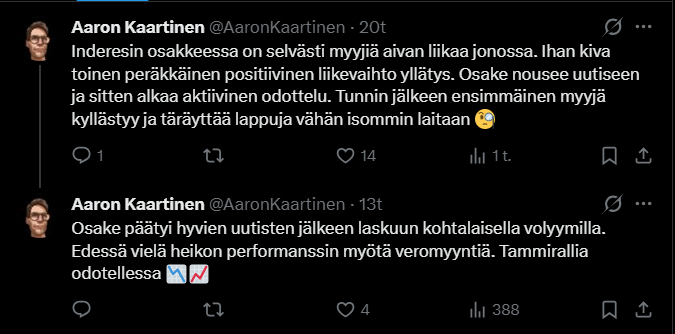

Hello,

Even though I’m not filling in for Mikael here, since I’ve been responsible for the majority of company monitoring agreements concluded before 2024, I’m certainly the right person to answer this ![]()

I dug up some data. Between 2018 and 2025, 69 companies have listed in Helsinki and on FN (this doesn’t account for list transfers, but genuine new companies including spin-offs). Of these, 7 have never been under our monitoring, and 62 have at least been under monitoring (a couple went bankrupt, for one, monitoring never even started despite a contract, one was acquired, another terminated the agreement, etc.).

I calculated data for this period, and on average, listed companies have come under our monitoring approximately 7 months after listing. The spread is, of course, very wide. 27 companies have been taken under monitoring immediately, and in these cases, we were either involved in the IPO or monitoring was initiated as soon as the listing began. Conversely, the longest sales cycle has been 1792 days, just under 5 years (this honor goes to BBS ![]() ). If we exclude cases where monitoring was initiated immediately (i.e., we had a contract signed before the IPO), the average rises to over 12 months. So, if monitoring doesn’t start immediately at the IPO or right after, it takes on average over 12 months for a company to come under monitoring. The median is, of course, somewhat lower, as those individual 3-5 year lags raise the average for everyone.

). If we exclude cases where monitoring was initiated immediately (i.e., we had a contract signed before the IPO), the average rises to over 12 months. So, if monitoring doesn’t start immediately at the IPO or right after, it takes on average over 12 months for a company to come under monitoring. The median is, of course, somewhat lower, as those individual 3-5 year lags raise the average for everyone. ![]()

If you look at which companies we are typically involved with right from the start of listing, they are usually smaller companies. This is because smaller companies usually come through smaller advisors (Evli, EY, Sisu, Alexander, UB, etc.), and these advisors typically don’t have their own analysis operations. Therefore, they are often interested in including us in the analysis or at least ensuring that someone starts monitoring the company quickly. In large IPOs, on the other hand, the organizers are brokerage firms (Nordea, Carnegie, SEB, etc.) that have their own analysis operations. They rarely need/want us involved because their own analysis operations handle these. In these cases, we typically don’t discuss company monitoring with the company before the listing, as the company has its hands full with the IPO and its focus is there. We usually start negotiations after the IPO.

Without going into specific company matters, as you can see from the 2025 listings (GRK, Posti, Nokian Panimo, Cityvarasto, and Framery), 4x were brought by large players, and only Nokian Panimo is smaller. It’s worth noting here that Evli was the lead organizer, and Evli also performed the IPO analysis. If I recall correctly, in all Evli IPOs during this period, Evli also initiated company monitoring. For clarity, I also state that we have been alongside Evli in several of their cases doing IPO analysis (e.g., Relais). ![]()

Then, a response to the sharp observation regarding Mifid2. We have not seen any change. The problem remains that trading in smaller companies does not sustain anyone, so earnings must come from elsewhere. In addition, commissioned analysis has become part of all players’ offerings in the Mifid2 era, and this is a significantly better way to finance the analysis of smaller companies.