Ao pitkässä artikkelissa käsitellään useiden muiden firmojen (mm Saab, W5, Mildef yms) ohella Bittiumia. Sen verran tuore, että Indra-kaupatkin jo kauppoja.

Bittium (markkina-arvo 1 mrd. EUR) – Suomalainen turvallisen viestinnän asiantuntija skaalautuu NATO-tason taktisten verkkojen avulla

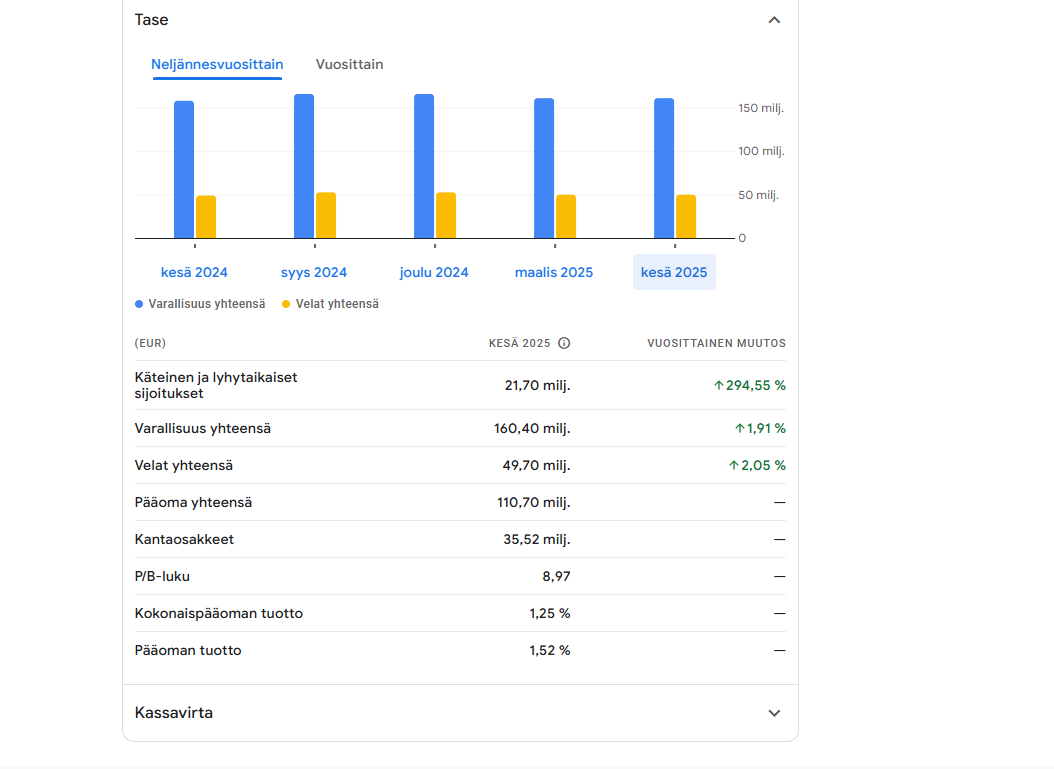

Bittium on suomalainen teknologiayhtiö, joka on erikoistunut turvallisiin viestintä- ja liitettävyysratkaisuihin puolustuksen, yleisen turvallisuuden, kriittisen infrastruktuurin ja lääketieteellisten sovellusten aloilla. Nykyisessä syklissä Bittiumin liikevaihto on kasvanut vuoden 2022 82,5 MEUR:sta, jolloin liiketulos oli lähellä nollaa ja tilauskanta noin 28 MEUR, vuoden 2024 85,2 MEUR:oon, jolloin tilauskanta oli 45 MEUR ja liikevoitto 8,6 MEUR eli 10,1 %:n kannattavuudella. Bittium saavutti juuri läpimurron Espanjassa yhteistyössä Indran kanssa ja nosti vuoden 2025 ohjeistustaan 116–120 MEUR:n liikevaihtoon ja 19–21 MEUR:n liikevoittoon. Tämä sisältää pienen osan Indran kanssa tehdystä teknologiansiirtosopimuksesta, mutta myös taustalla oleva tuloskehitys on erinomaisella uralla.

Sodan vauhdittama Euroopan puolustusbudjettien kasvu on nostanut Bittiumin Defense and Security -liiketoimintaa, sillä taktisten IP-verkkojen, ohjelmistoradioiden ja turvallisten viranomaisälypuhelinten kysyntä on kasvanut asevoimien ja turvallisuusvirastojen keskuudessa, kun taas sen lääketieteelliset ja T&K-palvelutoiminnot ovat pysyneet paremmin suojassa konfliktisykliltä. Mielestämme tällä yhdistelmällä on merkitystä. Osa nykyisestä kasvusta on konfliktin ajamaa, kun NATO- ja EU-maat nopeuttavat taktisten verkkojen sekä johto- ja hallintajärjestelmien modernisointia lyhyellä aikavälillä, mutta suuri osa kysynnästä on strategista ja liittyy monivuotisiin ohjelmiin, joilla vahvistetaan johtamista, hallintaa ja viestintää sodan välittömän tempon sijaan. Yhdessä kustannusleikkausten ja uudelleen suunnatun strategian kanssa tämä parantaa Bittiumin edellytyksiä kasvuun ja kannattavuuden parantumiseen taktisten verkkojen modernisoituessa.

Näemme nykyisen arvostuksen sisältävän aggressiivisia odotuksia jopa Indra-kaupan jälkeen. Vuoden 2025 ohjeistuksella Bittiumin Defense and Security -segmentin EV/EBIT on noin 45-50x (arvioitu konsernin nykyisen arvostuksen perusteella), joten yhtiön olisi saavutettava poikkeuksellisen suuria voittoja puolustusalalla lähiaikoina, jotta arvostuskerroin näyttäisi mukavalta. Koska Bittiumilla näyttää tällä hetkellä olevan vankka teknologinen etumatka suuriin kilpailijoihin nähden erittäin kyvykkäiden taktisten IP-verkkojen ja ESSOR-aallonpituuksien kanssa yhteensopivien Tough SDR -radioiden ansiosta, se voisi saavuttaa merkittävän markkinaosuuden tulevina vuosina ja tuottaa vaaditut tulokset. Indra-kauppa Espanjassa todistaa, että Bittiumilla on edellytykset voittaa myös ”kansalliset mestarit”, joten näkymät ovat erinomaiset. Nähtäväksi jää, riittääkö se oikeuttamaan 1 mrd. EUR:n markkina-arvon.

Kauppalehdessä tuore artikkeli Bittiumin hurjasta lennosta ja siinä haastateltu OP Pohjolan analyytikko Kimmo Stenvallia ja mikä pisti silmään Factsetin lukuihin perustuva kaavio, jossa ennuste 2025 osingoksi 2,35€ (ja 2026 2,46€)…onkohan tuo aivan hatusta vedetty vai mitä mieltä porukat?

Hienoa, siinä ilmapallo tyhjennettiin kertapistolla, ihmettelin noin korkeaa lukua mutta en itse keksinyt mennä kertomaan listatut osakkeet tuolla mainitulla luvulla…kaikkea ne toimittajat toimittavat??

Tässä Jussi Halmeen video Bittiumista. Toki enemmän yhtiötä seuranneille ei pitäisi olla hirveästi uutta.

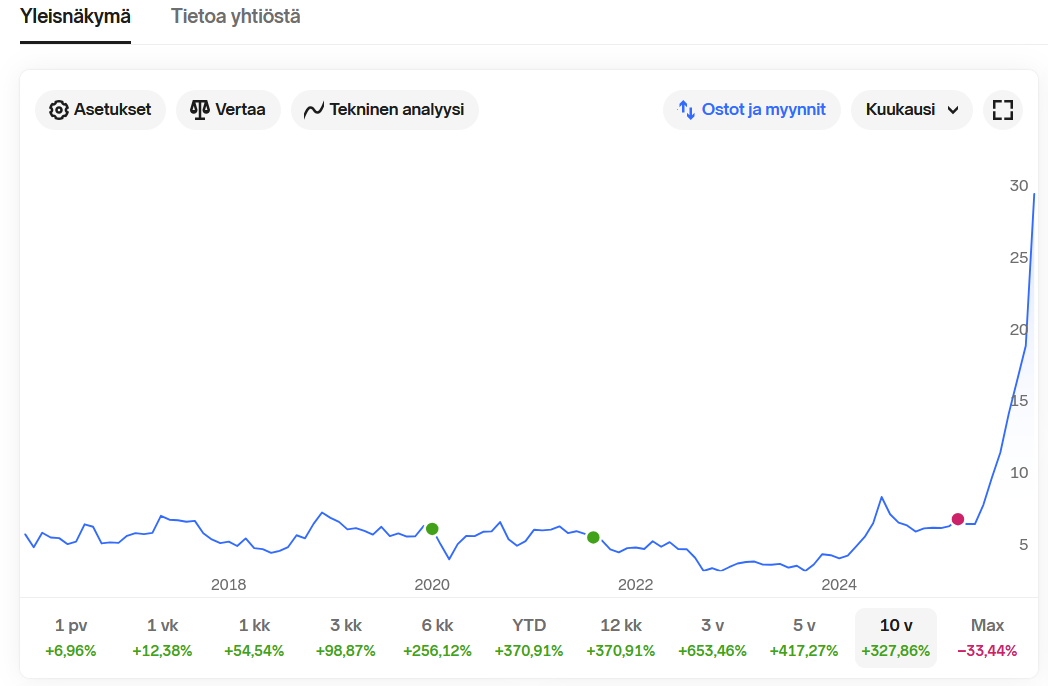

Bittium on noussut Helsingin pörssin kuumimmaksi puheenaiheeksi yli 300 % kurssinousullaan. Mutta onko kyyti jo kylmää uusia sijoittajia ajatellen? Tässä videossa perkaamme Bittiumin hurjaa muodonmuutosta oululaisesta teknoyhtiöstä Euroopan puolustusmarkkinoiden kiinnostavaksi peluriksi.

Käymme läpi Defense & Security -yksikön kasvun, tuoreimmat Q3-luvut sekä ne kriittiset riskit, joita miljardin euron markkina-arvo ja kireät arvostuskertoimet tuovat mukanaan. Onko Bittium enää järkevä sijoituskohde vai onko tulevaisuuden potentiaali jo syöty? Hyppää mukaan pohtimaan, onko kyseessä kallis mahdollisuus vai puhdas odotuspeli.

Kiitos tästä! Jussi on positiivinen, jalat maassa oleva ja selkeästi puhuva kaveri, suosittelen ottamaan kanavan kuunteluun. Bittiumin pienomistajana kaipasin jo vaihtelua sille sokerihumalaiselle kirjoittelulle, joka Bitin ympärillä vallitsee. Omakohtaisesti olen kokenut jo vastaavan Revenion suurena omistajana, kun taivas oli rajana ja 60€:ssa ostin vielä lisää. Bitti on hyvällä polulla, mutta kuten Jussi osuvasti toteaa, nyt kurssi hinnoittelee jo auvoista blue ocean tulevaisuutta ihan samoin mitä oli Reveniossa muutama vuosi sitten. Itsellä kaikki Reveniot jäi salkuun ja tämän Bitin kanssa en juuri nyt tiedä, ostaako takaisin “erehdyksessä” myydyt siivut vai seurata lukujen kasvua nykyisellä positiolla. Perusteltuja mielipiteitä ja analyysiä Bitistä kaipaan lisää ja kiitos Jussille hyvistä videoista. Ps. Siirtäkää kahvihuoneeseen, jos ei kuulu tähän ketjuun.

En nyt löytänut oikeen parempaakaan ketjua tälle löytänyt, mutta ylläpito voi siirtää tarvittaessa muualle.

Sijoitusvuosi on itselle ollut kyllä isossa kuvassa oikein hyvä (ytd 22%), mutta isoin “moka” tälle vuodelle on osunut Bittiumiin. En tiedä onko täällä hengenheimolaisia, mutta itsehän laitoin kaikki lappuni laitaan 2025 maaliskuussa ja tätä loppuvuoden nousujuhlaa on saanut seurata katsomosta. Ei tämä asia ole oikeestaan yhtään vaivannut vuodenaikana, mutta tässä ihan viimesinä viikkoina tämä katsomosta seuraamienn on alkanut ärsytttämään, kun tätä nousutarinaa nyt tunnutaan hehkuttavan aivan jokaisessa kanavassa mitä tulee seurattua.

On toki aika rohkeaa sanoa, että olisiko sitä muka malttanut olla myymättä näitä osakketa esim 15 euron kohdalla (itse myin 9 euron hintaan) ja pitää koko potin salkussa läpi vuoden. Toki tämä rakettinousu on tapahtunut noin 2 kuukauden sisällä.

Tuon myynnin taustalla on kyllä ihan perinteinen oppikirjaesimerkki sijoitus psykologiasta. Ensimmäiset ostot vuonna 2020 ja lisäystä vuonna 2021. Matkan aikana on käyty varmaan -40% tuotossa, mutta isossa kuvassa olen nähnyt yhtiön aina potentiaalia omaavana, mutta piippuun on jääty potentiaalin lunastamisessa. Sitten kun tämä puolustushype alkoi, niin siinä alkoi jo hieromaan käsiä, että nytkö se ketsuppipurkki aukeaa. Aika nopeastihan vuoden 2024 aikana noustiin tuonne 8-9 euroon, mutta siihen se nousu sitten pitkälti jäi toviksi.

Tässä kohtaa on toki myös hyvä sanoa, että Bittiumin liiketoimintaa en oikeasti syvällisesti ymmärrä, mutta kyllä tuo 2024 ja 2025 alkupuoli sai itseni jotenkin kypsäksi siitä, että eikä tämä potentiaali nytkään realisoidu ja tässä on nyt vain noustu puolustushypen avulla. Niinpä päätin kaikki osakkeet myydä noin 20% tuotolla, mutta osakehan on tuon jälkeen noussut noin 350%, joten kait se on inhimmillistä, että jollain tasolla asia harmittaa. Huvittavaa on vielä se, että tuon minun myynnin jälkeen osake taisi vielä laskea johonkin 7 euroon ja ehdin pitää itseäni jo nerona ja taputella vähän omaan selkään .

Ei tämä lisäarvoa keskusteluun juuri tuonut, mutta ajattelin nyt yhden yksityissijoittajan tarinan jakaa siitä, että on tällä osakkeella joku onnistunut töpeksimäänkin tänä vuonna. Onnittelut kaikille nykyisille omistajille ja hyvää uutta vuotta!

50 meur tilaus on sopimuksen mukainen tilaus lisenssistä. Kokonaisuutena tällainen lisenssikauppa pitää sisällään lisenssitulon, teknologian ja tuotannon siirtoprojektit sekä lopulta royaltituloa. Olemme sopineet asiakkaan kanssa, ettei kaupan yksityiskohtia avata tämän tarkemmin. Sopimus ei sisällä Bittiumin valmistamien Tough SDR -radioiden myyntiä Indralle, eikä mitään muitakaan Bittiumin taktisen tuoteportfolion tuotteita (TACWIN, Comnode tai ohjelmistot) tai Security-tuoteportfolion tuotteita. Mikäli näitä päästäisiin myymään, olisi kyseessä ihan oma erillinen kauppa - mikä luonnollisesti olisi erittäin tavoiteltavaa kauppaa

Näin vuoden viimeisenä päivänä kiitokset vielä teille palstalaisille hyvistä ja hedelmällisistä keskusteluista yhtiön puolesta. Hyvää ja menestyksekästä uutta vuotta kaikille ja jatketaanpa sitten ensi vuoden puolella!

Ihmeellisen vähän Hesulin viime vuoden eniten noussut yhtiö puhututtaa tällä palstalla. Yhtiöllä on tällä hetkellä sen verran hyvin verkot vesillä että tänäkin vuonna tuon tittelin uusiminen ei ole täysi mahdottomuus. Bittium on niitä harvoja kotimaisia pörssiyhtiöitä jotka operoivat tulikuumalla puolustussektorilla, ja bonuksena Medical-puoli joka sekin on hyvin kasvava markkina.

Samaa mieltä, yllättävän vähäistä keskustelua firmasta ja sen mahdollisuuksista. Naapuripalstalla juttua sitäkin enemmän, mutta ei kovinkaan laadukasta..

Osakkeeseen on toki ladattu odotuksia, mutta eipä vielä olla nähty Bittiumin logoja takakannikassa tai 30e hatunsyöntilivejä. Eli ainakaan samanlaista piensijoittajahypeä ei ole havaittavissa, kuin esim. 2021 tiettyjen palstan suosikkiosakkeiden kohdalla nähtiin. Päin vastoin keskusteluissa ja Bittiumia koskevissa markkinakommenteissa tuntuu pinnan alla vallitsevan varovaisen toppuutteleva, riskejä ja kohonnutta arvostusta esiin tuova pohjavire.

Jotta kommenttini ei jäisi ihan metatasolle, niin itse omistan tätä edelleen erityisesti UK:n mahdollisuuden ja BAE-yhteistyön vuoksi. Jos britteihin päästäisiin sisään vastaavalla lisenssisopimuksella, niin olisiko sen suuruus 1x, 2x vai 5x Espanja? Kaikissa skenaarioissa tulos ja osakekurssi hakisivat ihan uusia tasoja, ja Bittiumin teknologia sementoisi asemansa vuosikausiksi eurooppalaisten asevoimien standardina. UK:n lisäksi isoja mahdollisuuksia on toki muuallakin.

Medicalin osalta en olisi yllättynyt mahdollisista yritysjärjestelyistäkään (esim. eriyttäminen), kun Defense nyt näyttää varmistavan asemansa yhtiön keihänkärkenä pitkälle tulevaisuuteen.

Tiedotteessa todetaan että Espanjalla ei ole tällä hetkellä kykyä tuottaa tällaista teknologiaa itse, minkä vuoksi on valittu kaksitahoinen strategia: hankitaan markkinoilta järjestelmät jotka mahdollistavat välittömästi saumattoman toiminnan liittolaismaiden kanssa ja samalla kehitetään Espanjan omaa kapasiteettia. Indran ja Bittiumin välinen sopimus mahdollistaa strategian molemmat vaiheet.

Tämä oman kapasiteetin varmistaminen on puolustussektorilla varsinkin isoille maille kriittinen asia. Bittiumin teknologian lisensoiminen pelastaisi Saksankin armeijan siitä pinteestä, johon se on Rohde & Schwarzin luokattoman virityksen takia joutunut.

SEBin tilaisuudesta TJ Petri Toljamon esitysmateriaali.

Kuvassa muuten droonit lentää parvessa liitettynä Bittiumin taktiseen verkkoon. Patrian yksi toimipiste sijaitsee nykyään Bittiumin Oulun päärakennuksessa. Yhteistyö voi olla aika hedelmällistä.