I finally decided to create a thread for this so I don’t have to spam the Stock Price Monitoring thread ![]() .

.

Coala Life makes systems/applications/devices for heart monitoring (I’m not very familiar with the industry, so I can’t say for sure). So, the sectors are SaaS and health tech. They have already accumulated a good number of patents and product approvals/recommendations, so the technology risk is limited, and sales should really pick up speed this year. The company went public last year in a slightly unusual way when a former company “bought” it onto the exchange and sold off its old businesses.

"Coala Life is a medical device company founded in Sweden focusing on cloud-based cardiac and pulmonary diagnostics. The company has developed and launched the Coala Heart Monitor - a multi-award winning, FDA-cleared and CE-approved product platform enabling long-term remote monitoring, analysis and algorithm-based diagnostics of heart and auscultation of lungs, remote in real-time. The Coala Heart Monitor is mainly marketed to healthcare providers as an Rx solution for use in patient’s everyday life and home environment. The company’s solutions are based on over 10 years of R&D, and are protected by more than 30 patents. The head office is based in Uppsala, Sweden and since 2019, the US office is based in Irvine, California. More than 10,000 patients have used, been diagnosed or are under long-term monitoring with the Coala Heart Monitor. In the Coala Care Portal, there are currently more than 1,700 doctors and nurses connected to more than 500 care providers. "

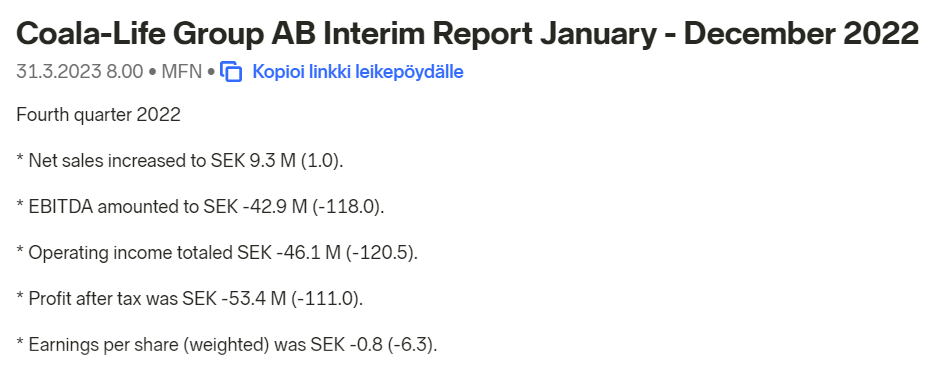

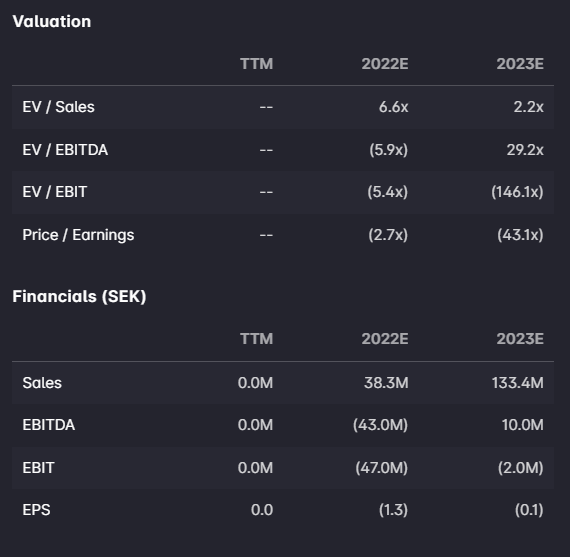

The company is, of course, still heavily loss-making, but the figures for previous quarters have apparently been affected by matters related to the listing arrangements. Dilution has been significant, and due to the unusual listing, the company’s valuation was challenging (and at least on Nordnet, misleading), which is why the stock price looks… very interesting. Red Eye’s forecasts:

Q1:

Coala_Q1_2022_SV_FINAL.pdf (coalalife.com)

A fairly large acquisition was announced a moment ago.

To which Red Eye commented:

Coala Life: Initial Take on the Acquisition of Vitrics (redeye.se)

The CEO just added a good chunk today:

“Coala Life’s CEO, Dan Pitulia, acquired 500,000 shares on June 9, 2022 at a total value of approximately 1,6 MSEK, with an average price per share of 3.2277 SEK. The shares were acquired on Nasdaq First North Growth Market.

Following the acquisition, Dan Pitulia owns a total of 3,411,279 shares, corresponding to 4.29 percent of the outstanding shares in Coala-Life Group AB (publ), as well as 1,271,706 warrants, the ownership is in person and through related parties and companies.”