Pieni sisäpiiriostos yhdeltä uusista johtajista, Annica Witschardilta. Epäilen kuitenkin ettei jää ainoaksi tälläiseksi.

4 tykkäystä

Tutustuin tarkemmin tähän Ålandsbanken analyysiin, joka näyttää siltä, että vedetty vaan viivottimella lukuja tulevaisuuteen. Antaa hieman “ruusuisen” kuvan yhtiön tulevaisuudesta. Tekstissä ei mitenkään selitetty läpi yhtiön velkatilannetta tai uudelleen rahoitustarvetta.

Raportin mukaan nettovelka suhteessa omaan pääomaan laskee tänä vuonna 408% –> 275%. Osaako kukaan täältä selittää miten tämä olisi edes teknisesti mahdollista Intrumin kohdalla?

Yhtiö on tehnyt merkittäviä alaskirjauksia taseessa viimeiset vuodet ja mikään ei anna olettaa, että alaskirjauksia ei tarvisi tehdä myös tulevaisuudessa.

Toinen hassu juttu oli toteamus, että Operating Margin (adj) on 40% vuonna 2028. Mistä lähtien velkoja voi periä 40% tuotolla? .

2 tykkäystä

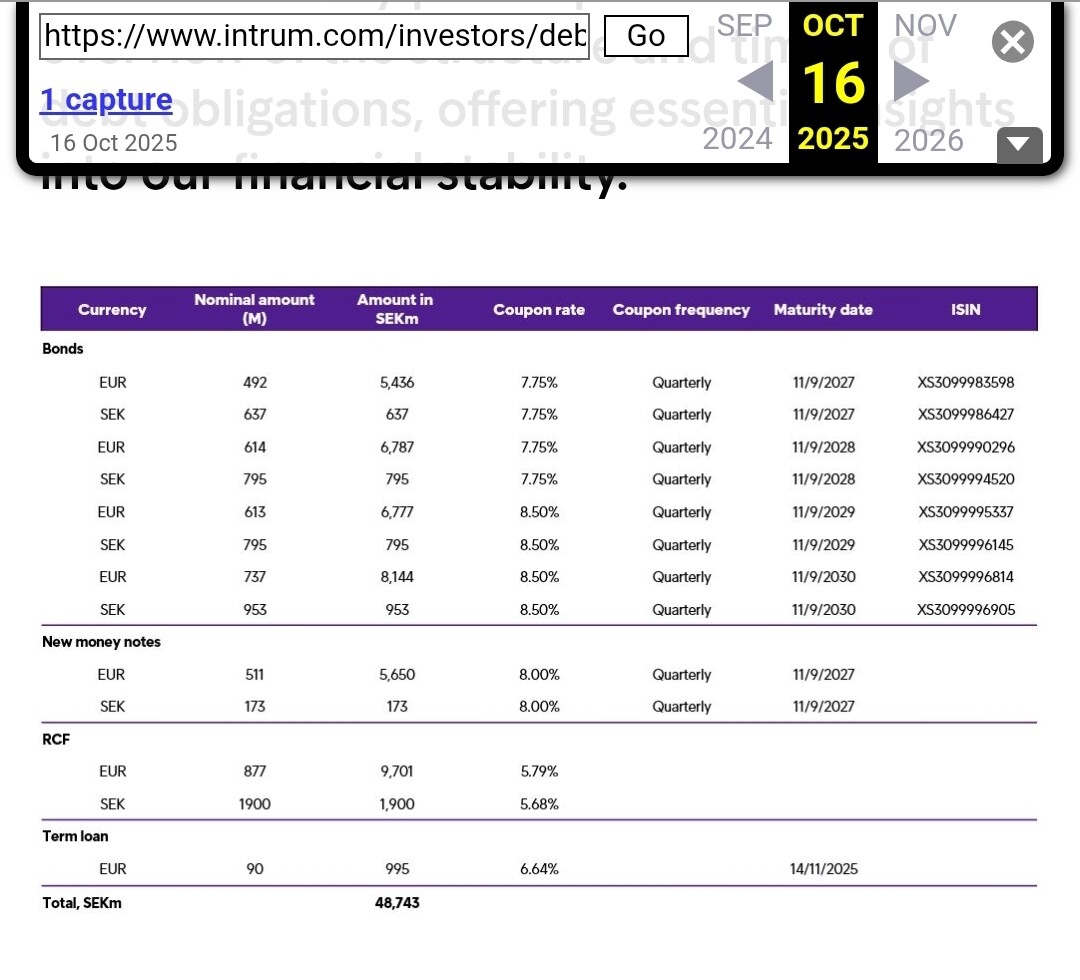

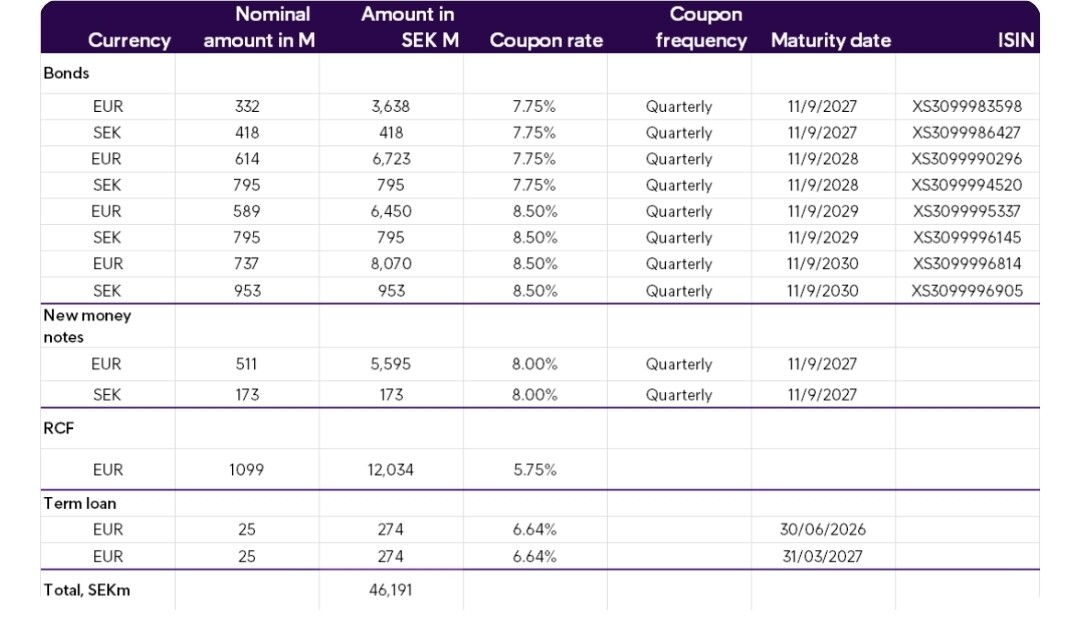

Tuli tämä taulukko mieleen, että 2027 bondit oli lähellä 100 pistettä ja muut vielä mateli.

Sitten käväsin katsomassa tuon Intrumin oman sivuston aikakoneella, niin olivat ostelleet noita 27 bondeja.

|16.10.25 | 15.12.2025 |

|

En tiedä miten usein he tuota sivustoa päivittelevät, mutta voipi tuota hieman seurailla.

Ja muita hiljaisia signaaleita noista portfolio ostoista (capital lightia), irtisanomisia ja vaikka Ophelos lanseerauksia tai tuubi esittelyitä.

En silti vielä ole kirvestä heittämässä kaivoon, kun vihdoista viimein tuo analyytikkorintama on aika suopeita Intrumia kohtaan.

5 tykkäystä

Lippu heiluu, mutta täysin “väärä” lippu. NC ilmeisesti lopettanut osakkeiden dumppaamisen ja jäänyt 10% siivun kanssa paikoilleen. Miksi? Innokkaimmat luonnollisesti spekuloivat, että tuo dilkataan kokonaan jollekin uudelle pääomistajalle, jonka jälkeen kaikki muuttuu täysin.

4 tykkäystä

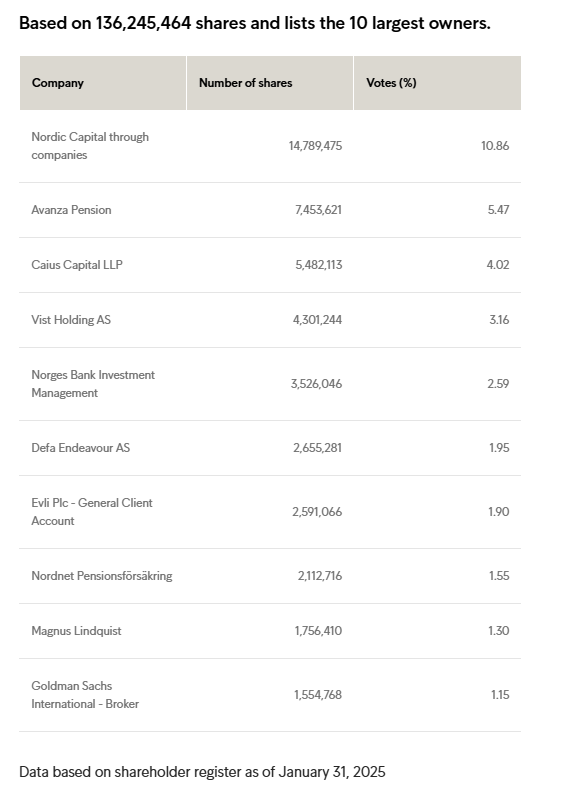

Uusi omistajalistaus tuli tammikuulta. Ammattimaisesti väärä vuosiluku perässä.

*NC ei ole koskenut pottiinsa, Caius taisi lisätä ja uutena tuorein tulokas ja osakkeita kauhonut Vist Holding AS.

7 tykkäystä

Ilmeisesti: Vist Holding AS emo on Steneken Holding AB jonka taustalla on taas non-profit Vidarstiftelsen…jos chat GPTä voi uskoa olisi tuo potti ~20% säätiön omistuksista. Täysin hämärää hommaa säätiön rahoilla, jos näin on.

3 tykkäystä

Uutisvirtaa (alla nordnetin AI-kooste kokonaisuudessaan):

Luottoluokitusnäkymää reivattu positiiviseksi, joskin Moodys säilyttänyt Caa2- luokituksen. Vähän sanahelinän puolelle menee, vaikka näennäisesti positiivnen uutinen.

Lisäksi UBS nostanut targettia ja eräs shorttari sulkenut positiotaan.

Luottoluokituslaitos Moody’s on tarkistanut Intrumiin luottoluokitusnäkymät vakaista positiivisiksi ja vahvistanut sen Caa2-pitkän aikavälin luottoluokituksen. Tämä luokituksen nosto heijastaa yhtiön edistystä velkaantuneisuuden vähentämisessä joukkovelkakirjalainojen takaisinostojen ja vakaan kassavirran ansiosta. Intrumiin uuden strategian, joka keskittyy velan vähentämiseen ja toiminnalliseen tehokkuuteen, odotetaan parantavan edelleen sen taloudellista asemaa, vaikka suhteellisen heikkouden odotetaan jatkuvan seuraavien 12–18 kuukauden ajan.

-

Moody’s nosti Intrumiin luottoluokitusnäkymät vakaista positiivisiksi ja vahvisti Caa2-pitkän aikavälin luottoluokituksen.

-

Luokituksen nosto johtuu Intrumiin velkaantuneisuuden paranemisesta vuoden 2025 toisen puoliskon joukkovelkakirjalainojen takaisinostojen sekä vakaan kassavirta-EBITDA:n ja kassavirran jälkeen.

-

Intrum suunnittelee velan vähentämistä edelleen tämän vuoden ensimmäisellä puoliskolla velkasalkun myynnillä ja vuoden 2027 joukkovelkakirjalainojen takaisinmaksulla.

-

UBS nosti Intrumiin tavoitehintaa 47 kruunusta 54 kruunuun ja säilytti neutraalin suosituksen.

-

Brummer Multi-Strategy pienensi lyhyeksi myytyä positioitaan Intrumissa alle 0,5 prosenttiin, lakaten olemasta julkinen lyhyeksi myyjä, vaikka 4,64 % pääomasta on edelleen lyhyeksi myytynä.

8 tykkäystä

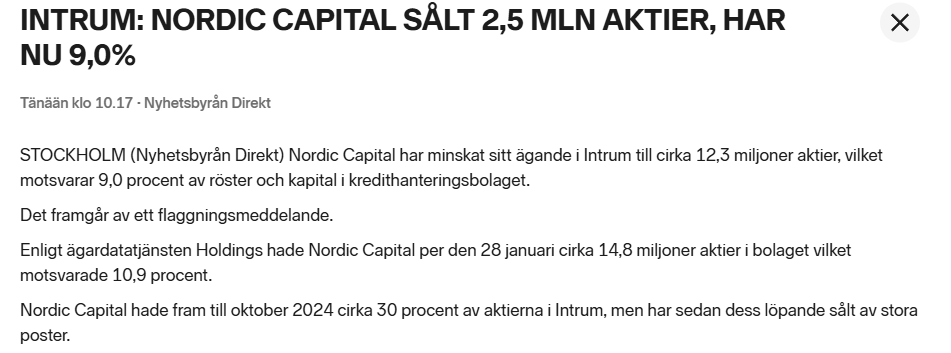

Tulihan se odotettu liputusilmoitus, eli NC jatkanut taas myyntejä ja alle 10% lippu heilahti. 2,5 miljoonaa osaketta lähtenyt. Tahti siis näyttää kiihtyneet, kun nyt lähti jo noin reipas kasa lyhyessä ajassa.

Tammikuu oli jostain syystä poikkeus NC myynneissä ja ihmettelinkin, kun osarin jälkeen ei liputusta tullut sekä tammikuun omistajalista näytti, etteivät olleet vähentäneet lainkaan.

Tätä tahtia olisivat sitten lopullisesti ulkona jo muutamassa kuukaudessa. Toivottavasti viimeistään kesään mennessä kuitenkin. Nyt kasa alkaa olemaan jo sen verran pieni, että voisi mennä blockinakin jollekin.

6 tykkäystä

Onkohan tuo määrä myyty blokkina jollekki taholle, kun liputusraja oli aika lähellä jo ennestään. Ja se ilmotus pitäs antaa melko pian ku raja rikkoutuu.

NCn lähtö on taas askeleen lähempänä.

Sitä vaan ajoin takaa, et NC ei enää olis rysäyttelemässä osakkeitaan ostotasoille…

5 tykkäystä

Blogikirjoitus joka herätti suuria tunteita Sharevillessa Intrumin cheerleadereissa:

Education of a Value Investor (Miscellaneous)

The Pitfalls of Discounted NAV: When Cheap is Actually Expensive

With real-world study cases on JM , UIE and Intrum

Feb 12, 2026

In the world of value investing, few metrics are as seductive as the Discount to Net Asset Value (NAV). It appeals to our most basic instinct: buying a dollar for 50 cents. It suggests a margin of safety, a free lunch, an arbitrage opportunity waiting to be closed. However, as all children growing into adulthood finally realized - parallel to naive value investors learning the hard way - there is no free lunch.

If you buy a holding company or a real estate developer solely because it trades at 30% below its NAV or Book Value, you are not necessarily buying value. You are buying a derivative of the underlying assets, attached to a specific business model, often laden with structural risks that the headline number ignores.

Join me on our journey as we dissect three specific cases where the “Discounted NAV” thesis falls apart when viewed through first principles, bottom-up analysis. This is our menu for today: JM’s illiquid inventory**, UIE’s** cyclical concentration and the accounting assumptions of Intrum.

Disclaimer: This article is not a critique of the long-term viability or quality of the companies mentioned. While there are many compelling reasons to hold these assets, the focus here is to highlight the specific risks of relying solely on a discounted NAV as a primary investment thesis. Valuation is rarely as simple as a single metric.

(All the numbers are written as of 11 Feb 2026 and may be subject to my personal error)

Case Study 1: The Time-Value Trap (JM AB)

The Discounted NAV:

JM AB is a Nordic residential developer. The current market cap is 8.79B SEK, while the reported NAV is 7.9B SEK. The company also reports that there is a massive hidden “surplus value of development properties” in their building rights portfolio (land bank) of ~5.0B SEK that is not reflected in the balance sheet. This hidden NAV is most possibly marked to market.

When adding the hidden surplus (7.9B + 5.0B), the implied NAV suggests that the share price is trading at ~30% discount to its NAV.

The Pitfall:

This argument confuses Inventory with Assets.

JM AB owns land (building rights). They cannot mail you a plot of dirt. To realize this surplus NAV, JM must process, build, and sell apartments over decades. The discount is simply the market applying a discount rate to future cash flows.

The Numbers:

Let’s calculate the Present Value (PV) of that headline 5.0B SEK surplus.

Inventory Size: ~35,400 building rights

Production Rate: ~2,300 starts per year (recent run-rate)

Years to Realization: 35,400 / 2,300 - approx 15.4 years

Nominal Surplus Flow: 5.0B SEK / 15.4 = ~325M SEK / year

Discount rate: 10% (12.5% cost of capital offset by 2.5% land price appreciation)

This is effectively a DCF limited to 15 years. The resulting PV is roughly ~2.5B SEK.

The market isn’t ignoring the discounted NAV; it is discounting it for time. By the time JM converts the last building right into cash, the cost of time and capital has eaten 50% of the value. When you add 7.9B and 2.5B, the result is 10.4B SEK. With market cap of 8.79B SEK, this is still a discount of 15% to NAV. Well, there is also the problem with our assumptions. For example, we assume the production rate to be 2,300 starts per year, while in reality the numbers may vary between 1,500 to 4,000 starts per year. We also apply no discount on the not-hidden NAV of 7.9B SEK.

Investing in JM AB needs consideration on the time value of money and the execution risk. This is why the market puts a discount to the their NAV.

So, what’s the alternative?

Use Margin of Safety. Currently we are at ~15% discount to Net Present Value (if you believe my calculation). If the discount widens to >30%, then it is potentially time to look at JM closer.

The pitfall of the pitfall:

This calculation assumes minimal (2.5%) land appreciation. If land prices rise by 5% annually while JM holds it, the “Surplus Value” grows over time, partially offsetting the discount rate. However, trusting a 15-year inflation forecast to bail out your valuation is speculation, not investing.

The most important thing - following Howard Marks

I want my dear readers to use Margin of Safety when evaluating an investment. The Margin of Safety concept is essential regardless of valuation methods.Case Study 2: The Cyclical Peak Trap (UIE vs UP)

The Discounted NAV:

Let’s look at UIE (United International Enterprises). It’s a holding company with a NAV derived largely from the market price of its largest holding, United Plantations (UP). Looking at UIE’s current market cap and NAV, you see a ~30% discount. The logic seems clear: Why buy UP directly when you can buy it through UIE for cheaper?

The Pitfall:

This logic ignores Mean Reversion.

This logic assumes the current market price of the underlying asset (UP) is the correct anchor for value. UIE is not a diversified compounder like Investor AB or Berkshire Hathaway. In those vehicles, if one holding is at the top of its cycle, another might be at the bottom. The portfolio effect smooths the NAV risk.

UIE is effectively a mono-line bet. While UIE does hold a stake in Schörling AB (giving some exposure to diversified basket like Hexagon and Securitas), United Plantations currently accounts for approximately ~80% of UIE’s total NAV. Its fate is mathematically tied to palm oil.

The Numbers:

Let’s look at United Plantations (UP) in terms of P/B (Price-to-Book), EV/Ha (Enterprise Value per hectare of lands) and its premium valuation to peers (based on their Q3 2025 and website).

Market Cap 18.81B MYR

Net Cash 566M MYR

Enterprise Value = 18.81B - 0.566B = 18.24 MYR

Book Value 2.93B MYR

Total Planted Area ~51,000 Hectare

Current P/B: ~6.4x. Historical P/B: ~2.5x

Current EV/Ha: ~350k MYR. Historical EV/Ha: <150k MYR

Current premium to peers: ~5x. Historical premium to peers: 2-3x

UP is currently trading at over ~2.5x its historical median valuation. On top of their record high valuations (a commodity company with a 6.4x P/B is insane to me!), their margins are also near record highs compared to their historical numbers. This signals a peak cycle. The underlying asset is priced for perfection, sitting at a cyclical peak fueled by CPO (Crude Palm Oil) prices. If UP’s valuation mean-reverts to ~3x P/B (still a premium to history) i.e. drop by 50%, the UIE’s NAV would effectively drop by 40%. Did you get the math?

You buy $1.0 of UIE’s NAV for $0.70. You’re happy.

UP mean-reverts**.** That $1 of NAV re-rates to $0.60 - your $0.70 entry is now a massive premium to the new reality. Are you still happy?

So, what’s the alternative?

Don’t Buy the NAV. Buy the Normalized Earnings. Value UIE on “cycle-normalized” earnings of UP. Calculate the average earnings of UP over a full commodity cycle (5-10 years). Apply a historical multiple (e.g. 15x) to those normalized earnings. If UIE trades at a discount to that number, you have a Margin of Safety.

The Pitfall of the Pitfall

The analysis assumes historical valuation pattern will repeat. One would argue that the palm oil market has structurally changed (due to ESG planting restrictions limiting supply), meaning UP deserves a permanently higher multiple. If this time is truly different, UP’s share price will stay high and UIE’s NAV will not collapse. On the other hand, I would put my money on history rhyming.

The most important thing: I want my dear readers to critically evaluate an investment thesis on holding companies trading at discounted NAV. Not all holding companies put their eggs in many baskets, some of them put most of their eggs in one basket hanging 10 meters above the ground.

Case Study 3: The Accounting Assumptions (Intrum AB)

The Discounted NAV:

Intrum (the debt collector/credit manager) seems to be deeply undervalued, trading at a fraction of its Book Value (Equity). Investors may point to the fact that they own massive portfolios of NPLs (Non-Performing Loans) and recently sold a chunk to Cerberus at a price close to Book Value, seemingly validating their accounting.

The Pitfall:

The “Book Value” of an NPL portfolio is an “accounting” value, which is entirely dependent on the Discount Rate used to value future cash flows. Intrum uses internal models (ERC) with a discount rate of 10-15%. Quoting from the Q4 2025 report “…discounted at the effective interest rate as determined at the time of the acquisition…“ - the report seems to use 13%. Essentially, the lower the discount rate the more “Book Value” the NPL will show.

On the opposite spectrum, we can see how much the market values the same risks by looking at the yield to maturity of Intrum’s own bonds - which range depending on maturity dates. These yields are higher than 13%, reflecting market concern.

The July 2026 bond yield is ~20%

The March 2028 bond yield is ~13%

The September 2029 bond yield is ~14%

When Cost of Capital > Return on Invested Capital, value is destroyed, not created.

The Numbers:

Let’s strip the accounting and the balance sheet down to see what the equity is really worth if we mark the debt portfolio with another discount rate.

- Value the “GoodCo” (Servicing):

The servicing business is capital-light. Let’s assume a somewhat generous 9x multiple based on the reported FY 2025 reported EBIT of ~3.5bn SEK.

GoodCo’s Intrinsic Value = 31.5B SEK

- Value the “BadCo” (NPL Investments):

According to the Q4 2025 report, the BadCo’s NPL portfolio has a Book Value of ~22bn SEK from a total ERC of ~46B SEK, discounted with 13% effective rate. If we re-price this at 16% yield, the actual present value drops by ~15%.

BadCo’s Intrinsic Value = 22.0 x 0.85 = 18.7B SEK

- Intrum’s Intrinsic value:

Total EV - Net Debt = (31.5B + 18.7B) - 44.0B SEK = 6.2B SEK

The “Book Value” of Equity is reported as 12.78B SEK in the Q4 2025 report, but the economic value might be closer to 6.2B SEK with non-conservative assumptions. If you buy at the current 6.75B SEK valuation thinking you are getting a ~50% discount to Book, you are actually paying at a slight premium to Intrum’s intrinsic value (if you believe my calculation).

So, what’s the alternative?

Value the GoodCo, Zero the Book.

The NPL portfolio is tricky to value due to the accounting assumptions. Let the debt holders own it. Calculate the intrinsic value of Intrum based solely on the Servicing business and the Net Debt. Looking at the current situation, the Servicing’s intrinsic value is actually “underwater” due to the Net Debt. Wait until it grows its EBIT, or the Net Debt lowers significantly (e.g. more sales of the NPL to pay down debt).

The Pitfalls of the Pitfalls

You cannot easily amputate the “BadCo” from the “GoodCo” like I did here. The Servicing business relies on the Investment book to feed it volumes. If Intrum stops investing, servicing revenues may decline. Furthermore, the Cerberus sale suggests someone is willing to pay near the accounting Book Value, though skeptics would argue that the sale was subsidized by the attached long-term servicing contract.

I also must admit that the market’s pessimism may eventually create massive opportunity if Intrum can successfully refinance its debt. However, banking on such a gamble is a speculation, not fundamental investing.

The most important thing: I want my dear readers to be patient. I understand that a turnaround may promise an exponential returns. However, Intrum’s turnaround is complex and the numbers show that the investment is in speculation territory. I would bide my time - quoting Peter Lynch “what is important is to wait for the actual evidence of the turnaround occurring, not just the symptoms.”

The Quick-Fire Pitfalls: Other Discounted NAV Illusions

If the above three aren’t enough to make you skeptical, here are some other quick-fire pitfalls:

The “Debt-on-Debt” Trap: A holding company that owns a subsidiary. Both carry debt. Even if the subsidiary makes money, it is forced to keep the cash to please banks and rating agencies. This leaves the parent high and dry, not being able to get the cash and pay its own bills and debts. The NAV is there, but you can’t touch it.

The “Class War” Trap: This is a structural trap where common shareholders are the last to eat. Preference shares act as “proxy debt” with a senior claim on both dividends and assets. In a stagnant company, their mandatory payouts function as a persistent tax, slowly bleeding the common NAV you thought you bought at a discount. If the company’s value drops, the preference holders stay “at par” while the common equity absorbs 100% of the blow.

The “Development Projects” NAV: This is similar to the accounting trap, but often applied to infrastructure projects. The company reported NAVs based on “Mark-to-Model” valuations of development projects (e.g. offshore wind, hydrogen). These are highly sensitive to interest rates. When rates rise, the project NPVs turn negative long before the quarterly report admits it on-paper.

Conclusion

When you see a company with discounted NAV, ask yourself: Is this a mispricing, or is it the market correctly pricing the risks? In most cases, it’s usually the latter.

NAV is an opinion. Cash flow is a fact.…

*

Disclaimer: I am not a licensed financial advisor. I do not hold positions in the securities discussed. The content provided in “The Northside” is for informational and educational purposes only and represents the personal opinions of the author. It is not intended to be, and does not constitute, financial, investment, legal, or tax advice. Investing involves risk, mostly the risk of losing money because you listened to a stranger on the internet. Do your own due diligence.*

Lähde: The Northside | Substack

3 tykkäystä

Se mikä itseäni eniten askarruttaa on että miksi pääomistaja myy koko ajan kovaa vauhtia osakkeitaan pois näillä hinnoilla (ei kai sielläkään ole osaamatonta porukkaa arvioimaan yhtiön arvoa ja mahdollisuuksia) ja vastaavasti yhtään isoa ostajaa ei ole ilmaantunut noita ostamaan blokkikaupalla (sama sulkuhuomia).

Sharevillen faniporukan kommentointi on lähinnä lähentänyt sormeani myyntinapille.

1 tykkäys

Kirjoituksen tekijä Northside oli vähän peruutellut Placera-foorumilla. Hän ei ollut huomioinut että -26 velat oli jo hoidettu ja oli myöskin käyttänyt liian isoja korkoja jäljellä oleville veloille. Placera Forum

6 tykkäystä

Nordic Capitalin myynithän johtuvat siitä että he ovat sääntömääräisesti sulkemassa rahastoa, ja varat täytyy palauttaa omistajille. Intrum on ollut vain osa sitä kuviota, ja vaikka heillä on ollut iso osuus firmasta, on rahasto ollut niin iso ja pitkäaikainen että Intrum-osakkeiden loppuhinnan optimointi ei ole heille rahaston lopputuoton kannalta merkitsevää. He ovat saaneet siitä vuosien varrella isot osingot, ja rahastossa oli muitakin firmoja. Rahasto vain täytyy sulkea. Parempi tietysti olisi jos he olisivat saaneet blokkikaupalla lapuille uuden omistajan, mutta se ei toistaiseksi näytä onnistuneen. Nyt voi tietysti toivoa että blokkikauppa onnistuisi pian.

8 tykkäystä

Itekki luin tuosta Bamfordin linkistä vain alun ja Intrumin kohdan. Sitten kun siinä alettiin puhua 2026 rahoituksesta ja jopa 20% rahoituksen kuluista niin lopetin lukemisen. Samalla toisella puolella jätettiin huomiotta miten paljon investing portfolion odotetaan tuottavan pitkässä juoksussa.

Eikä viittiny myöskään samalla teilata, hyvähän se on sinällään kaiken maailman näkemyksiä laitella.

Mutta tuo artikkeli oli kyllä huti. Siinä oli heitetty pitkälti päästä mitä vaan mieleen juolahtaa.

Voihan siitäkin toki opiksi ottaa, ettei alhaiset arvostukset sinällään tarkoita välttämättä hyvää entryä. Ainahan niille alhaisille arvostuksille on joku syy, mutta samalla hengenvedolla pitää huomioida ettei alhainen arvostus itsessään myöskään tarkoita automaattisesti huonoa entryä. “Markkina hinnoittelee aina oikein” on ajatusmallina kuitenkin todettu vääräksi monen monta kertaa, vaikka se toki oikeaankin voi osua yhtä lailla.

… Ja tämän takia Intrumin suhteen pitää seurata kassavirtoja ja projektoida tulevien vuosien tuottoja. Isoin riski nyt lähinnä on että vastoin johtajien puheita laitetaan massiivinen anti tulille ja kiirehditään velkataakan kanssa, mutta ei Intrum konkurssiin ole enää menossa.

5 tykkäystä

Onko tälle lähdettä? Olen tätä koittanut selvittää mutta en ole löytänyt varmistusta väitteelle vaikka se tuntuukin olevan konsensus usealla foorumilla.

Kiitokset kaikille Northsiden blogia kommentoineille.

3 tykkäystä

En osaa sanoa lähdettä, missä lukisi selväsanaisesti että NC VIII on elinkaarensa päässä joten tyhjennämme portfolion, jotta voimme aloittaa uuden portfolion kasaamisen, jossa tuemme seuraavia yrityksiä kasvun ja kehityksen tiellä.

Tämä nc viii on 2013 vuonna perustettu, ihan koko historiaa en ole tutkinut, missä kohtaa Intrum astui kuvioon. Mutta viime aikoina ovat olleet myös Noba bankin omistustaan purkamassa.

Ja NC kotisivuilta saa infoa, että he eivät ole jäämässä ikuisiksi omistajiksi. Intrum on ilmeisesti statuksella “tehtävä suoritettu” omistus puretaan vähitellen.

Seurasin joitai toisiakin yhtiöitä, jossa tämä nc fund viii on omistaja niin myynnit on jatkuneet näissäkin. Ei tämä exit koske pelkästään Intrumia ja vaikuttaa enemmän rahastorakenteen logiikalta ja sääntöihin pohjautuvalta toiminnalta kuin että Intrum kaatuu, joten exit.

Ja ennen kriisiä NC teki ihan hyviäki kotiutuksia myymällä Intrumia yli 200sek. Sit osingot lypsetty, joku on saattanut laskea osto hinnan millä NC osakkeitaan on ostanu/saanut…

6 tykkäystä

Samassa kohdassa itsekin loppui kiinnostus siihen artikkeliin. Eli pohjatyötä ei oltu tehty juuri lainkaan tai sitten vaan tekoälyllä hutaisten. Hienosti kuitenkin kirjoittaja myönsi virheensä Avanzan puolelle.

Jos haluaa vähän syvällisemmän analyysin joka on vähän härkämäisempi, niin tuossa on norjalaisen ilmeisesti Nordean juniorin tekemä. Tai ainakin päättelin linkedinin perusteella junnuksi, koska oli vielä opiskelija.

Intrum writeup.pdf (593,1 Kt)

8 tykkäystä

Niin se vaan on, että kaikki gapit tulee täytettyä. Intrum kävi täyttämässä tuon 9.1 tuleen gapin kun käytiin 40.29 kr. Alas mennään sen verran isolla vaihdolla tänään, että NC taitaa nyt painaa oikein kunnolla lappuja pihalle.

On muuten pisin laskuputki 5v aikana, eli 10 päivää pelkkää punaista ilman pienintäkään reboundia. Valitettavasti ei olla vielä edes daily os, joten lasku saattaa jatkua pidemmälle alle 40 kr.

11 tykkäystä

Kuuntelin Q4-puhelun:

-

Rivien välistä luettava, että Investing-puoli ollaan laittamassa kokonaan rahoiksi pakon edessä. Tähän viittaavat myös uudet tavoitteet.

-

Menetetty tulopuoli korvataan Servicen suuremalla voittomarginaalilla (35%). Tämä tapahtuu pääasiassa kuluja leikkaamalla

-

Intrum uudelleenrahoittaa tänä vuonna H1 vuoden 2027 velat osittain kassavirralla (1/3) ja osittain markkinoilta lainaamalla pääomalla. CFO uhosi, että saavat paremmat ehdot markkinoilta kuin nykyisten lainojen ehdot.

Mielenkiintoista nähdä miten tulevien vuosien rahoitus hankitaan markkinoilta, todennäköisesti se tulee olemaan jollain tavalla sidottu omaan pääomaan. Onko kenellekään täällä ideoita miten rahoitus tullaan hankkimaan markkinoilta?

1 tykkäys