

Edit:

Vähän parempi otto Nvidiasta, Irenistä ja Mirantisista:

https://x.com/franklee6924t/status/2053344382053503273?s=46&t=Gf87bhKtIDEQ8PoQTL96bQ

12 tykkäystä

Vielä tuli tänään tieto vaihtovelkakirjoista. Dilutaatio on todellinen. 2,3 MRD USD tämän instrumentin osuus. Jos kasvu ja laskutus toteutuu johdon maalailemalla tasolla niin ongelmaa ei tietty ole.

8 tykkäystä

Nämä ja se 6MRD ATM ovat siis ihan taskurahoja tässä bisneksessä. 1GW rakentaminen kaikkineen maksaa kymmeniä miljardeja - siksi Irenin ilmajäähdytteiset kyvykkyydet ovat painonsa arvoisia kultaa. Osassa Kanadaa ja Childressia pystytään retrottamaan vanhoja BTC louhintapajoja pilkkahintaan, tuottavat hyvää kassavirtaa ja lieventävät edes vähän rahantarvetta. Kunhan sinne saadaan niitä GPUta ![]()

Mutta nämä nestejäähdytteiset AI-tehtaat vaativat aivan sairaasti rahaa, joten niitä rakennellaan varmaan 250-300(brutto)MW kerrallaan (tuohon olisi tämän SN:n jälkeen juuri varaa). Ensi vuonna tulee satavarmasti uutta ATM:ää ja muutenkin rahoitukseen käytetään GPU/DC/sopimus-panttausta ja kaikkea mitä keksitään.

Notesit aiheuttavat sitten aivan kummallisia liikkeitä osakkeen hinnassa kun vanhoja suljetaan, haetaan hintaa uusille ja vaikka mitä. Tänäänkin niitä näkee.

Tämä on sitä mitä aggressiiviset kasvuyritykset tekevät, edellinen ATM pumpattiin $5-$15 hinnoissa ja diluutio kiritti meidät yli $70. Sitten kun diili ei miellyttänyt tai sitä ei ymmärretty tultiin alas kolmeen kymppiin.

Tarkoitan tällä sanoa sitä, että diluutio on normaalia kun kasvetaan ja yritys ei olisi ilman sitä päässyt yhtään mihinkään - sama koskee kaikkia pääoma-ahnaita kasvufirmoja.

Tällainen yritys joko tunnetaan erityisen hyvin, jätetään sijoittamatta tai mitoitetaan panos sen mukaan mitä vatsahapot kestää.

Jos on sitä mieltä että (kalenteri) q1/27 lv on yli miljardi (eli ARR ohjeistus saavutetaan/ylitetään) ja kasvaa harppauksin niin saattaa nähdä asian toiselta kantilta. Oletus on että jokainen miljardi joka lyödään kiinni tuottaa sitä LVtä todella pitkään ja siksi taseelle tulisi myös antaa arvoa eikä edes pelkän ARRnkään perusteella arvottaa.

(kalenteri) q1/26 AI lv oli kyllä suunnaton pettymys (oma target 65-85M) ja alleviivasi kuinka tärkeää oli saada tuo Nvidia kumppanuus vihdoinkin aikaiseksi. Liekö HBM-kriisi mikä hidastutti tuotantoa .. no sama se, tarvittiin etusija.

12 tykkäystä

Asia on juuri kuten kirjoitat. Kunhan nyt vaan listasin miten valtavalla vivulla ollaan liikkeellä. Ja kuten molemmat totesimme mitään ongelmaa ei ole KUNHAN kasvua tulee ja velkoja voi rullata eteenpäin.

Q1 liikevaihtoon jos vertaa niin nämä eri instrumenttien yhteenlasketut miljardit ei ole taskurahoja.

5 tykkäystä

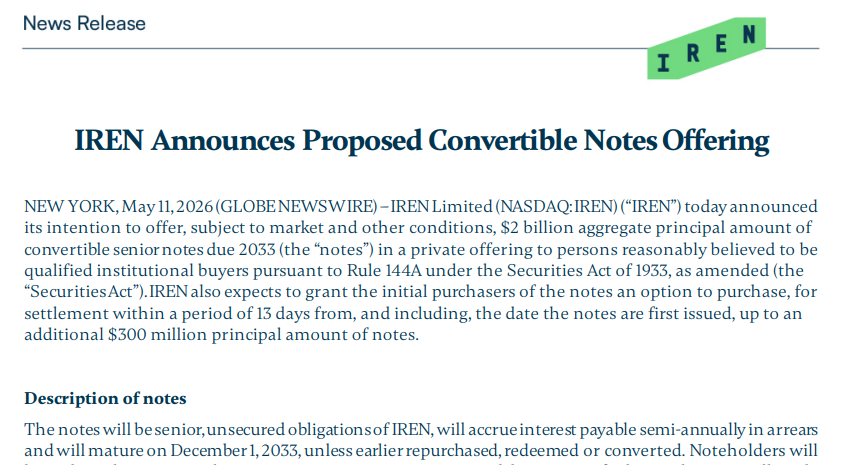

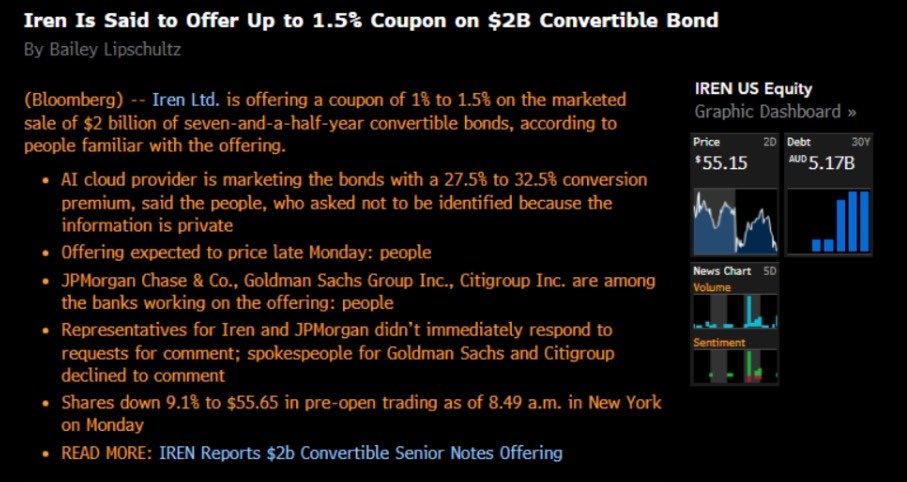

Emission ehdot

• Kuponki: 1,0–1,5 % (vahvistetaan hinnoittelussa)

• Koko: 2 miljardia dollaria

• Maturiteetti: 7,5 vuotta → eräpäivä noin loppuvuosi 2033

• Konversiopreemio: 27,5–32,5 % yli nykyisen kurssin eli nykykurssiin peilaten ollaan noin 70 dollarissa

Tähän on rakennettu laimentumista lieventämään “Capped Call” mutta sen ehtoja ei ole vielä kerrottu.

Huomiona että joulukuun 2025 emissiossa kuponki oli 0 %.

Hedge fundit ostaa tätä niin tulee paljon shottipainetta lähiviikoille kun hedgeävät Deltaa Convertible Arbitrage - strategiassa

6 tykkäystä

Puolet tästä summasta, vuosia lyhyempi maturiteetti

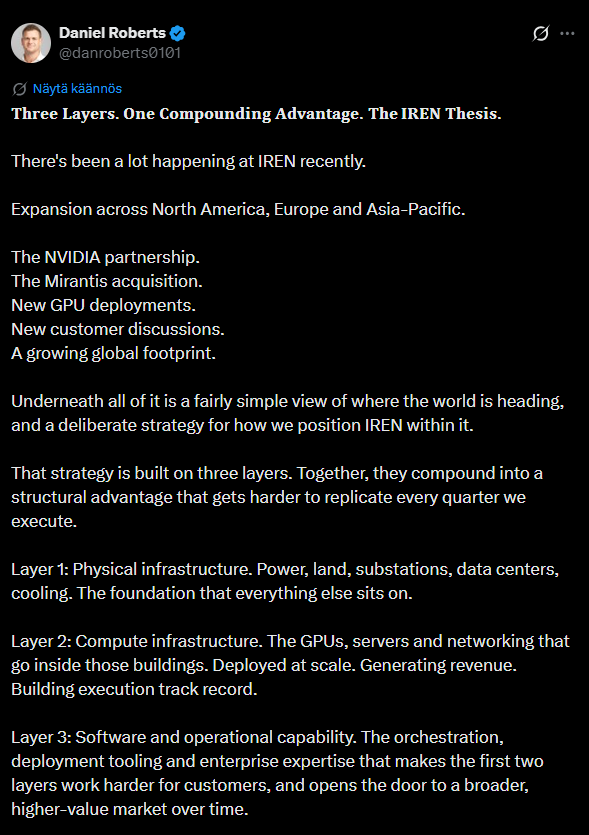

USAssa tällä viikolla kierrellyt toimitusjohtaja pisti eetteriin varsinaisen ensyklopedian firman perusajatuksesta, tavoitteista ja nykytilanteesta. Käsitellään myös miten uudet yhteistyökuviot ja yristysostot liittyvät visioon.

Tästä ei voi tehdä TLDRää - avaa, näe ja koe.

https://x.com/danroberts0101/status/2057755830443713024?s=20

Aloitussanat

19 tykkäystä

Tällä tyypillä on hyvää kontenttia Irenistä X:ssa. On tehnyt yli 50 sivuisen katselmuksen Irenistä, joista ilmasella pääsee lukemaan osan.

11 tykkäystä

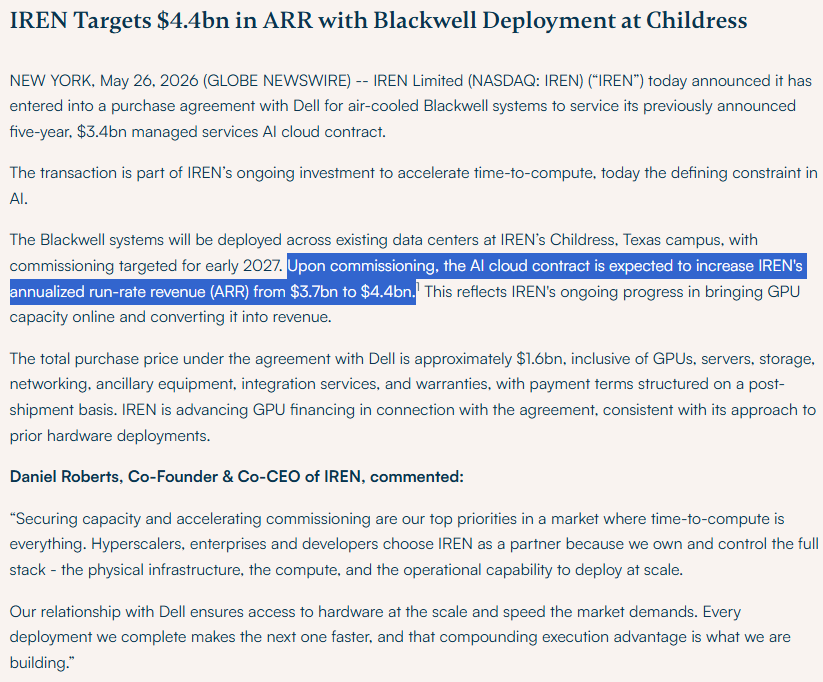

2026 vuoden lopun ARR tasoa nostettu tiedotteessa. (https://iren.com/investors/news)

Ihan lyhyessa ajassa ARR arviota on siis nostettu miljardilla. Tulosraportin aikoihin oli ensi nosto 3,4MRD–>3,7MRD ja nyt sitten edelleen → 4,4MRD.

Jos yhtiön johto ei nyt ihan ole valehtelemaan lähtenyt niin onhan tää huikeessa lennossa.

12 tykkäystä