Facts are being thoroughly mixed up here, perhaps partly on purpose?

When the Verona results were published last year, even the experts on this forum said that public Phase 3 (P3) data is rarely available, especially regarding this high-risk MDS case. They only became public at ASH in December 2025.

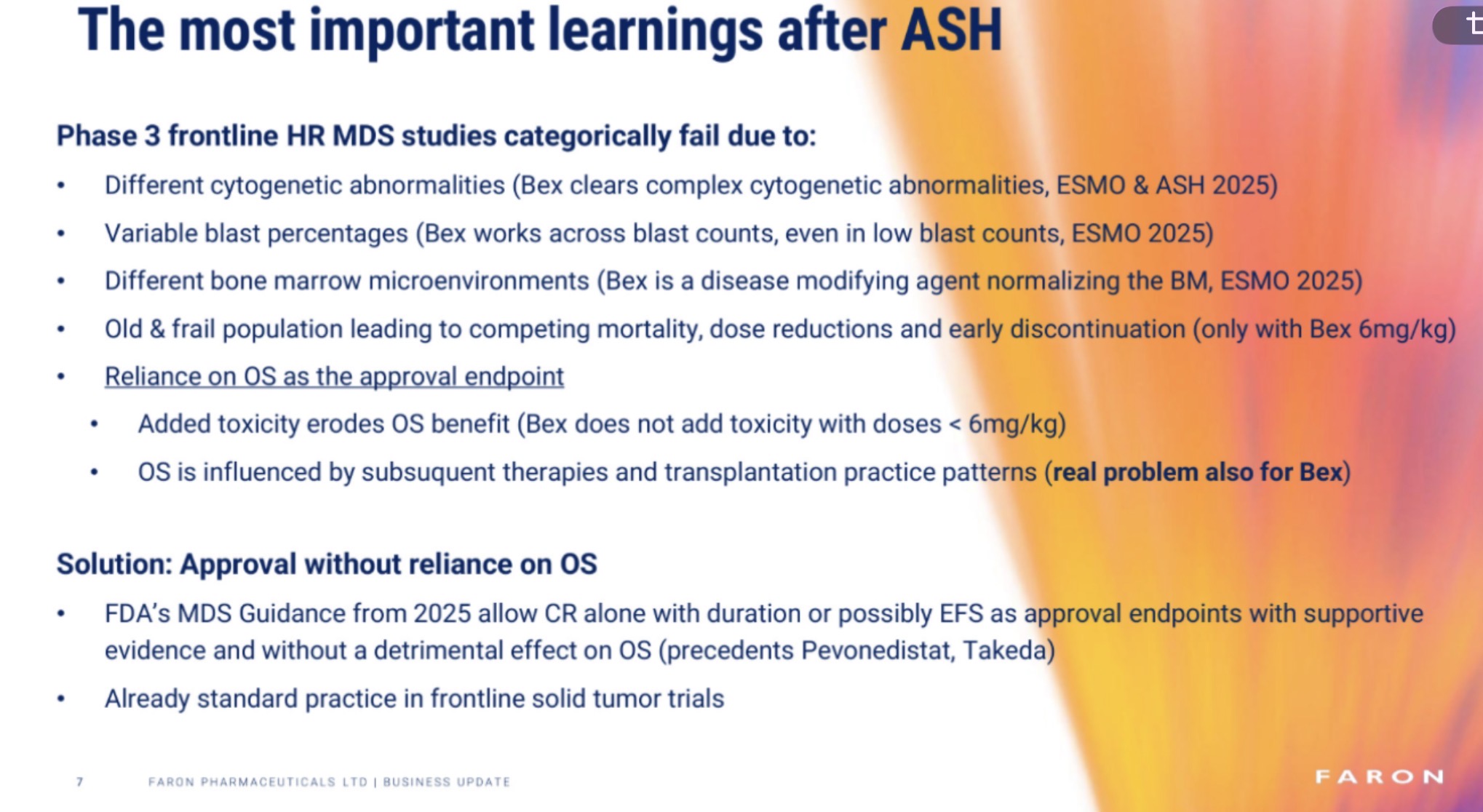

Venetoclax (Vene) had OS as an endpoint, which was the only option according to FDA guidelines until last autumn. It’s useless to blame Faron’s expertise for choosing OS as the endpoint in early 2025. Besides, Faron itself has been pushing for cCR and CR endpoints all along.

In practice, there have been two (2) months to react with a new plan on how to move this study forward for r/r MDS patients. In that regard, everything looks good now; CR endpoint approval is not the issue, but rather the new FDA recommendation.

However, one should look at the big picture; this MDS TP53 etc. is just one small tree in the whole forest. Faron won’t collapse even if the offering doesn’t bring in a penny. They can put Bex for MDS on ice and wait for investigator-initiated trials if they so choose. Is it sensible? Well, no, because patents eventually expire and Big Pharma (BP) knows this too; also, a blinded study for Bex is needed to get more scientific data from a slightly larger population.

The point is, the MDS market is just a way for Faron to access larger markets found in solid tumors, etc. Someone skilled could make a nice diagram of the market Faron is currently targeting.

Based on the same logic, Big Pharma will not make offers. Novartis won’t do it; they want to maintain good relations because the science itself and the large business case haven’t disappeared. On the contrary, progress has been made all the time.

One could of course ask, if everything looks good in the plans now, why not partner on the same terms as intended in the autumn? Good question, but if 40 million is raised from the offering for a new study that Faron is capable of doing, then from the shareholders’ perspective, it would just be foolish to give away value to others when, even after dilution, the value on 11/27 could be many times higher. With the emphasis on “could,” of course, assuming the results are good. No one denies the risk.

As Faron continues to advance its frontline development plan and addressing the FDA’s remaining question on contribution of each agent testing bexmarilimab + azacitidine against placebo + azacitidine, investigators from the BEXMAB Phase I/II trial believe that the benefit of bexmarilimab in r/r MDS is clear given the data produced to date in the BEXMAB trial. Hence, led by City of Hope (USA) an investigator-initiated trial (IIT) in r/r MDS is also planned to commence in 2026 to produce more data in the last line setting while Faron pursues the frontline setting. This IIT data in r/r MDS is planned to be used for further validation of the benefit of bexmarilimab in last line HR MDS and support the discussion by Faron of potential accelerated approval in r/r MDS with the FDA at the time of the frontline Phase II read out.

Faron also plans to support up to five investigator-initiated trials to further validate bexmarilimab’s potential in combination trials in melanoma, lung cancer (NSCLC), soft tissue sarcoma, breast cancer (ER+ BRC) and leukemia (AML). The Company believes that these additional trials can further strengthen and expand the potential of bexmarilimab in solid tumors, which it expects to increase bexmarilimab’s attractiveness for a potential commercial partnership with biopharmaceutical companies on a global basis.