It might not be worth inventing something like this oneself when there’s a ready product nearby, and there’s no need to specially manufacture vehicles for the Giraffe. Just put it on any flatbed. But why not for licensed manufacturing, for example. Saab reveals Giraffe 1X Compact Radar Module Saab reveals Giraffe 1X Compact Radar Module

According to Nordea, the conditions for economic growth have improved in Finland. Of course, there is no actual economic growth now, as it was just reported that GDP decreased in Q2. So let’s at least rejoice in the improved conditions for economic growth, even if actual economic growth is not yet visible.![]()

11 Likes

I consider First North to be a kind of dump; I don’t even try to look for potential investment targets there. There are enough large, real companies available globally.![]()

1 Like

Working at Inderes sometimes feels like a TV series, where each episode (workday or week) has a theme.

Today’s clear theme has been ownership and major shareholders, which I encountered in two ways.

In the morning, while walking to work, I listened to @Sauli_Vilen’s interview with Taaleri’s CMD. Familiar themes were present: Garantia, some fund was being grown again, and for a change, capital was being hoarded in the company. I talked to Sauli about Taaleri again after arriving at the office and glanced at the analyses. It’s quite clear that Taaleri trades on the stock exchange below the sum of its parts. The price-to-book value ratio is also one, which is strange when the return on capital is quite decent and the company’s historical track record in acquisitions has sometimes been good. But the clear problem is that no one really knows what the major shareholders want from Taaleri. The strategy bounces all over the place. The stock has been languishing for 10 years, and this doesn’t seem to be ringing any alarm bells in the company! ![]() This has always been the case during my time at Inderes and when I first got to know Taaleri more in 2016, and by all accounts, this will always be the case until an awakening occurs among the major shareholders.

This has always been the case during my time at Inderes and when I first got to know Taaleri more in 2016, and by all accounts, this will always be the case until an awakening occurs among the major shareholders.

Then I made a video with @Pauli_Lohi about Fodelia, because we thought the hidden gems Fodbar and Feelia were worth highlighting to investors. But here too, I considered the company’s historical track record in capital allocation. For the major shareholders, chips seemed to be a beloved industry, and sometimes Feelia’s excellent cash flow was thrown into kebab meat (which was an unsuccessful acquisition). Now Fodelia is focusing a bit (with Feelia and Fodbar as spearheads), but I wonder if more could be extracted from the company by streamlining and divesting Oikia’s chips. Fodelia has been languishing since its short listing history in 2019.

In the short term, companies’ stagnation can be blamed on CEOs or the economy. Then, if problems persist, the board. And if the stagnation continues for ten years, the owners can look in the mirror. Changing the CEO and board is still easy, but shaking up major shareholders is not. The interests of major shareholders can be divergent, such as building some kind of empire.

There would certainly be a demand for an activist investor on the Helsinki Stock Exchange.

66 Likes

IQM has raised €275M in new funding from US-based Ten Eleven, Tesi, and other investors ![]() :

:

18 Likes

Nordnet Customers Net-Bought Electric Bicycle Company Shares for 1.8 Million – Likely an Investment Scam

In Nordnet’s trading statistics, the third most net-bought foreign share was the small electric bicycle company Fly-e. Nordnet has blocked buy orders for the company’s shares in its service.

14 Likes

I could immediately quote here the message I wrote this morning in the Spinnova thread, since the topic is relevant. Let me add that it’s quite unlikely that this would be the case with Spinnova, but it’s good to discuss the topic otherwise.

9 Likes

The current bull run actually started already in October 2023. So almost 2 years ago. We’re soon going to be at ATH in Helsinki too.

12 Likes

In that message, I talked about Citycon’s stock. You can look at a graph of it over a suitable period, but it has declined in almost all timeframes. I myself just exited it with a small loss.

It occurred to me, how many of you are in a situation where your own role at work affects what kind of companies you invest in? Since I have quite a broad playing field under my responsibility, I inevitably get to know the services of many listed companies, and through this, I sometimes develop a strong understanding of their strengths and weaknesses. Then, when you come to the Inderes forum, you might read quite hopeful texts about the growth opportunities of some companies, and you just think to yourself, “Oh boy, if only you knew what’s happening in company X, Y, or Z” ![]() I know that insiders naturally think about this, as they have to limit the information they provide due to legislation, but what about when you are, say, a customer of company X and you know very well how bad things are, and at the same time you wonder how people are investing? I myself am in an industry that hasn’t been doing particularly well in recent years, and here too there are these eternal promises, described as turnaround companies. I always feel like giving my two cents in forum discussions, but some brake kicks in, wondering if it’s appropriate, etc.

I know that insiders naturally think about this, as they have to limit the information they provide due to legislation, but what about when you are, say, a customer of company X and you know very well how bad things are, and at the same time you wonder how people are investing? I myself am in an industry that hasn’t been doing particularly well in recent years, and here too there are these eternal promises, described as turnaround companies. I always feel like giving my two cents in forum discussions, but some brake kicks in, wondering if it’s appropriate, etc.

60 Likes

This is a forum where investors help investors. ![]()

53 Likes

I’ve really savored this message, even though its core message is a bit bitter. But it summarizes the public pressure of investing well. This is a field where it’s a top performance if you’re not completely wrong 49% of the time. Or you can even be completely wrong 90% of the time, but when you are rarely right, you make years of gains. Psychological pressure and the typical comparison to others can easily make one feel unwell during periods of underperformance. No wonder many well-known investors like Buffett communicate very rarely and almost never comment deeply on their investments.

40 Likes

48 Likes

Next lynching. Go check out what Proprius has gone and bought. Read the whole story to find out why I’m advertising here too.

https://forum.inderes.com/t/proprius-partnersin-rahastot/37976/255?u=_teemuhinkula

19 Likes

Anna, just keep coming! ![]() These kinds of tidbits, so-called from the field, can sometimes be the best content on a forum. As long as all parties in the discussion remember to be critical of sources and capable of independently assessing how relevant the information shared on the forum is to the business of the company in question

These kinds of tidbits, so-called from the field, can sometimes be the best content on a forum. As long as all parties in the discussion remember to be critical of sources and capable of independently assessing how relevant the information shared on the forum is to the business of the company in question ![]()

If I find out at work or in my free time that, for example, a discussion partner is an employee, customer, or otherwise interacts with an interesting small company, I start asking more about the company ![]() Rarely do you get any groundbreaking information for an investment case this way, but you can always learn something from discussions. Sometimes a customer might even badmouth a company and at the same time advise absolutely not to invest, but that has had no effect on the company’s and investment’s success, but rather the opposite

Rarely do you get any groundbreaking information for an investment case this way, but you can always learn something from discussions. Sometimes a customer might even badmouth a company and at the same time advise absolutely not to invest, but that has had no effect on the company’s and investment’s success, but rather the opposite ![]()

For example, regarding Relais’ subsidiary Raskone, I heard a lot of bad things and stories of failed repairs from several of the company’s customers when I inquired about experiences with the company when Relais announced acquisitions. Either Relais has managed to turn the customer experience completely around, or these were just isolated incidents that can sometimes happen in the country’s largest brand-independent commercial vehicle repair chain when a lot of repairs are being done ![]()

For example, it’s difficult to draw very big conclusions from such a small piece of information, as the sample size is very small on a group scale. In any case, Raskone has developed excellently under Relais’ wings, especially in terms of profitability, despite these customers tearing their hair out.

Also, when Puuilo was listed, several acquaintances complained to me about narrow and messy aisles and worn-out store furniture, shopping carts, etc. Well, the number of these messy stores was then roughly doubled, and at the same time, the best profitability in the retail sector in Finland was achieved, and as the CFO said, business went just as well, if not better, from a slightly rougher hall with affordable prices and a carefully considered selection aimed at DIY men and women ![]() Of course, the store concept is also fresher in newer locations nowadays.

Of course, the store concept is also fresher in newer locations nowadays.

And it can also go the other way, that it would indeed be worth listening to a customer who criticizes the company. My friend, for example, once trashed Kamux when the additional insurance purchased for the car didn’t cover some repair. It would have been worth listening and selling the shares in good time ![]() This happened during the peak of the share price in 2021. So, if you share information directly from the field on the forum, it’s worth considering how significant it is for the company’s business. If I remember correctly, there might even be a separate thread for sharing these lighter customer experiences I’ve mentioned. However, over time, truly valuable information directly from within the industry has been shared in many company threads, and I encourage anyone who has such information to do so!

This happened during the peak of the share price in 2021. So, if you share information directly from the field on the forum, it’s worth considering how significant it is for the company’s business. If I remember correctly, there might even be a separate thread for sharing these lighter customer experiences I’ve mentioned. However, over time, truly valuable information directly from within the industry has been shared in many company threads, and I encourage anyone who has such information to do so!

33 Likes

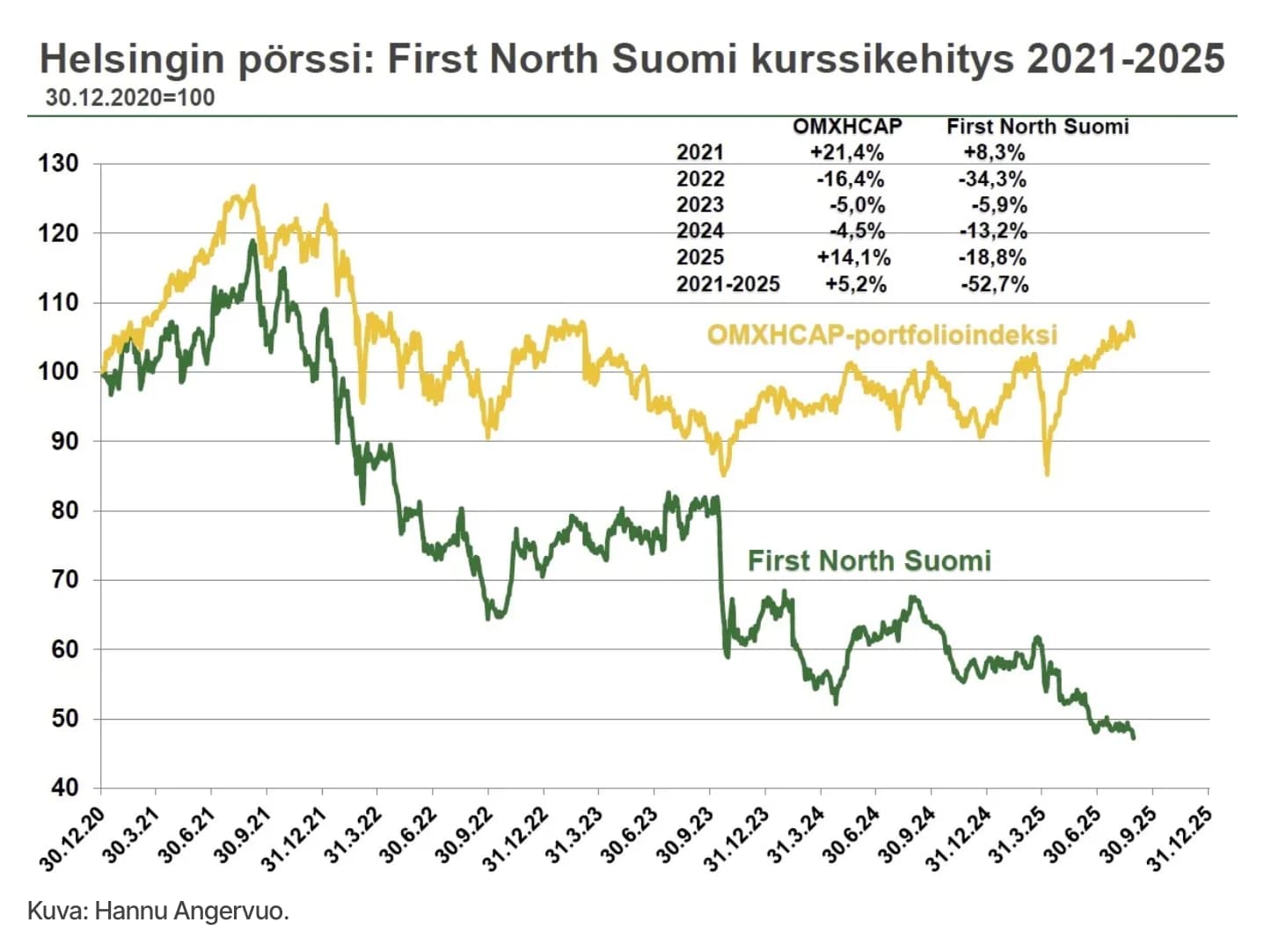

I, at least, view First North companies as part of the entire stock market, but as a list, it has been a bomb in recent years. ![]() ~60% down from its peaks. The OMXH Small cap index, i.e., small companies on the main list, is, however, “only” less than 40% down from its 2021 peaks. The OMXH Small cap has also recovered slightly from its lows.

~60% down from its peaks. The OMXH Small cap index, i.e., small companies on the main list, is, however, “only” less than 40% down from its 2021 peaks. The OMXH Small cap has also recovered slightly from its lows.

This probably explains the gloomy sentiment on the forum. If you look at Helsinki’s large companies, we are practically at an ATH (All-Time High) with dividends. Nordea, Finland’s most popular company to own, is at an ATH. The national stock Mandatum is almost at an ATH, etc. But there are a lot of small-cap focused pickers here.

On the other hand, among the larger and popular players, for example, Neste, Qt, and Tietoevry have crashed, and Nokia is going nowhere.

The good thing about that little-known index is that, compared to it, many portfolios have certainly outperformed in recent years. ![]()

27 Likes

Thanks for the long answer! This is a good justification for the fact that an individual’s knowledge of a company still represents an individual’s knowledge, and doesn’t necessarily provide essential background in a changing world where everything is constantly in motion. However, regarding tech/software companies, I can generally say that if, in my job role, I notice product development lagging and mandatory migrations or technology conversions are missing, then moving forward, the legacy will always hit a wall, and newer competitors accelerate their pace.

This topic is therefore a good indicator for an investor because a company’s dynamic is often one or the other. Either there’s a good product development culture or a good sales culture. Having both in a company is, in my experience, rare. Poor management may not understand that in a software-centric product company, the maintainability and development potential of the product are more decisive in the customer’s eyes. So, real money must be invested in this, not just empty promises. At worst, one sees that it is precisely the salespeople who jump from one software company to another when they themselves realize how the basic product cannot withstand competition, meaning it doesn’t benefit the salesperson either.

Well, my whole idea originally stemmed from the fact that at work/as a customer, one often encounters listed companies, and when one gets a good insight into their products, it changes the investment case, if one had such a case in mind for the company before. Perhaps in summary, one could say that if an investor gets in contact with customers of company X, Y, or Z, it is precisely those customers who can sometimes provide revealing information that can positively influence one’s thoughts. This is, of course, difficult to apply to something like Kamux, but it’s more effective in software companies when considering business customers.

10 Likes

Foreign holdings in Nordic early-stage companies are just rounding errors. Revenues are smaller than the salary costs of the teams screening them; the goal is to get

2 Likes

Lapwall is the first company that comes to my mind regarding this. My own experiences with that company are old, but they were particularly negative. In my opinion, it’s a rather risky company. Despite this, it is currently trading at multiples that, in my opinion, would require the vast housing stock built between 2016-2022 to be fully occupied, at least 1 successful data center project already completed, and certainty about a decrease in timber prices. According to Inderes’ forecasts, Lapwall’s EV/EBIT for 2025 is 23, and adjusted, 17.8. For comparison, Qt’s EV/EBIT is 18.3, and adjusted, 16.1. I personally consider Qt’s opportunities for profitable growth significantly higher than Lapwall’s. Both can, of course, succeed or fail, but I simply don’t understand Lapwall’s multiples.

6 Likes

In my opinion, there’s a somewhat similar phenomenon visible here as in the ongoing discussion of company chains vs. one’s own experiences with companies.

A company’s product, let alone its quality, does not necessarily determine a company’s stock market journey in any way if the industry is right or even slightly bubbled. More than quality issues, investors are interested in stories and future potentials, whereas within the company (excluding management team work) often only the delivery phase of already completed deals or, at most, the sales pipeline is visible. The potential of product development, on the other hand, cannot really be sensed from within the company. Then, when these are told by someone else, we cannot be sure of their position in the company, their perspective, what is opinion and what is fact…

Even if one wanted to draw conclusions from these ‘tea leaves’ to support investment decisions, in my opinion, they are not really suitable for that. Nowadays, in the golden age of investment scams, one should in any case approach all sorts of online narratives, if not with hostility, then at least with healthy skepticism.

10 Likes