It’s no longer worth trying to buy Basware on the stock exchange, trading has ended with a redemption of EUR 40.10.

The stock price has been quite flat for the last 5 years if you compare the start and end points, but there have been considerable dips in between, thanks to the abysmal VVK (2019), Corona (2020), rising interest rates (2022), not to mention the company’s own contribution. I don’t feel like digging up the reason for the 2018 drop, nor do I remember it, as I didn’t own it back then.

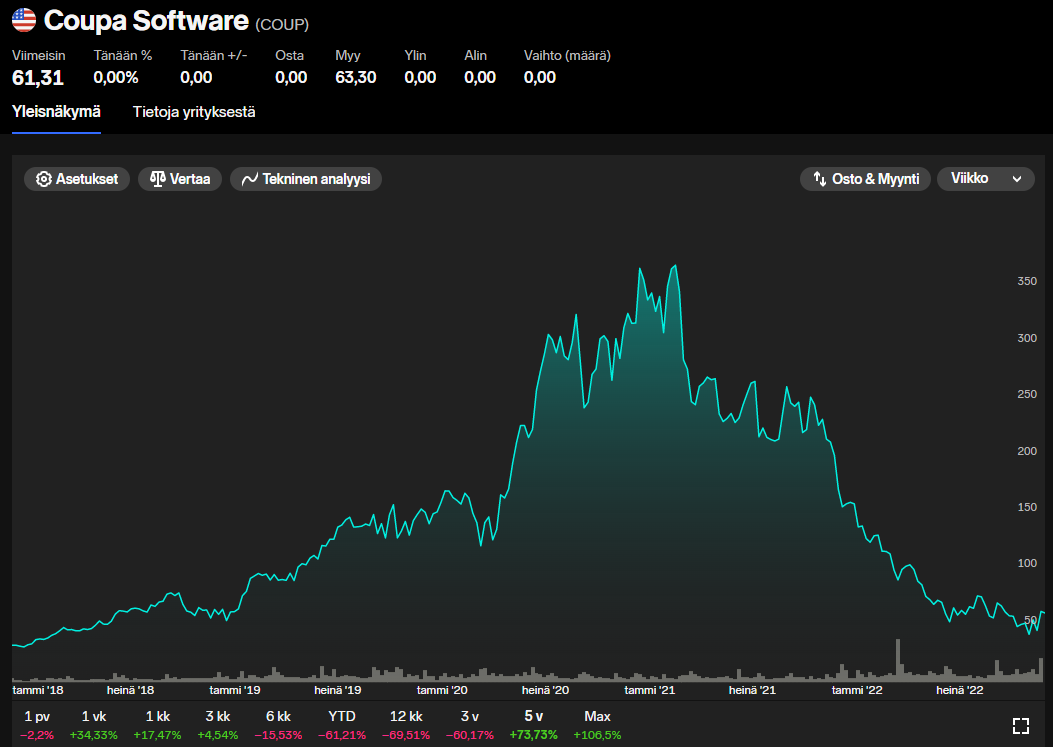

I checked an American peer, Coupa, whose valuation made me, as a Basse owner/swinger, quite envious: the Market Cap was on a different planet, you see.

Now Basware’s Market Cap ended at 580, revenue in 2021 was 153 MEUR, net profit -15 MEUR.

Coupa’s Market Cap yesterday was 4760 MEUR, revenue in 2021 was 725 MEUR, net profit -380 MEUR.

- According to the most recent quarter, the annual run-rate revenue is approx. 800 MEUR, net profit -300 MEUR.

- Coupa has traditionally achieved growth through acquisitions somewhat outside the actual Basse business.

One can conclude that Coupa has not become free despite a strong downward trend in its stock price.

If one amusingly compares Basse’s redemption price to Coupa’s valuation (by scaling revenue):

153/800 x 4760 = 910 MEUR, meaning Coupa is still valued >50% more expensively than Basse in the redemption situation in the aforementioned manner.

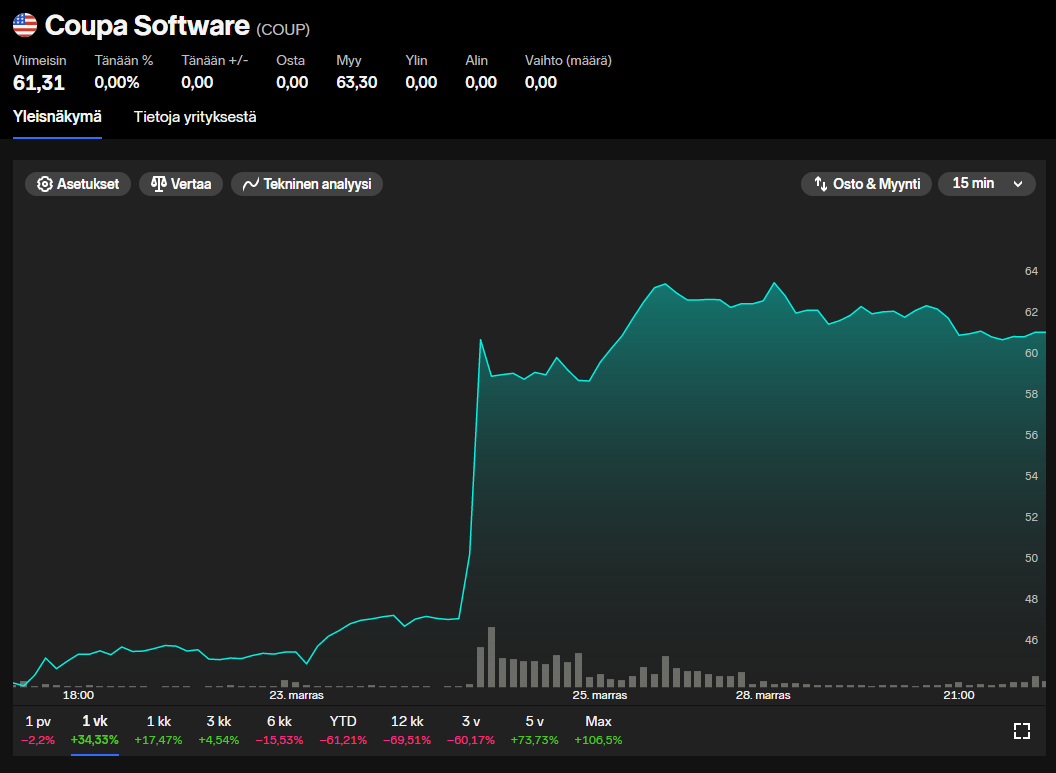

Interestingly, last week, speculation was reported that PE Vista had been exploring a Coupa privatization. That explains the latest push to the > 60 USD level. Before that, the price had fallen to 45 USD.

If you further remove that speculated premium from Coupa’s valuation, the valuation was only relatively marginally more expensive than Basse’s redemption price.

Conversely: after April 14, when Basse’s redemption was announced, Coupa’s share price has halved from the 100 USD level to that 45-60 USD range.

→ Basse’s redemption came at just the right time, it could very well be 20 EUR or so again without the redemption.