I agree that big things will happen during February or in early March. Significant moves regarding strategy or corporate restructuring could likely be made within this timeframe. By mid-March at the latest, the notice for the Annual General Meeting will be issued – I wonder what interesting and out-of-the-ordinary items might be on its agenda? It’s clear, of course, that at the very least the Board will be authorized to issue X million shares – for our acute needs…

2 Likes

The pipeline is progressing, of course, as the days go by. The future and new opportunities have been depicted on slides, but the funding for all of it is indeed still missing. Based on previous financing arrangements, I’ve gotten the impression that the company is willing to drive right to the edge—even if it means going over—with new financing solutions. Consequently, it’s a very realistic possibility, in my opinion, that we’ll next hear about financing when the cash is practically gone.

3 Likes

Currently, cash is being preserved by diluting shareholdings through an increase in the number of shares while repaying debt with additional shares.

Before the March general meeting, Faron aims to maximize its negotiating position by publishing expanded data (such as the BEXAR and BLAZE study updates in solid tumors at the end of January). The goal is to create “competitive tension” toward Big Pharma and demonstrate that bexmarilimab is Phase 3-ready. At this stage, the company needs either a letter of intent (LOI) or concrete signs of an upfront payment to be able to present something other than a survival model to the general meeting.

The general meeting on March 30, 2026, acts as a deadline where the company’s board must obtain new, broad authorizations for share issues and potentially for drawing the third debt tranche if a partnership agreement has not yet been signed. A hypothesis could be that authorizations are sought at the general meeting to enable either a large directed issue (institutions) or the finalization of a partnership deal.

The meeting is, at least for me as an investor, a kind of crossroads: it will be either the formalization of a rescue operation or a major moment of celebration accompanied by a newly announced mega-deal.

I suppose one could create an infinite number of hypotheses?

7 Likes

I wouldn’t count this as your mistake; rather, I think this falls on Faron’s reporting. Shareholdings are public information, and everyone can check them from Euroclear practically in real-time. However, Faron does not display this ownership information as is on its own website, and I ask for the umpteenth time: Why not?

There is no mention of Karvonen’s affiliations and controlled entities on the company’s website, but he is reported to own 104,000 shares:

Neither Faron nor anyone else can expect that someone would go looking for this information in the 2024 offering prospectus. For example, in Karvonen’s case, an easy solution would be to show that company as an owner and, in the additional information—or at least in the information detailing management holdings—state that it is Karvonen’s controlled entity.

The actual state of Syrjälä’s, and indeed everyone else’s holdings, seems questionable when Faron modifies them from Euroclear’s official data according to its own criteria.

7 Likes

You lumped all sorts of things together earlier, neatly turning rumors into facts regarding, for example, Karvonen’s “sales” and Faron’s breach of disclosure obligations. Now you’re blaming Faron’s communication for the fact that the bottom fell out of your rumor-mongering. That deflection is quite Trumpian, indeed. Perhaps you could focus more on fact-checking instead of just churning out others’ “findings” as half-truths—if, that is, you want to be making these kinds of summaries at all…

16 Likes

Everyone can draw their own conclusions. @Donkey said they had checked the holdings from Euroclear and Karvonen’s name was not found there, so their “hearsay” proved to be a fact following Karvonen’s statement. Thus, Karvonen’s name is still not found in the shareholder register, as he does not own the shares.

Faron, Karvonen, or anyone else cannot expect anyone to read the 2024 share issue prospectus to verify the matter, as I already stated above. Faron could easily fix this if they wanted to, by reporting the holdings exactly as they appear in Euroclear.

2 Likes

You are right. There wouldn’t be anything unclear about this if care was taken to ensure that the information is up to date and in an understandable format.

I’m mostly kicking myself because checking the unclear situation of just one person would not have been a difficult task.

2 Likes

Yeah, you spoke about sales (hearsay - not fact), not holdings. And you claimed that the sales haven’t been reported (your own interpretation - not fact). Well, enough of this.

13 Likes

Once again, several messages have been posted to this thread that hold practically no value from the perspective of investing in Faron. And here’s one more of those.

Regarding this discussion about Karvonen’s ownership, perhaps Faron’s website could include a clarification under management holdings that the ownership also includes controlled entities. As for whether the absence of such a clarification has any significance, I don’t think so.

16 Likes

“Cornerstone of next-generation multi-indication immunotherapy"

No more beating around the bush; it’s being said directly to Big Pharma → If you want to break treatment resistance to PD-1, targeted therapies, or chemotherapy – this isn’t just one combination among others, but the foundation upon which other treatments can work.

62 Likes

When could the first results from the BLAZE trial be expected? The announcement of the start was made on 22.12.2025.

3 Likes

It’s good that medical research results are being published as peer-reviewed articles. Reading the article with my limited expertise in pharmacology and medicine, it seemed to me that it mainly covers and highlights the same things that Faron has already presented several times in conference presentations and posters. Or do the medical experts on this forum find any substantially new points or insights regarding bex in this article?

3 Likes

My take on that publication is that, for the first time, it’s stated in black and white that Clever is the primary gatekeeper that must be targeted in all cases. This means that treatments and drugs are not of equal value, and for things to work ideally, a drug like Bex should be involved. Of course, this has been clear to us on the forum, but professionals and BP (Big Pharma) want hard facts, which is exactly what we have here now.

8 Likes

It is a good publication, but considering Maija’s affiliations and the timing, what comes to mind, unfortunately, is a carefully timed campaign book – if you know what I mean. Let’s hope the market interprets this solely on a scientific basis – all support is worth its weight in gold right now.

5 Likes

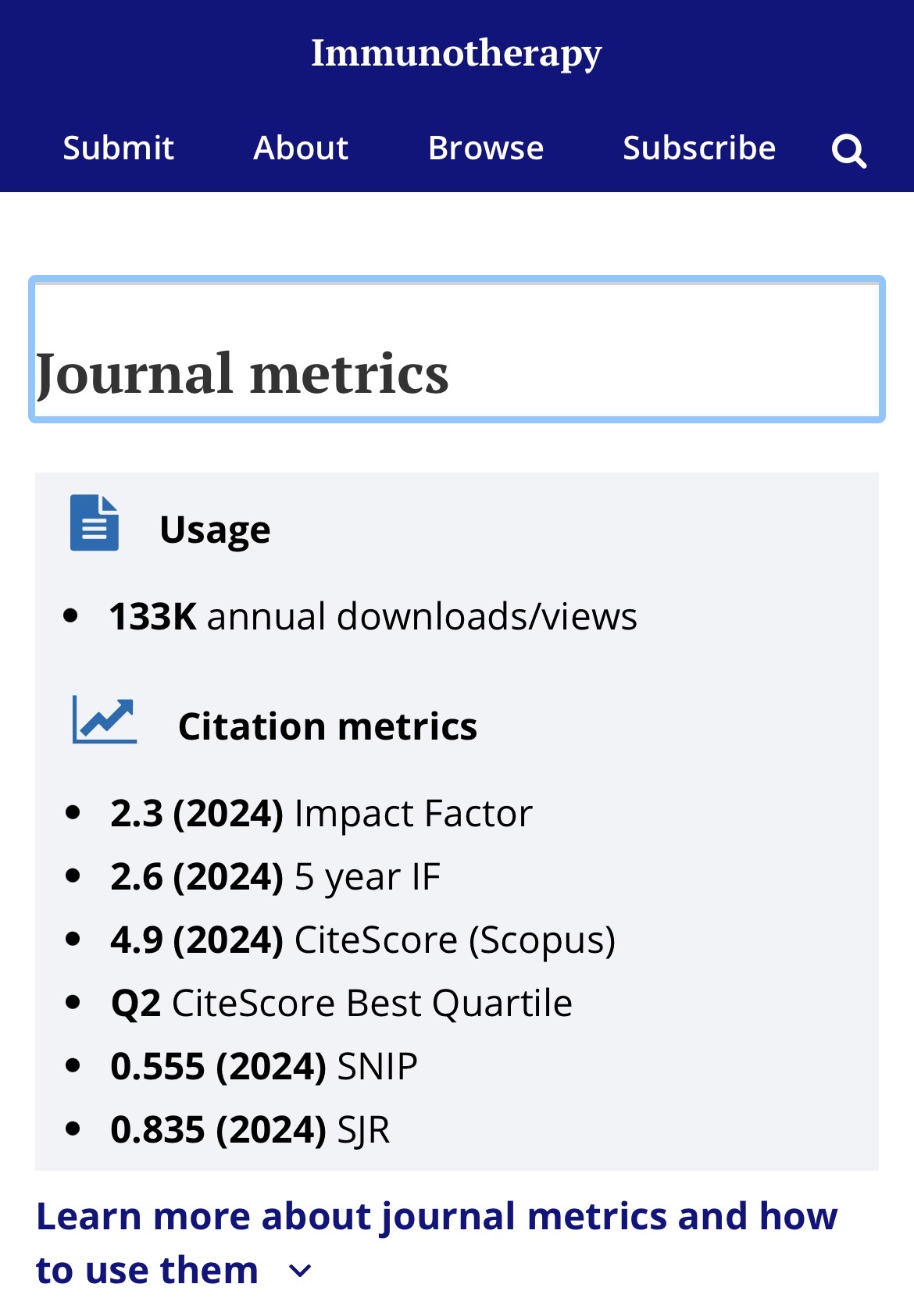

Faron Pharmaceuticals Ltd. (AIM: FARN, First North: FARON), a clinical-stage biopharmaceutical company focused on treating cancers through novel immunotherapies, today announces the publication of a comprehensive review article in the prestigious peer-reviewed journal Immunotherapy.

Even if the article didn’t necessarily bring much new information to the forum members, Maija’s research is now accepted by the scientific community, i.e., peer-reviewed. Regarding the significance of this and how prestigious the Immunotherapy journal is, **Vino_Pino**Mestari or someone else with a better understanding of the matter could provide their own perspective. Personally, I see this as a significant step forward.

15 Likes

I’m not familiar with that journal directly, but the Impact Factor is quite low at 2.3

Below the middle tier among medical journals, but not a “trash” journal.

4 Likes

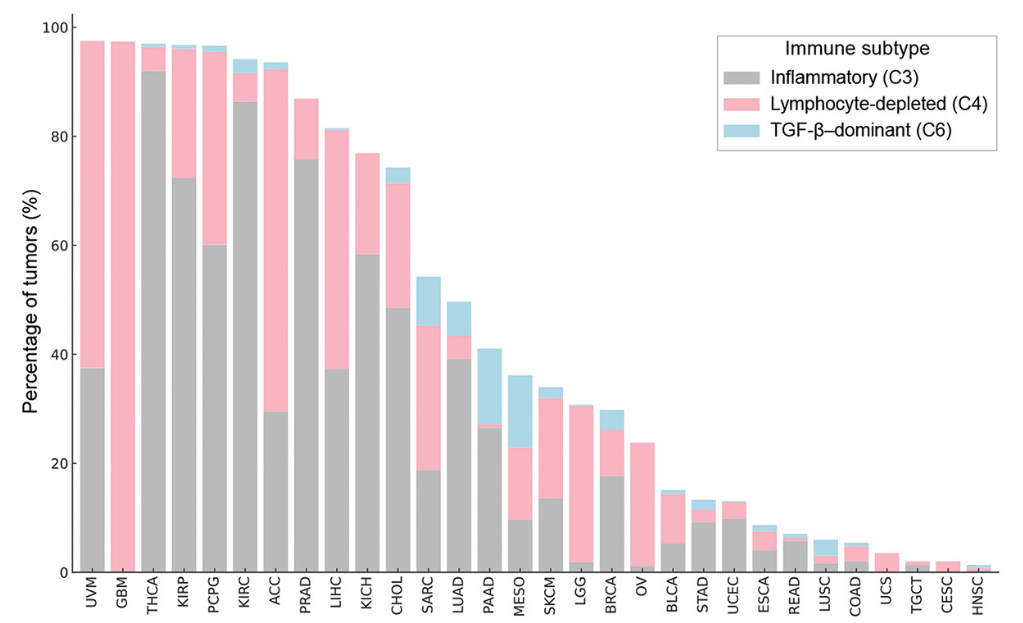

This is a review article. Review articles usually do not publish new data; instead, they review and synthesize information from previously published articles. I haven’t read the whole thing yet, but I skimmed through it. This article provides background on the biology of Clever-1 and the rationale for Bexmarilimab combination therapies. Additionally, it presents, among other things, Clever-1 expression in different cancer types and the immunological state of tumors (in Figure 3 below). This is very relevant information for assessing Bex’s target market in solid tumors and is likely an important topic in partnership negotiations.

For example, based on this diagram, one can already get a much better assessment of the cancers that would most likely benefit from Bex treatment. C4 (red) is a potentially Bex-benefiting immune subtype, as it is a lymphocyte-depleted tumor environment, and previous Matins and Bexmab trials have shown Bex treatment leading to T-cell accumulation in the tumor after treatment. C3, on the other hand, could be tricky if that inflammatory environment is associated with high IFN-gamma levels, which causes the tumor macrophages to not react to Bex in the desired way. Furthermore, the targeted cancers must inherently be Clever-1 positive, meaning the cancers found on the right side of the table are unlikely to be good candidates for Bex treatments.

edit: abbreviations for the cancers in the image

UVM (uveal melanoma)

GBM (glioblastoma multiforme)

THCA (thyroid carcinoma)

KIRP (kidney renal papillary cell carcinoma)

PCPG (pheochromocytoma and paraganglioma)

KIRC (kidney renal clear cell carcinoma)

ACC (adrenocortical carcinoma)

PRAD (prostate adenocarcinoma)

LIHC (liver hepatocellular carcinoma)

KICH (kidney chromophobe)

CHOL (cholangiocarcinoma)

SARC (sarcoma)

LUAD (lung adenocarcinoma)

PAAD (pancreatic adenocarcinoma)

MESO (mesothelioma)

SKCM (skin cutaneous melanoma)

LGG (brain lower grade glioma)

BRCA (breast invasive carcinoma)

OV (ovarian serous cystadenocarcinoma)

BLCA (bladder urothelial carcinoma)

STAD (stomach adenocarcinoma)

UCEC (uterine corpus endometrial carcinoma)

ESCA (esophageal carcinoma)

READ (rectum adenocarcinoma)

LUSC (lung squamous cell carcinoma)

COAD (colon adenocarcinoma)

UCS (uterine carcinosarcoma)

TGCT (testicular germ cell tumors)

CESC (cervical squamous cell carcinoma and endocervical adenocarcinoma)

HNSC (head and neck squamous cell carcinoma)

43 Likes

GBM, for example (quote: “Glioblastoma (GBM) is a highly aggressive, fast-growing cancer of the brain’s supporting tissue (grade IV astrocytoma). It is the most common adult brain tumor, occurring frequently in those aged 45–70. There is no cure for the disease, but surgery, radiation therapy, and chemotherapy are used as treatments to alleviate symptoms and slow growth.”) is a likely beneficiary. So yes, the market opportunities for BEX are immense.

14 Likes

On the other hand, glioblastoma is a cancer located in the central nervous system, and the CNS immune defense functions in a completely different way than in the rest of the body. In the central nervous system, microglial cells are responsible for the immune defense, meaning that the lymphocyte-depleted environment is likely due purely to the biology of the central nervous system. Therefore, it is entirely possible that Bex may not be applicable for the treatment of glioblastoma or other CNS cancers.

15 Likes

Jerej, could you please list the cancers from the image in descending order in Finnish for which Bex could work in that framework?

6 Likes