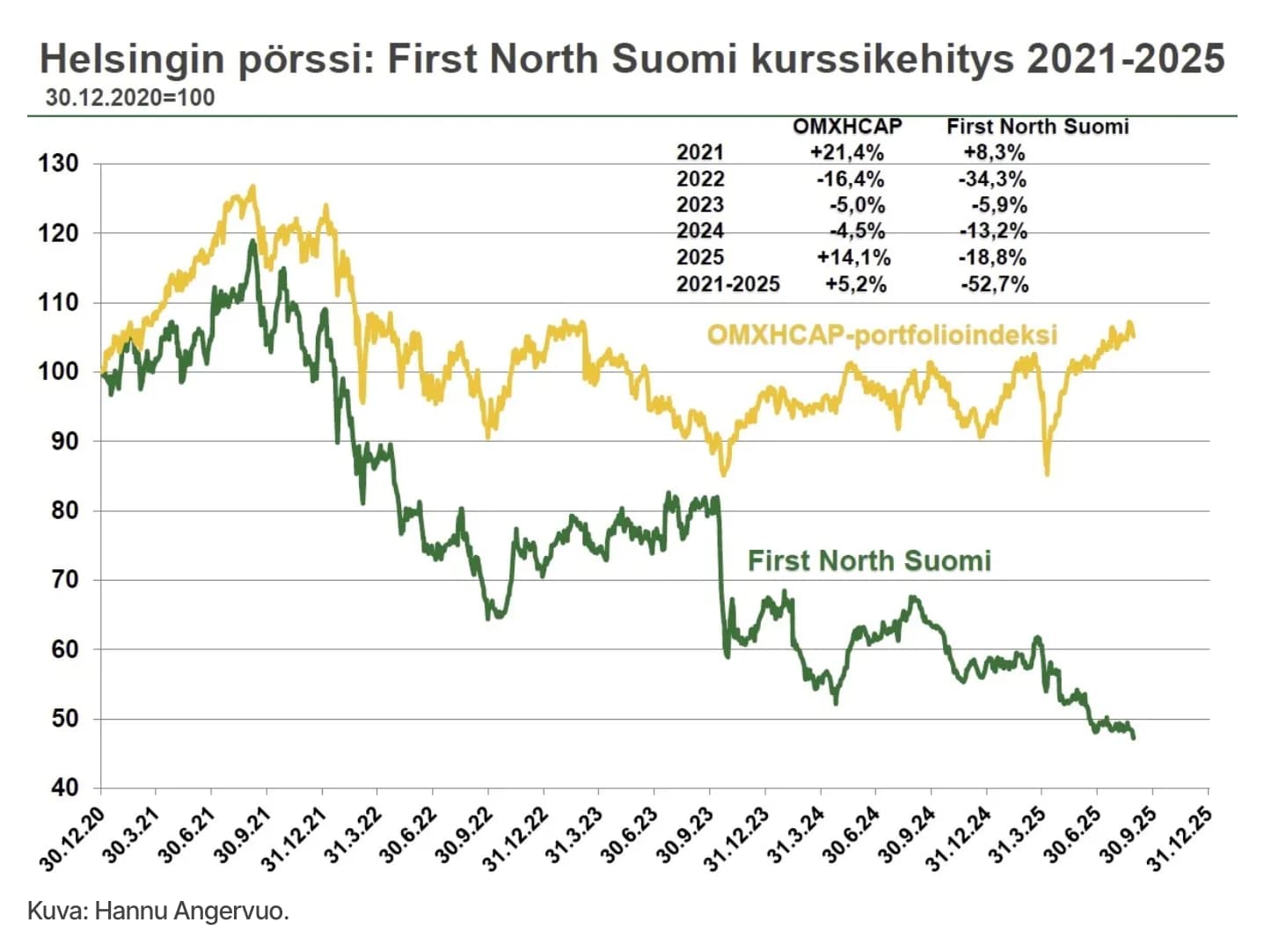

I, at least, view First North companies as part of the entire stock market, but as a list, it has been a bomb in recent years. ~60% down from its peaks. The OMXH Small cap index, i.e., small companies on the main list, is, however, “only” less than 40% down from its 2021 peaks. The OMXH Small cap has also recovered slightly from its lows.

This probably explains the gloomy sentiment on the forum. If you look at Helsinki’s large companies, we are practically at an ATH (All-Time High) with dividends. Nordea, Finland’s most popular company to own, is at an ATH. The national stock Mandatum is almost at an ATH, etc. But there are a lot of small-cap focused pickers here.

On the other hand, among the larger and popular players, for example, Neste, Qt, and Tietoevry have crashed, and Nokia is going nowhere.

The good thing about that little-known index is that, compared to it, many portfolios have certainly outperformed in recent years.

Thanks for the long answer! This is a good justification for the fact that an individual’s knowledge of a company still represents an individual’s knowledge, and doesn’t necessarily provide essential background in a changing world where everything is constantly in motion. However, regarding tech/software companies, I can generally say that if, in my job role, I notice product development lagging and mandatory migrations or technology conversions are missing, then moving forward, the legacy will always hit a wall, and newer competitors accelerate their pace.

This topic is therefore a good indicator for an investor because a company’s dynamic is often one or the other. Either there’s a good product development culture or a good sales culture. Having both in a company is, in my experience, rare. Poor management may not understand that in a software-centric product company, the maintainability and development potential of the product are more decisive in the customer’s eyes. So, real money must be invested in this, not just empty promises. At worst, one sees that it is precisely the salespeople who jump from one software company to another when they themselves realize how the basic product cannot withstand competition, meaning it doesn’t benefit the salesperson either.

Well, my whole idea originally stemmed from the fact that at work/as a customer, one often encounters listed companies, and when one gets a good insight into their products, it changes the investment case, if one had such a case in mind for the company before. Perhaps in summary, one could say that if an investor gets in contact with customers of company X, Y, or Z, it is precisely those customers who can sometimes provide revealing information that can positively influence one’s thoughts. This is, of course, difficult to apply to something like Kamux, but it’s more effective in software companies when considering business customers.

Foreign holdings in Nordic early-stage companies are just rounding errors. Revenues are smaller than the salary costs of the teams screening them; the goal is to get

Lapwall is the first company that comes to my mind regarding this. My own experiences with that company are old, but they were particularly negative. In my opinion, it’s a rather risky company. Despite this, it is currently trading at multiples that, in my opinion, would require the vast housing stock built between 2016-2022 to be fully occupied, at least 1 successful data center project already completed, and certainty about a decrease in timber prices. According to Inderes’ forecasts, Lapwall’s EV/EBIT for 2025 is 23, and adjusted, 17.8. For comparison, Qt’s EV/EBIT is 18.3, and adjusted, 16.1. I personally consider Qt’s opportunities for profitable growth significantly higher than Lapwall’s. Both can, of course, succeed or fail, but I simply don’t understand Lapwall’s multiples.

In my opinion, there’s a somewhat similar phenomenon visible here as in the ongoing discussion of company chains vs. one’s own experiences with companies.

A company’s product, let alone its quality, does not necessarily determine a company’s stock market journey in any way if the industry is right or even slightly bubbled. More than quality issues, investors are interested in stories and future potentials, whereas within the company (excluding management team work) often only the delivery phase of already completed deals or, at most, the sales pipeline is visible. The potential of product development, on the other hand, cannot really be sensed from within the company. Then, when these are told by someone else, we cannot be sure of their position in the company, their perspective, what is opinion and what is fact…

Even if one wanted to draw conclusions from these ‘tea leaves’ to support investment decisions, in my opinion, they are not really suitable for that. Nowadays, in the golden age of investment scams, one should in any case approach all sorts of online narratives, if not with hostility, then at least with healthy skepticism.

In a long bull market and stable environment, small-cap companies can be real gems if they are doing well. They are cheap, and initially, only private investors can get involved. A rising stock market and reasonable economic performance encourage saving more into stocks, and some of that money flows into these small companies. Eventually, their market values grow so large and stock turnover reaches a level that institutions can also get involved. The rise thus gains further momentum from increased buying pressure.

The same effect is now turning in the wrong direction in a bear market and a difficult economic environment. Small-cap companies are crashing, digesting the growth companies of previous years, which does not encourage investing in them. Why buy today if you can get the stock cheaper after a couple of negative news in six months? A classic deflationary problem! At the same time, among private investors, their own finances may be tight, or the fear of job loss may be high. Then there’s no desire to tie up their money in some illiquid ‘Nordic early-stage’ index setup. When companies don’t look appealing, or even if they look at least reasonable, the crowd is mainly on the selling side. Institutions are mainly trying to get rid of these, or have gotten stuck in them. A takeover bid would be almost the only lifeline for large owners.

A kind of small-cap winter, then. This could take a few years, but fortunately, the current winter has already lasted several years. Surely spring will come again someday. At least these are no longer spoiled by price, although the group is a mixed bag and one shouldn’t paint too many generalizations.

Pah, even Fitnesstukku isn’t like it used to be. In past years, I got used to being able to pick up my stuff from the pickup locker in a couple of days. I got around to ordering creatine and other “analog stereos” last Friday, and I still haven’t even received a shipping confirmation…

Why can’t this be turned around on a principal level? Pohjola’s first courses have dropped en masse, and in hindsight, that has been an opportunity for companies to raise funding against unrealized value. That’s certainly tempting, because who wouldn’t want uncompensated money where the outcomes are IPO money or the company’s success in addition to that. In 2021, small-cap companies were valued, and wasn’t that ultimately a golden age more for stock sellers than for pickers?

Of course, this can make it difficult for a good company to list during a bear market, when the pricing sentiment is at the level of the first. But why would a good small company want to seek money from a mini-Hesburger (mini-Hesulista) if the world is full of it, provided there’s something good to offer in return? Instead, the situation is apt to create pricing errors. Primarily upwards, but still with leverage downwards if something genuinely good strays into the notorious den of consortia, main owners, and professional talkers.

Shouldn’t it be an ideal environment for stock picking in terms of returns? Of course, the problem is that it highlights the difficulty of stock picking, and no consolation prizes are even awarded for participation. Or one could just buy a share in the global monopoly board’s Erottaja hotel and wait for the unsuccessful stock pickers to land on the square in turn. Then index investors and those successful stock pickers from previous decades always win. Pohjola’s first evokes emotions, and it’s hard to believe in the realization of indistinguishable profits on the horizon of small companies, but that’s what stock picking over the long term has always been about, whether it was about tulips, cars, or artificial intelligence. And just to clarify, we were talking about Pohjola’s first as an index here.

Edit. And yes, there’s always time to jump on board… just as there is to get off.

Exactly! Winter is a good time to make investments, as long as you are careful about what you stuff into your portfolio.

The sunshine has already started to hit the brush pile of large companies, so why shouldn’t smaller ones sometimes emerge from under the snow again? And you don’t have to pay a fortune for them, like in 2020–22.

Addition. I think I once pointed out years ago, during the IPO craze of 2020–21, that when the number of shares increases on the stock exchange, demand must also increase. Now, what has happened is that there has been an oversupply of shares, but demand for them has plummeted. Hence, prices down.

In this sense, the IPO craze, even if the party is fun at the time, is bearish for stocks.

I already promised/hoped for this news a couple of days ago here in the cafeteria. I did delete it so that no one would get upset and start flagging. Now we can surely talk about it as there’s a fact in the printed word.

I guess it “grows” now when fat in the abdominal area decreases.

Someone who’s already lean should sacrifice themselves for science and try if their penis grows with Ozempic, even when there wasn’t inches of extra fat at its base to begin with.

Who will sacrifice themselves to be the guinea pig?

Even strange things affect bodybuilding, I won’t comment on that. But for example, if a bodybuilder has a small head, it makes the shoulder line look wider, etc.

Kevin Levrone was indeed a very big guy, but he had such a narrow and small head, which he used to his advantage in poses:

Big Arska has indeed said that he started bodybuilding because before bodybuilding he looked strange naked when one part was disproportionately large compared to the rest of his body. He had to bulk up his body to be bigger.

One owner’s large ownership stake (60%) catches the eye, and without delving into the matter, I have experience with companies where one person’s ownership stake has been >50 percent, and they certainly didn’t end happily (SSH and Biohit) until the largest owner agreed to reduce their ownership. Taaleri Mikromarkka (now active in Proprius) was at least along for the ride until they realized it wouldn’t amount to anything and sold their stake. Without taking a stand on how this will turn out, just a shy note on the dangers of a large owner from the sidelines, with all friendship.

Without taking a stand on this particular case, it’s generally advisable to check with whom you own a company.

Owners appoint the board, and the board appoints the CEO. The board defines incentives for the CEO. The influence of the owners is more or less evident in all company operations.

If an investor were to buy half of a company with another person, it would surely be clear to many of us that we would investigate the know-how and motives of this other owner. But do we conduct such research in the stock market? I always glance at the owner list, but even that often remains superficial, as it usually takes years to truly understand the quality of the owners.

I must defend the Viafin thread, which I like very much, to the extent that it clearly shows the owners’ trust in the company and the lack of ambiguities, as there’s no need to constantly debate about the company; once a quarter, confirming the cash flow is enough. And for me, with Viafin, even reporting once a year would be enough. No need to hear updates every three months on how pipes have been cleaned.