Pauli Lohen has made an overview of, among other things, meat prices and meat companies in general.

Meat prices in Finland have so far developed quite moderately compared to the increases seen in other European markets. However, there has recently been a shortage of beef, which is expected to be moderately reflected in domestic raw material prices in the near future. In addition to the moderate tightening of the cost environment, we also expect the demand environment to be somewhat challenging for meat industry companies in the early part of the year. We therefore estimate that Atria’s and HKFoods’ earnings growth will remain moderate this year.

Pauli provided his preliminary comments as Atria will publish its Q1 interim report next Thursday.

We estimate the market situation was challenging in the early part of the year due to, among other things, weak consumer confidence and rising meat prices in Sweden. At the same time, however, the company benefits from implemented efficiency measures and export growth.

The Group’s net sales grew to EUR 420.5 million (EUR 416.8 million). Atria Sweden’s net sales increased by EUR 6.8 million compared to the corresponding period last year. Atria Finland’s net sales were EUR 2.1 million lower than in the comparison period. The weak market development of Atria’s represented product categories in Finnish retail weighed on Atria’s net sales.

The Group’s operating profit was EUR 12.8 million (EUR 8.0 million), or 3.1% (1.9%) of net sales.

All business areas improved their operating profit.

Atria Finland’s operating profit was EUR 11.2 million, which was EUR 4.0 million better than in the corresponding period last year. The good profit development is a result of streamlining poultry production and concentrating production in Nurmo’s new poultry plant. The export of chicken meat to China, which started in December, also improved operating profit.

Atria Sweden’s operating profit was better than in the corresponding period last year, which was a result of successful sales to retail and Foodservice customers and the integration of the Gooh! ready-meal business into Atria in May 2024.

In the Atria Denmark & Estonia business area, both countries improved their results.

Atria Finland initiated the planning of an investment program to modernize ready-meal production and energy management at the Nurmo plant. The total cost of the project is estimated to be approximately EUR 60-90 million. The planned investment program is in line with Atria’s strategy to invest in ready meals and be a pioneer in responsible food production. The modernized ready-meal plant would enable completely new carbon-neutral food production.

The Group’s free cash flow during the review period was EUR 11.7 million (EUR -28.1 million).

Adjusted return on equity, rolling 12 months, was 11.2 percent (6.7%).

The preparation of Atria’s Group strategy has progressed as planned. The new strategy will be published at the end of the year.

After the review period

The Finnish Food Workers’ Union strike in Finland, which took place on April 8-10, 2025, halted deliveries from the Nurmo plant, with the exception of poultry products. The strike also had negative effects on Easter season deliveries.

Atria Finland is investing approximately EUR 7 million in a new pancake production line and the technical modernization of the production department.

The company appears to be in excellent financial shape. Only a small improvement in revenue, but EPS 0.28, more than double Inderes’ forecast and well above consensus.

Atria’s Q1 performance was mostly better than anticipated, as operating profit clearly exceeded our forecasts, supported by efficiency improvements from the new poultry plant. However, the company warns that the food industry strike seen at the beginning of April affected Easter season deliveries, which will have a negative impact on results for the rest of the year. The downward earnings guidance for the full year remained unchanged.

Atria is clearly a dividend stock as an investment. At the same time, management actively develops the company and seeks growth in various areas. As debt also decreases, it creates opportunities for both profit distribution and investments in line with the new, developing strategy in the coming years.

The market is constantly changing, as evidenced by the growing demand for ready-made food and more prepared food, such as pancakes. At the same time, the market for sandwich toppings in Finland decreased by almost nine percent in the early part of the year.

Note.

The author owns Atria shares.

IR Window is a channel for SalkunRakentaja’s and Sijoittaja.fi’s corporate partners for background and analytical articles, as well as other interesting investor information. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

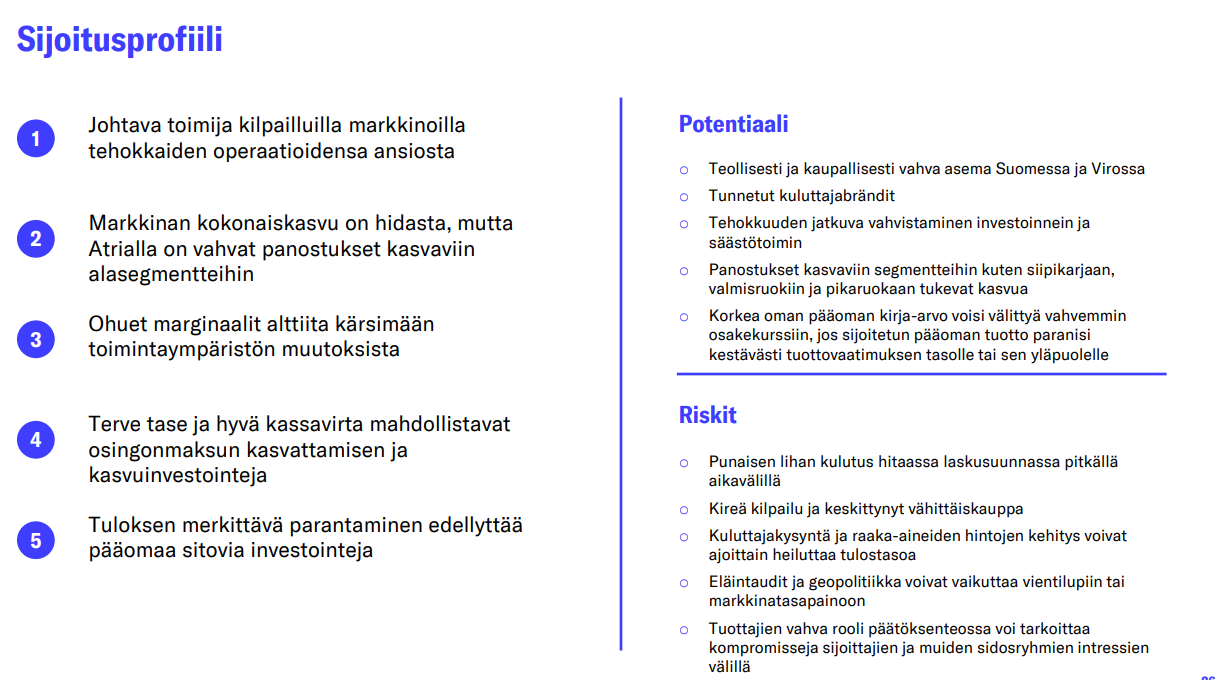

What is the basis for Atria’s current P/E and EV/EBIT valuation, which is below historical levels? How should the stock’s current valuation even be interpreted and by what metrics?

Historically, EV/EBIT of 11 and P/E of 12 have been fairly normal valuation levels for the company, but currently EV/EBIT is around 8.5 and P/E is 8. Dividend yield has historically hovered in the same 5-6% range, does that determine the share price? At the P/B level, the valuation has risen slightly, but at the same time, return on equity has also increased, meaning the rise is justified.

In my opinion, the company is now of higher quality in every respect than it was 5 years ago. A new level of profitability has been achieved, and a significant investment has been made in a new poultry factory. Many good new products have been developed in the ready-meal sector, and quark pancakes, for which a new investment is coming, have also apparently been a success of some kind. Therefore, in my opinion, the investments have been successful, considering the company’s industry.

Why has the stock’s valuation settled at a lower level? A higher quality company with lower multiples is a strange combination from the market. Shouldn’t the valuation rather be higher than historical levels? Is there still doubt about whether the company can maintain its improved earnings level? What about the fear of tariffs?

If the valuation were to correct towards historical levels in the coming years, a 30-50% increase would come solely from the valuation rise, in addition to 5-6% dividends and a moderate 2-3% earnings growth. The annual return expectation could climb close to 15% over 5 years in a very defensive industry. Without a rise in valuation, the return would then remain between approximately 5-10%.

I have been pondering that in Atria’s case, valuation multiples are influenced by at least the company’s industry, ownership structure, and to some extent, the China risk.

Industry: A large part of the business is meat production, not at all glamorous nor favored by ESG investors. The company might be seen as operating in a sunset industry, as, for example, pork consumption decreases year after year. On the other hand, the company has invested in poultry, whose consumption is steadily growing.

Ownership Structure: The largest owners are cooperatives, and this constitutes an ownership risk. The free float is small, and daily trading volumes are also small. On the other hand, it seems that despite the ownership structure, the company has been able to make sensible decisions, such as reasonable, but not excessive, dividend payments and investments (Nurmo poultry plant, previously announced investment in thin pancakes).

China Risk: In my opinion, this may have decreased recently, as the EU and China draw closer due to the Americans’ tariff disputes. However, both poultry and pork are exported to China, and especially for pork, parts of the carcass are exported that are not suitable elsewhere. If China were to impose tariffs or similar measures on these, it could have a significant impact on Atria’s profitability.

Pauli has published a new comprehensive report on Atria, the comprehensive report is available for everyone to read, as always.

Atria is one of Northern Europe’s leading food companies and a major player in the meat industry. The company’s investments are specifically targeted at growing segments, such as poultry and ready meals, which enables modest growth even if red meat consumption slowly declines in the long term. The recent rapid earnings growth is likely to slow down towards the end of the year, but we still expect an upward revision to the 2025 guidance due to a strong Q1. The value creation profile of the capital-intensive industry is moderate, but the stock’s favorable earnings-based valuation and good dividend yield make it attractive in our opinion. We raise our recommendation to Add (previously Reduce) and maintain our target price at EUR 14.0.

We forecast revenue growth to recover to approximately 2% in 2026-27, which largely corresponds to the company’s historical growth rate and is close to the assumed long-term inflation level. We expect growth to be generated fairly evenly across different units. We anticipate Atria’s market shares to develop stably overall. Investments in growth segments such as poultry and ready meals support long-term growth, but at the same time, demand for red meat is moderately declining. There could be upside potential in growth forecasts if the company’s investment plans for ready meals and production synergies between Finland and Sweden are fully realized.

Here are Pauli’s preliminary comments as the company releases its Q2 results.

Atria will publish its Q2 interim report on Thursday, July 17th, at approximately 1 PM. We estimate the result to decrease slightly from the comparison period due to factors such as food industry strikes, cool weather, and beef availability challenges. We expect the company to maintain its cautious earnings guidance for 2025 for now, even though our own earnings forecasts are slightly more positive.

One has to commend Atria, as it reports not only on the size of the investment but also on the monetary benefits it generates, more than just virtuous CO2 reductions.

Likewise, regarding the grants received.

Absolutely exemplary.

Well, perhaps the harsh reality in many other cases is that there isn’t such a good return to present…

From this, one can estimate Atria’s own contribution to be 82.4-24.7 = 57.7 million euros.

Annual savings > 5 million euros

→ 57.7/5 = approx. 11 years / yield approx. 9%

As well as the green transition tax credit (20% of 82.4%). This would apparently provide a tax benefit of 82.4 x 20% = 16.5 million euros from the investment value.

I don’t know if the tax credit works as I imagined above, but if so, it would increase savings

→ (57.7-16.5) / 5 = 41.2/5 = 8.25, yield approx. 12%

Annual energy consumption is estimated to decrease by approximately 50,000 MWh, which corresponds to 21 percent of Atria Finland’s energy consumption. The energy solutions included in this investment will achieve total annual savings of over 5 million euros.

Business Finland has granted 24.7 million euros in clean transition investment aid for the 82.4 million euro project. In addition, Atria is applying for a green transition tax credit for the investment, which can be 20 percent of the investment sum.

Technology Industries of Finland:

This tax support would reduce the corporate tax paid by companies by a maximum of 20% of the investment costs,

Q2 was financially quite good, considering the partly one-off challenges posed by the operating environment. We consider an upward revision of guidance likely, and with domestic demand picking up, there could even be upside potential in our forecasts. On the earnings day, the company announced a significant investment decision which, together with subsidies, enables the profitable upgrading of energy solutions at the Nurmo factories to be significantly more ecological. Favorable earnings-based valuation and good dividend yield support the attractiveness of the stock, even though earnings growth prospects for the coming years are very moderate.

Quoted from the report:

The announced investments in ready meals and energy efficiency will, in our view, only support earnings several years from now (mainly in forecasts only by 2028), and thus will not serve as key share price drivers in the 12-month horizon. However, we expect the company to achieve stronger results than its guidance for 2025, which, along with a potential strengthening of consumer behavior, could support the share price.

In my view, the reduction in financial expenses will compensate for the impact of the likely decrease in operating profit on net profit in the 2025 financial year. The company’s risks are described in the interim report.

In my view, there is currently no indication of a dividend reduction for the current financial year. At the current share price of 13.7 euros, Atria’s market capitalization is 386 million euros. The dividend yield on the last paid dividend is a good 5.0 percent.

Note.

The author owns Atria shares.

IR-ikkuna is a channel for background and analytical articles and other interesting investor information from SalkunRakentaja and Sijoittaja.fi’s corporate partners. The article is part of a commercial collaboration with the company. The article does not contain investment recommendations.

Here are Pauli’s comments on Atria’s efficiency measures.

Atria plans to centralize beef cutting operations at the Kauhajoki plant, which would enable annual cost savings of EUR 3 million, including personnel reductions at the Jyväskylä plant. The plan includes a significant investment of EUR 16 million in the Kauhajoki unit. This is a continuation of Atria’s active investment policy, which helps it maintain high industrial efficiency even in the industry context.

Here are Nordea’s comments stating that China’s potential tariff increases would raise Atria’s export costs by about 8 percent, but the impact would nevertheless be limited because exports are concentrated on less sought-after parts in Europe (such as heads and trotters).

Instead, European price pressures could weaken margins and the profitability of farms.

Here are Pauli’s clear and good comments on how China is raising import tariffs on pork.

According to preliminary information, the tariff level concerning Finland would not change radically, so the direct effects would remain small. The tariffs may also have indirect temporary effects through an oversupply of pork and increased competition in the EU. According to our estimate, pork exports to China have accounted for approximately 1% of the turnover for both Atria and HKFoods.

Here are also Rauli’s comments on Atria updating its strategy and targets.

Atria published its new strategy for 2025-2030, which focuses on ensuring the competitiveness of its core business, growth in selected product categories, and increasing cooperation between countries. The company also published its updated financial targets, which include a new revenue target of over EUR 2 billion and a higher return on equity target of 12% than before. The operating profit margin target remained at 5%. In our view, the updated strategy and targets do not bring significant changes, and thus do not affect our forecasts.