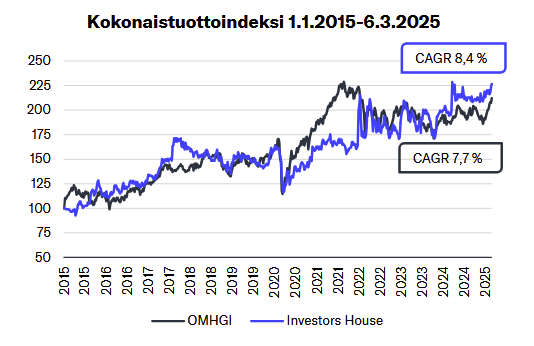

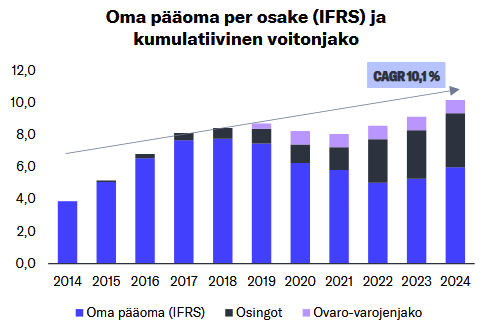

A special situation is currently underway due to a large dividend, but when looking at its history, it’s good to note that the current company’s history begins in 2014. The company has also distributed a significant portion of its assets as dividends. For this reason, a total return graph or cumulative equity and profit distribution are more sensible ways to examine the company’s performance than the share price.

When looking at the stock reaction, I’d like to remind people that you already own (in your current ownership stake in the company) that money. Now it’s just being transferred from the company’s balance sheet directly into your pocket.

IH has not created euros and value out of thin air overnight.

Thanks, I was already starting to feel like I was going crazy. This is a peculiar market inefficiency characteristic of Finland (?), but I can’t think of a good way to take advantage of it unless one has already bought the stock.

Am I wrong, but isn’t the market now starting to price in significant growth for real estate and service companies, because the dividend amount is constant? However, the service business is in its infancy and real estate is far from growth.

Roininen & co certainly seem to have expertise in the real estate market. They sold a huge number of apartments at peak prices during low interest rates. At the bottom of the construction and real estate wave, they managed to make big profits with the Kukkula project. Now that so much has been cleared from the balance sheet, new rabbits are needed out of the hat.

I really don’t remember a market reaction as absurd as the current one… I myself bought Investors House in spring and summer for about 5.25 euros, and I intended to hold it for a long time, but after reading Frans-Mikael’s comment this morning, I was able to anticipate an overreaction, though not quite this extreme. When the offer levels started to rise before 10 AM, I realized it was time to take the money and run.

Investors’ dividend frenzy for large dividends is always almost the same; I wouldn’t be surprised at all if the stock rose from here until the dividend ex-date.

Frans and @Petri_Roininen discussed, among other things, Q2 and the MASSIVE DIVIDEND!

Topics:

00:00 Start

00:18 Summary

01:11 Dividend

02:53 Apitare sale

03:33 Division into three

05:00 Service business

07:40 Real estate business

10:45 Market situation

I’m selling the company. Definitely not because of Maasiivinen’s dividend. But because you can get close to the sum of the parts from the stock market, and I don’t want to wait for the spin-off. In my opinion, other real estate sector stocks have more upside potential. And the previous commenter is indeed right, the title could be better…

I certainly wouldn’t blame Inderes at all for the absurdity of the market reaction; on the contrary, Frans-Mikael’s initial comment was calm and sensible. In my opinion, this is just an example of what the dividend frenzy that sometimes plagues the Helsinki Stock Exchange can lead to in extreme cases. It’s difficult to rationally explain how a company’s value would increase by 40% just because it announces one morning that it’s moving cash from one pocket to another. In my view, Inderes’ comments – unlike, for example, Kauppalehti’s articles sometimes – have, on the contrary, been very good at warning against fixating on dividend yield percentages, a tendency I also had as a novice investor.

Frans has prepared a new company report on Investors House.

Investors House’s very strong Q2 result was already known due to the capital gain, but it also exceeded our forecasts. However, attention was drawn to the board’s proposed giant dividend of 3.14 euros and the now likely division of the business into real estate and service operations. The company aims to build two separate growth companies, and Investors House’s historical track record in real estate business is excellent. Separating the service business unlocks hidden value from the balance sheet if the business turnaround succeeds and it serves as a good acquisition platform in industry consolidation. However, in our opinion, the share price clearly overreacted to the dividend news, which makes the short-term risk-reward ratio very weak in our view. We raise our target price to 6.10 euros (previously 5.90 €) due to the earnings beat, but we lower our recommendation to Sell (previously Reduce).

Our target price still includes the dividend for clarity.

The share price now seems to have truly stabilized at just under eight euros. This makes this irrational price movement perhaps even more comical: as if the pleasure of receiving a dividend had some kind of rationally determinable price, in this case, just under two euros per share. Anyway, to the point: What do you think, how will the share price behave after the ex-dividend date? IH’s real estate business has been high-quality, and I would gladly buy back my sold share of it once the valuation normalizes, but I somewhat suspect that not all the air will come out of the bubble after the dividend detaches. For a long time, however, IH’s formally absurdly high dividend payout ratio will be visible in various media tables, etc., so those who have now pushed the price to its current level may very well keep it there for some time, before reality dawns. My own guess is that the share price will only gradually normalize during the autumn.

From that 7.9 euros, a week after the dividend ex-date, it has come down a good 43%, and rightly so, to a lower level than where it was before the dividend decision. Many investors are probably wondering what to do with these shares now. I also like dividends, as Finnish companies rarely have smart uses for money, but this Finnish dividend frenzy sometimes takes on quite tragicomic features.

In my opinion, a reasonable benchmark is not the moment before the dividend decision, but the moment before the plan for the special dividend was announced, because that announcement didn’t create any value; it only raised the share price somewhat unjustifiably by over two euros. So, in my estimation, the fair value of the share should be roughly between 2.5 - 3 euros (= previous price 5.65 - dividend 3.01). The current price (4.5 €) should therefore fall by about two euros more before I would be interested in buying the shares back. The company itself is good, though.