Duell has not opened these much itself. Acquired targets go into a black box and only consolidated figures are reported.

Some active individuals have dug into country-specific financial statements and other public sources

At least I have the impression that TranAm is a perfectly good business. It was just bought in a hot market where the figures were a bit too good, and too high multiples were paid for them. In hindsight, it can be stated that it would not have been worth buying in a hot market.

Duell’s market value is ridiculously low IF goods circulate without any massive discount campaigns and French operations can be made to run normally.

However, there are possibilities that the inventory value is overstated, or it must be sold at a discount = either the goods do not circulate and rot in the warehouse, tying up capital, or they are sold at a loss. French operations and other fumbling with brands can anger customers, leading to lost sales or partnerships. If there are setbacks in the business, financing can quickly become critical, and a share issue or similar may be necessary as covenants are breached.

No matter what happens, in a year or two, it will be easy to boast, ‘I told you so.’

“Duell’s equity ratio on August 31, 2025, was 55.1% (55.0%)”

“Duell’s net debt on August 31, 2025, was 20.2 million euros (19.6 million euros). Duell’s net debt on August 31, 2025, relative to adjusted EBITDA for the past 12 months was 3.3x (2.8x). The covenant terms were not met at the end of the reporting period.”

The balance sheet would be quite OK if only EBITDA were at least at a satisfactory level.

Duell’s market value is now 16 MEUR.

Revenue just under 130 MEUR.

It is not realistic to expect margins to rise particularly high, but even with quite small profitabilities, a significant amount of net income and cash flow could be generated relative to market value. For example, in Inderes’ forecasts for 2029, EPS(adj) = €0.82 if EBITDA% = 5.2

It’s not worth looking as far as 2029 yet, but it illustrates how low the EBITDA margin is for the company’s valuation PE(adj)<4

IF the business were to do even reasonably well, the stock is cheap as dirt.

In light of that, I have wondered about this:

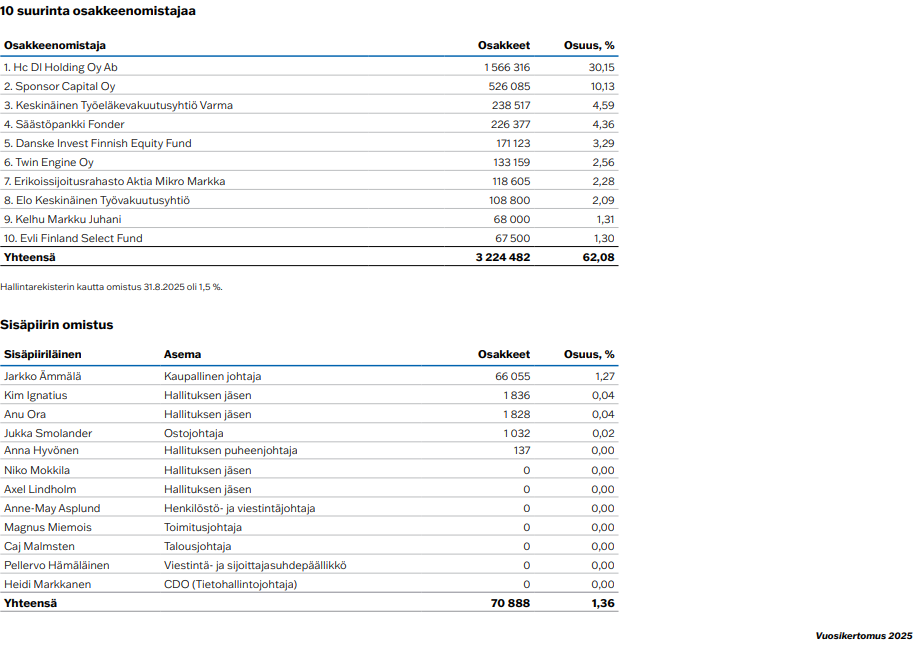

After 2023, insiders have only bought a couple of shares:

Since Duell has two main owners, it seems unlikely that a takeover bid is coming.

The value of the ownership stake of parties other than the Hartwalls is \~10 MEUR. With a 50% premium, the Hartwalls could try to buy the entire company off the stock exchange by paying 15 MEUR.