How did the 2024 public offering go?

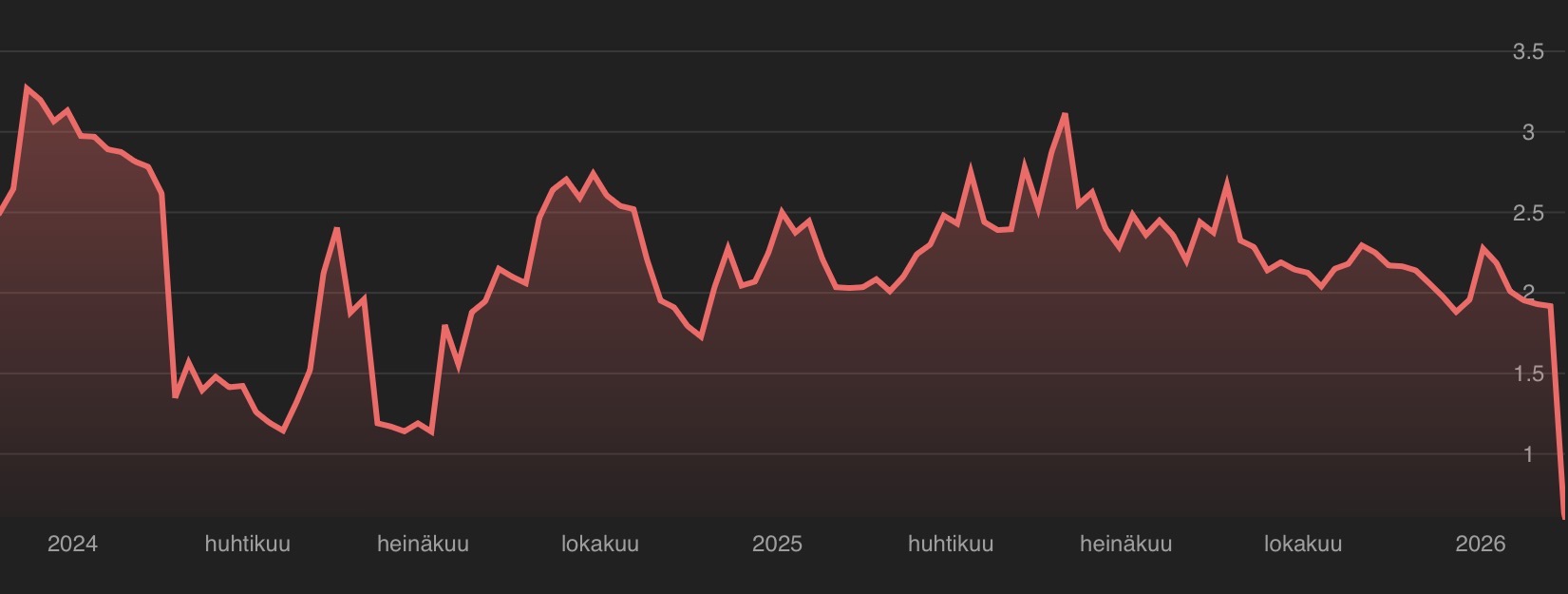

A major financial hiccup was announced in February. The share price dropped from just under 3 euros to nearly one. The CEO and CFO were replaced. Bridge financing was secured. A savings program was initiated. On April 4th, the company announced it needed a total of 27 MEUR to get in front of the FDA with BEXMAB. The price rose to approx. 2.5 euros in May. On June 4th, a 30 MEUR public offering was announced at one euro per share, 30 million shares. The price fell back to near one euro. It wallowed at the bottom for a month. The offering succeeded, and in September, the price was back near 3 euros. It took half a year for the value to recover to pre-hiccup levels from the time the financial difficulty was announced. It took 5 months from the announcement of the need for funds through a share issue. 3 months from the issue itself. Mcap rose significantly higher, as the number of shares increased from 70 → 100 M. Thus, it was quite difficult to “lose money” by force without selling low during that offering, or could you tell us how, @mestaripancho?

Past performance is no guarantee of future results.

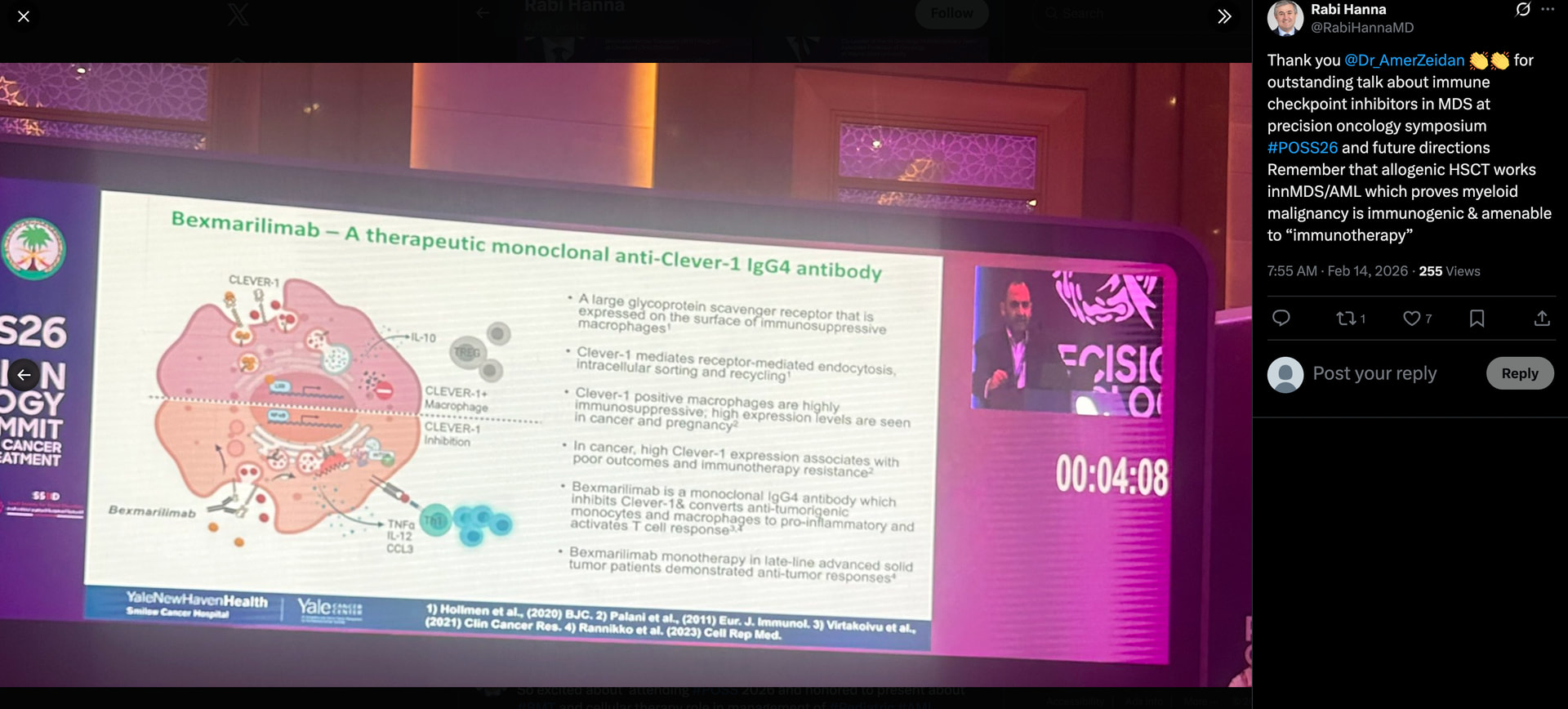

Back then in 2024, only BEXMAB Phase 1 (a “basket study” investigating safety and preliminary efficacy in several cancer types) had been completed, yielding important information: it’s not worth putting money into a larger trial for r/r AML; instead, move towards r/r MDS, where there is market need and room. Funds weren’t sufficient to expand into first-line, and fortunately, we only proceeded with a single patient in first-line aza+vene+Bex AML, given what we now know about vene’s toxicity, the need for dose adjustments, and the issues with low-blast count patients.

Furthermore, there was only preliminary evidence from Phase 2 back then. The FDA’s stance tightened regarding Accelerated Approvals (AA) at the same time when those who received AA licenses failed to complete Phase 3. Faron cannot be blamed for that policy change.

It is a strange thought in itself that if we want a partner to pay for Phase 3, the partner wouldn’t need to know what they are paying for and what they are committing to? Just standing idly by while burning administrative costs? This time it went well, as we heard in advance from experts about the recent landmine here for Faron and the partner. And we are trying to avoid it. Now top units and their doctors are on our side; they want access to Bex through trials (e.g., IIT r/r MDS USA). It will be interesting to see how the r/r MDS trial is designed—perhaps just additional recruitment for the single-arm study. A year ago, Zeidan “suggested” from his experience that at least 40 patients should be gathered with OS over a year to potentially get an AA. Whether that holds with current policy, they are likely better informed than us.

At the time of that previous offering, there was no information that we could proceed to Phase 2b and 3 in first-line HR-MDS (the planning changed even now) let alone the investigator-initiated trials (IIT) in r/r MDS, AML, melanoma+lung, sarcoma, and breast cancer. So now we are already closer to the finish line, meaning one could at least assume the company is more valuable than a couple of years ago, but “Viren” must get up—otherwise, we won’t reach the finish line, at least not in first place.