CapMan’s extensive report is finally out! ![]() It’s been quite a while since my previous extensive report, as if I recall correctly, I updated the last one in '22, and then Kasper updated the extensive report in '24 during my sabbatical. True to its name, the report became quite extensive as I got excited about writing and covering things very broadly. I don’t remember spending this many hours on an extensive report in a while, as I went through the industry comprehensively again.

It’s been quite a while since my previous extensive report, as if I recall correctly, I updated the last one in '22, and then Kasper updated the extensive report in '24 during my sabbatical. True to its name, the report became quite extensive as I got excited about writing and covering things very broadly. I don’t remember spending this many hours on an extensive report in a while, as I went through the industry comprehensively again. ![]()

I didn’t touch the forecasts in the report because I practically already made the changes in connection with the Q1’24 report. I couldn’t find reasons for changes in the big picture either, no matter how much I went through this. The company will be raising capital for practically all its strategies during 2026-2027, and if successful, AUM (Assets Under Management) should grow significantly. Although the fundraising market remains difficult, the situation is gradually easing, and additionally, the company has made significant investments in its own sales organization. There will be big differences in fundraising between product groups. In Infra, this should be a so-called “slam dunk,” while in real estate (Nordic Real Estate IV), fundraising will continue to be challenging. ![]()

If the company succeeds in fundraising according to our expectations, revenue will grow briskly. This growth should reflect strongly in the fee result (= operating profit based on recurring fees). The fee result is still at a very modest level and should leap to the next level from here. Given the highly scalable nature of the industry, that scaling shouldn’t be “rocket science” (Amerikan temppu), even though CapMan has undeniably had challenges with its cost efficiency in the past. In our forecasts, the scaling doesn’t happen at any crazy ratio, and if the company were to make cost adjustments at the same time (which I don’t think they will do by any means), the upward leverage could be significantly larger than our forecasts. ![]()

The valuation picture is exceptionally two-sided. With the current fee result, the value of the Management Business remains low, and the sum-of-the-parts actually falls below the current share price. On the other hand, if that growth materializes and the earnings scale, the sum-of-the-parts is easily above the current price. ![]()

Regarding the balance sheet, it is important for investors to understand that CapMan will start releasing significant amounts of capital from the balance sheet in the coming years. This is due to large investment commitments made previously and a slowed-down exit market. According to my calculations, CapMan will easily recoup EUR 100 million from its EUR 180 million portfolio by the end of the decade, and the company won’t invest nearly that much into its new funds. Consequently, cash flow will certainly be higher than earnings. In my opinion, downsizing the investment portfolio is more than justified anyway, as CapMan’s value currently relies heavily on the investment portfolio. In an optimal situation, the value rests mainly on the Management Business, and the investment portfolio is a supporting component. ![]()

What will CapMan do with this excess cash flow? Most likely, they will at least pay down some debt, but the rest will be distributed to shareholders and/or used for growth investments (practically M&A). In my opinion, it is a good assumption that from 2027 onwards at the latest, CapMan will distribute at least its entire result as dividends. ![]()

Why am I not at a BUY rating when next year’s P/E is 10x? ![]() Do I not believe in my own forecasts? The stock is undeniably cheap if the forecasts come through, and this would make a good Buy case. However, what rubs me the wrong way is that there is still very little concrete evidence available regarding those fundraisings. A moderately sized first closing was made for the forest fund, and a seed investment has been secured for NRE4. That is all the concrete evidence so far. If we had, for example, a strong first closing for Infra III (around 300m or so) and a reasonable first closing for NRE4 (even 150m) on the table, it would be easier to take an anticipatory stance. The fact remains, however, that if those fundraisings fall short and schedules are extended, it will flatten the growth curve and essentially weaken the scalability.

Do I not believe in my own forecasts? The stock is undeniably cheap if the forecasts come through, and this would make a good Buy case. However, what rubs me the wrong way is that there is still very little concrete evidence available regarding those fundraisings. A moderately sized first closing was made for the forest fund, and a seed investment has been secured for NRE4. That is all the concrete evidence so far. If we had, for example, a strong first closing for Infra III (around 300m or so) and a reasonable first closing for NRE4 (even 150m) on the table, it would be easier to take an anticipatory stance. The fact remains, however, that if those fundraisings fall short and schedules are extended, it will flatten the growth curve and essentially weaken the scalability. ![]()

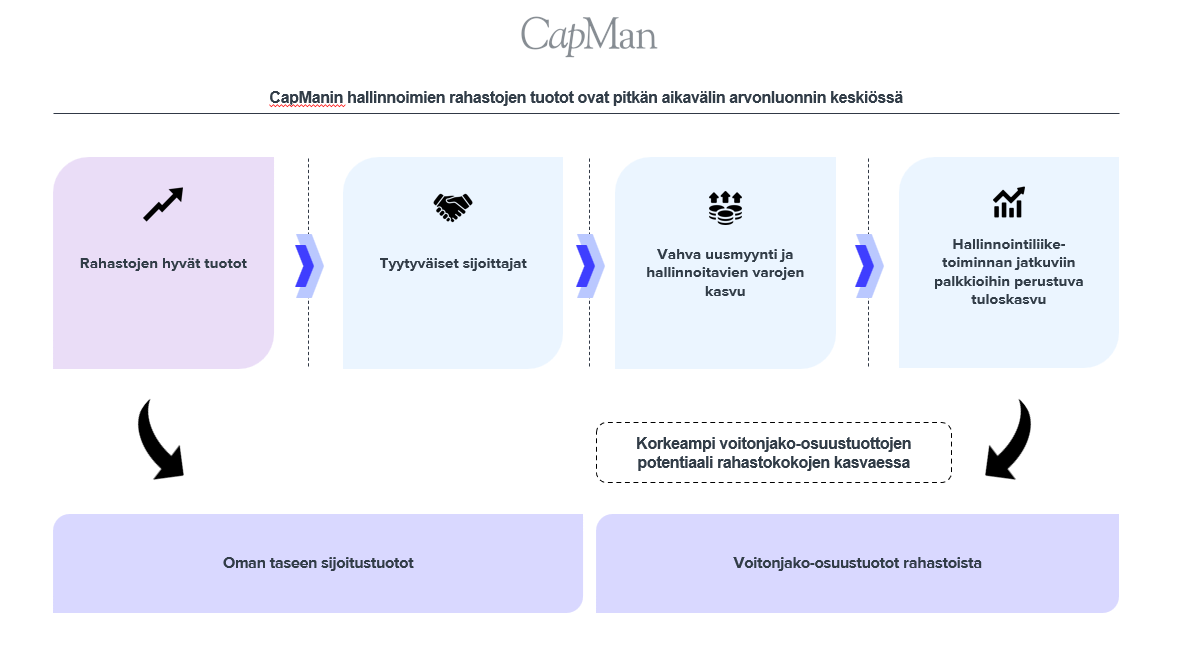

Finally, a reminder about CapMan’s business model and the fact that the whole thing ultimately rests on the good returns of the funds. If your products perform well, the other components will work too. Conversely, if the funds do not succeed, everything else becomes difficult. Fund performance is very hard to track from the outside, and the best metric for investors is carried interest income. If you don’t get carried interest, it unfortunately indicates that the underlying funds are staying below the hurdle rate. In a single vintage, this can be okay if the vintage has been terrible and you outperform peers. For example, in real estate vintages raised just before interest rates rose, you don’t need to expect carried interest, but being “at the top of the pile of corpses” is a decent performance. However, in the long run, the hurdle rate should be reached systematically. Here too, CapMan has a clear point to prove, as several large funds should move into the carry phase over the next two years. ![]()