Luoja varjele tästäkin 10 milliä ja Tran Amista 14milliä. Nyt koko firman market cap 21milliä.

Paljon paljon muutakin on ostettu.

Luoja varjele tästäkin 10 milliä ja Tran Amista 14milliä. Nyt koko firman market cap 21milliä.

Paljon paljon muutakin on ostettu.

Tässä on Petrin kommentit Duellin Pohjoismaiden logistiikkapuolen tehostamistoiminnasta. ![]()

Järjestely on osa yhtiön tehostamisohjelmaa, ja sen tavoitteena on saavuttaa noin 0,5 MEUR:n vuotuiset säästöt. Säästöt tukevat ennusteitamme yhtiön tulosparannuksesta, mutta eivät aiheuta välittömiä muutospaineita ennusteisiimme.

Liikevaihdollisesti heikko elokuu Suomessa Duellin segmentillä. Volyymin osalta koko Duellin Q4 meni lopulta käytännön tasoissa viime vuoteen verrattuna. Kesäkuun hyvät lukemat varmaan johtuivat surkeasta toukokuusta joka siirsi myyntiä kesäkuulle. Tämän aamuisessa datassa myös kesäkuun ja heinäkuun lukuja korjattiin alaspäin.

Euroopan luvuista ei ole tarkkaa tietoa, mutta käsittääkseni varsinkin Ranskassa on aika synkkä kuluttaja tällä hetkellä eikä muuallakaan olla viime vuoteen nähden kovin reippaaseen kulutukseen yllytty. Markkinaympäristö todennäköisesti ollut siis edelleen Duellin huonohko. Joskin Suomessa tuo Q3 oli vielä synkempää.

No kuluttajaluottamukset isommilla markkinoilla Suomessa ja Ruotsissa ovat sentään viime aikoina olleet vahvistumassa, niin ei ihan puhtaaseen synkistelyyn vaivuta tämänkään viestin osalta.

Sebiltä tuoretta raporttia Q4:n alla:

Viilasivat käyvän arvon haarukkaa alaspäin:

Fair value for the equity at EUR 4.0-4.6 per share (previously EUR 4.1-4.9) We set our fair equity value range at EUR 4.0-4.6 per share based on DCF and peer group valuation. Duell is operating below its historical profitability levels, and short-term risks are elevated given the weak trend and stretched leverage.

Odottavat Q4:lla vain 0,4milj€ EBITAa. Itse toivoisin Duellin ylittävän analyytikoiden odotukset sen perusteella, että tuo surkea kevät antoi vähän liiankin synkeät suuntaviivat kesän myynnille ja kelien parantuessa trendikin olisi ollut parempi. Lisäksi surkealle Q2:lla lainattiin jo inasen bisnestä Q3:lta eli Q3 oli kaikin puolin surkea ja Q4 ei olisi aivan niin surkea verrattuna viime vuoteen (oik. EBITA 1,5milj€). No, pari viikkoa ja sitten kuullaan tuloksesta ja tärkeästä tasetilanteesta.

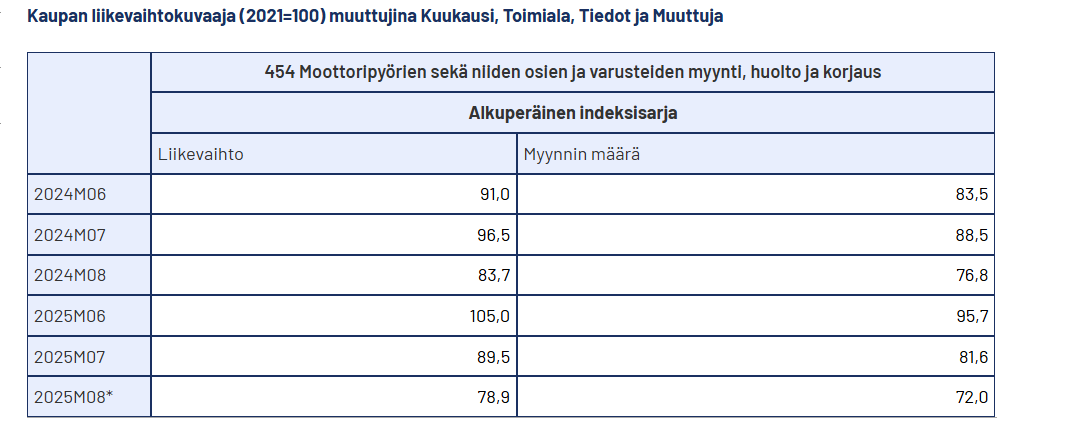

SEBin tuoreen raportin ja Tilastokeskusken tilastojen pohjalta intouduin taas vaihteeksi vähän pyörittelemään lukuja. En vaan ymmärrä aivan analyytikoiden ennusteita.

Duellin Q3:lla moottoripyörien sekä niiden osien ja varusteiden myynti, huolto ja korjaus (liikevaihto) tippui Suomessa Tilastokeskuksen mukaan 3,3% ja Duellin Pohjoismaat tippui noin 4% Nyt Q4 sama tilasto on jopa pienellä plussalla, niin silti Duellin pohjoismaiden liikevaihdon oletetaan laskeneen Inderesin ennusteissa noin 7% (SEBillä jopa 11%). Käsittääkseni Ruotsissa markkina olisi ollut vielä hitusen parempi. Toki Duellilla on muitakin tuotekategorioita.

Vaikka kannattavuutta puolustetaankin nyt kovenanttien vuoksi, niin odotan kyllä liikevaihdon osalta analyytikoiden ennusteita ylittäviä lukuja. Kannattavuuden osaltakin voi olla mahdollisuuksia parempaan, jos paremmat kelit on ohjanneet kuluttajaa Duellin kannalta kannattavampiin kanaviin toukokuun jälkeen (pienemmät korjaamot/myymälät verkkokaupan sijaan).

Inderes odottaa liikevaihdon laskevan Q4 4,5% (SEB vielä enemmän) ja koska kruunu on vahvistunut niin neutraaleilla valuuttakurseilla lasku olisi ollut silloin vieläkin isompi. Ohjeistus taas sallii liikevaihdon osalta jopa ihan pienen kasvunkin Q4:lla.

Muu Eurooppa onkin sitten enemmän itselleni kysymysmerkki ja varsinkin Ranska on todennäköisesti ollut vaisu.

”Pelko vie pimeän puolelle” sanoi muuan Mestari Yoda kaukaisessa galaxissa. Omakin usko vahva, että heikoilla keleillä moottoripyörän ollessa varastossa on kustannustehokas verkkokauppa helposti yliedustettuna — mikä toki varmaan heijastui kahden suuren Eurooppalaisen verkkokauppayhtiön +20% kasvulukuihin. Myynnin ajoittuminen arvoketjussa on toki vaikea ennustettava ulkopuolelta (milloin maalis/huhtikuun ennakkotilaukset on kulutettu loppuun ja onko jälleenmyyjillä ollut uskallusta täyttää varastoja loppukesää kohti). Q3 näki heikoimman bruttomarginaalin koko Duellin pörssihistoriassa, mutta silti analyytikot ennustavat vielä heikompaa marginaalia Q4:lle. Toki kausiluonteisuus antaa tälle historialliset perusteet (loppukauden alennusmyynnit), mutta hyvinkin näen mahdolliset perusteet parantuneelle/stabiilille bruttomarginaalikehitykselle.

Edit. On ollut erittäin pieni vaihto osakkeella, markkina odottavalla kannalla kohti tulosta 2vk päästä.

Sysimusta on arvostus. Idereskin luovuttanut kun satasen päältä suositteli ostamaan ja koko matkan alas osta. Voitollinen firma, jännä ettei mitään ennakkoa että markkina kääntyy. Nyt monessa osakkeessa mikä tappiolla niin huima arvostus.

Eikös kovenanttejen rikkoutuminen pidä ilmoittaa heti jos näin tapahtunut? Tulos ja tilanne kyllä nyt tiedossa.

Ei tarvitse ilmoittaa. Tulos ja tilanne on kyllä yhtiöllä jo tiedossa.

Jos tuollainen SEBin ennustama vaatimaton 0,4milj€ oikaistua EBITAa olisi tulossa Q4, niin silloin koko vuodelta olisi kasassa vain 4,3milj€. Silloin ohjeistuksen “oikaistun EBITAn odotetaan jäävän viime vuoden tasosta” on kyllä lievä ilmaus kun vertailukauden EBITA oli 6,2milj€. En tiedä Duellin sanallisen ohjeistuksen käytäntöjä, mutta kyllä kai osa yhtiöistä tuossa tilanteessa tarkentaisi sanoilla “selvästi” “merkittävästi” tai julkaisisi alustavat luvut ennakkoon. Kuten Duellkin teki vuonna 2023.

Osake on tullut yli 40% alas että kyllä siinä jo pikkusen huomioitu tuloksen laskua.

Itseä yllättää ettei yhtään povaa käännettä markkinaan ja tulokseen.

Käänteisestä splitistäkin jo yli puolittunut, aina on varaa tulla alas vaikka tulostakin tekee.

Ahkera iltatyöläinen Tommi Saarinen on antanut ennakkokommenttinsa, kun Duel julkaisee Q4-rapsansa torstaina. ![]()

Duell julkistaa tavanomaisesta poikkeavaa tilikauden jaksotusta mukaillen Q4-raporttinsa torstaina 16.10. Odotamme liikevaihdon laskeneen lievästi vertailukauden tasosta ja kannattavuuden jatkaneen vaisua kehitystä epäsuosiollisen myynnin jakauman johdosta. Taseasema säilyy kireänä, mutta emme odota mahdollisen kovenanttiehtojen ylityksen aiheuttavan käänteentekeviä negatiivisa seurauksia. Kiinnostus tilinpäätöspäivänä kohdistuu taseaseman lisäksi alkanutta tilikautta koskevaan ohjeistukseen sekä kommentteihin liittyen pidemmän aikavälin taloudellisia tavoitteita, sillä yhtiö poisti aiemmat tavoitteet tulostason jäätyä odotuksista päättyneellä tilikaudella. Tarkistimme liikevaihdon ennustettamme lievästi ylös ennakon yhteydessä, mutta liikevoiton ennusteisiin tällä ei ollut vaikutusta.

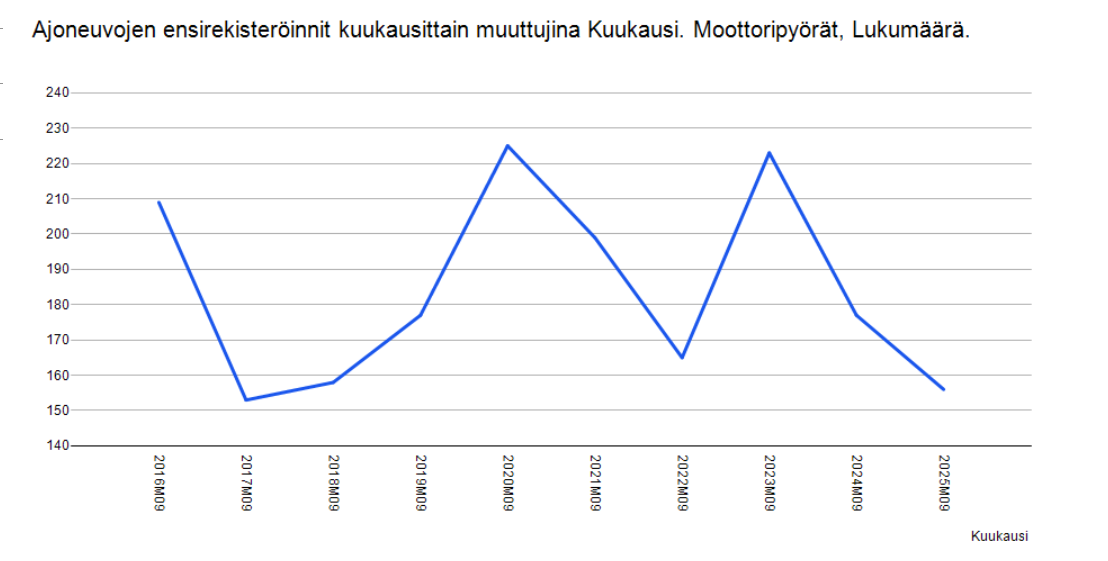

Vaisu syyskuu moottoripyörien rekisteröintien suhteen:

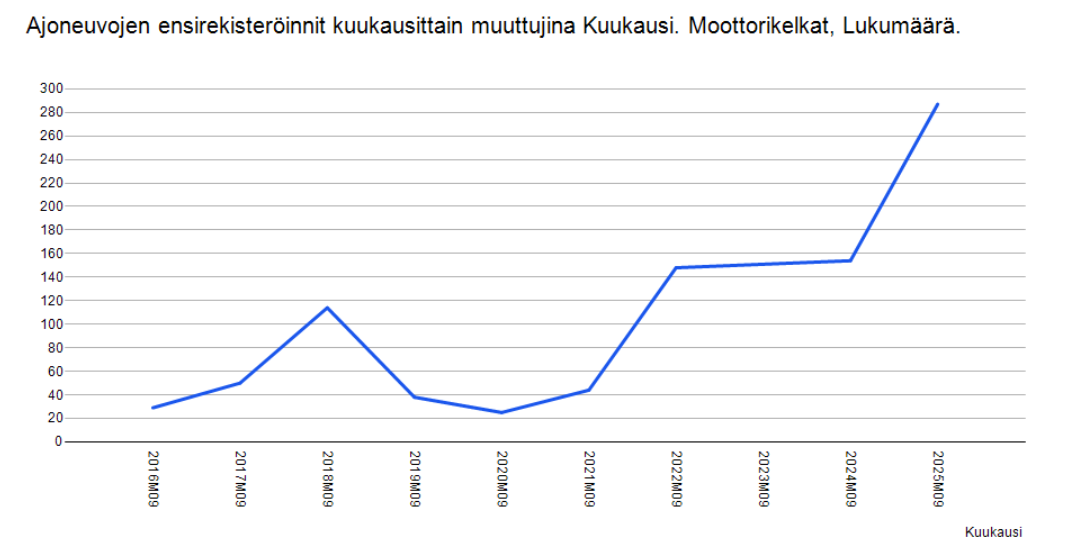

Moottorikelkoissa sitä vastoin todella vahvaa kasvua:

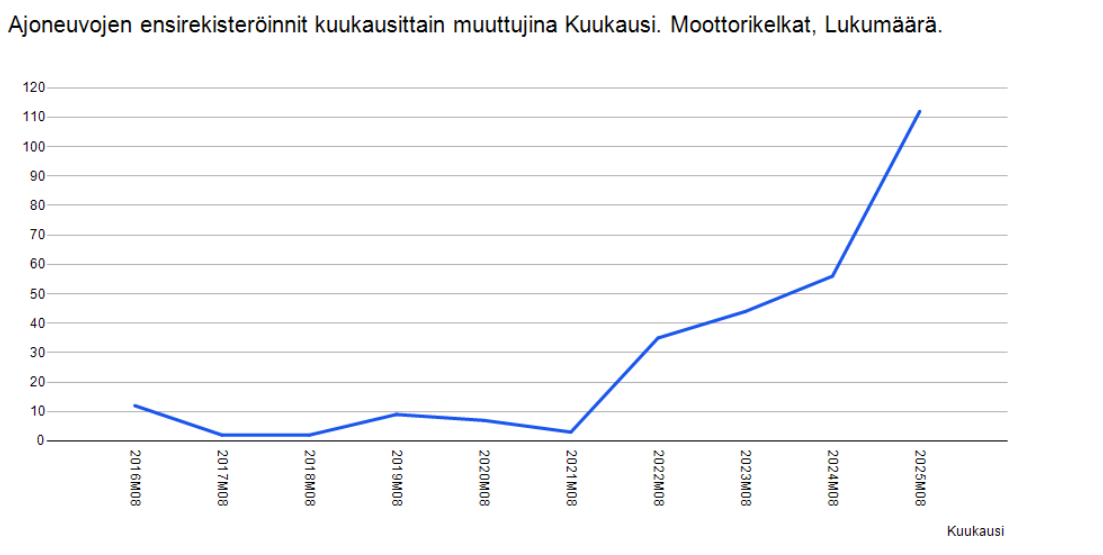

Elokuu oli jo tosi vahva:

Näkyyköhän näissä syksyn moottorikelkkarekistöröinneissä Lapin vahvat matkailun kasvuluvut ja safaritalot hankkivat uusia kelkkoja turistien käyttöön? Vai onko jotain muutoksia rekisteröintien suhteen joka selittää todella vahvan kasvun?

Aika satavarmasti kyseessä on uudet safarikelkat joten tuosta ei hirveästi kannata mitään johtopäätöksiä vetää eikä muutenkaan uusista laitteista Duellin osalta kun myyvät pääasiassa varaosia vanhoihin laitteisiin.

No ei suoraan toki, mutta on Duellin kannalta kyllä hyvin merkittävää minkä verran suomalaiset hankkivat moottoripyöriä, kelkkoja yms. joihin juuri näitä varaosia/varusteita hankitaan. Aika tarkkaan Duell itsekin seuraa ensirekisteröintejä eri maissa. Toki monesti myös ostetaan varusteita kun hankitaan uusi kulkuväline.

Ensireaktiot tilinpäätöstiedotteeseen huomenna livessä. Tervetuloa mukaan! ![]()

Duellin Q3 ulkona, ahaa, taisi ollakin tilinpäätöstiedote, yhtiö ei itsellä seurannassa: Duell Oyj tilikauden 2025 liiketoimintakatsaus syyskuu 2024–elokuu 2025 | Kauppalehti

Alla esitetyt koko vuotta sekä vertailuvuotta koskevat luvut on johdettu julkistetusta tilinpäätöksestä. Tilivuoden luvut ja kvartaaliluvut ovat tilintarkastettuja. Vertailukauden luvut perustuvat tilintarkastettuun tilinpäätökseen.

Kesäkuu 2025–elokuu 2025 “Q4 2025” (vertailuluvut suluissa 6/2024–8/2024):

Liikevaihto laski -2,3 % ja oli 30,9 miljoonaa euroa (31,6 miljoonaa euroa). Vertailukelpoisilla valuuttakursseilla laskettuna liikevaihto laski -1,1 %.

Oikaistu EBITA oli 1,0 miljoonaa euroa (1,4) ja oikaistu EBITA-marginaali oli 3,4 % (4,3 %).

Nettokäyttöpääoma oli 50,0 miljoonaa euroa (48,3 miljoonaa euroa).

Liiketoiminnan kassavirta oli 2,9 miljoonaa euroa (7,4 miljoonaa euroa).

Syyskuu 2024–elokuu 2025 “2025” (vertailuluvut suluissa 9/2023–8/2024):

Liikevaihto kasvoi 1,6 % ja oli 126,6 miljoonaa euroa (124,7 miljoonaa euroa), täysin orgaaninen kasvu. Vertailukelpoisilla valuuttakursseilla laskettuna liikevaihto kasvoi 0,8 %.

Oikaistu EBITA oli 4,9 miljoonaa euroa (6,2) ja oikaistu EBITA-marginaali oli 3,9 % (5,0 %).

Nettokäyttöpääoma oli 50,0 miljoonaa euroa (48,3 miljoonaa euroa).

Liiketoiminnan kassavirta oli 1,6 miljoonaa euroa (-0,9 miljoonaa euroa).

Osakekohtainen tulos oli -0,20 euroa (-0,00 euroa) (katsauskauden lopun osakemäärän mukaan).

Ohjeistus 2026

Kuluttajien luottamus on edelleen heikkoa ja markkinoiden epävarmuus jatkuu.

Duell odottaa markkinaympäristön pysyvän heikkona seuraavan 12 kuukauden ajan.

Siksi ohjeistuksemme tilikaudelle 2026 on seuraava:

Duell odottaa orgaanisen liikevaihdon pysyvän samalla tasolla kuin edellisenä vuonna.

Duell odottaa oikaistun EBITA:n pysyvän samalla tasolla kuin edellisenä vuonna.

Pikaisella vilkaisulla:

-Pahin pelko eli lisäpääomituksen tarve väistettiin. Kovenantit meni rikki, mutta waiveri saatiin. Lisäksi kovenanttiehtoja muutettu lokakuussa sopimaan Duellille paremmin.

-Kannattavuus odotuksia parempi. Myyntikatemarginaali palautui.

-Velkaa enemmän kuin analyytikoilla odotuksissa, jota selittää suurempi vaihto-omaisuuden määrä mitä kertyi vaikeilla keliolosuhteilla Q2 ja Q3 sekä pari miljoona korkeammilla myyntisaamisilla. Q3:han nämä ostovelat ja myyntisaamiset olivat niin suosiolliset, että velkaisuus näyttikin “liian hyvältä”. Lisäksi toteutettu Ranskassa toimenpiteitä “** Vertailukelpoisuuteen vaikuttavat erät, EBITDA: Ranskan varasto siirtoon liittyvät kustannukset 600 000 euroa.”

-Ohjeistus vaisu

-Pohjoismaat suoritti paljon analyytikoiden odotuksia paremmin ja heikkous oli tällä kertaa Euroopassa (Ranska pääsyyllinen ilmeisesti)

En itse pääse webcastiin linjoille, mutta olisi mielenkiintoista kuulla:

Lisäksi kysymys toimarille, että kauanko luvattuja osakkeiden ostoja pitää vielä odottaa.

Lopuksi haluan kiittää kaikkia organisaatiomme jäseniä heidän ponnisteluistaan tilikauden aikana. Vuosi oli haastava, mutta keskittymällä tunnistettuihin kehitysalueisiin olen varma, että vahvistamme Duellia edelleen ja parannamme sen tulosta alkaneella tilikaudella.

Toimarin kommenteissa kuitenkin näin. Jätettiin tilaa posarille tällä kertaa.