Kiitos isosti, nyt ymmärsin tosiaan ton päällisin puolin. Tossa tuli tosiaan nyt tiedote että järjestelyt saatu päätökseen. Tämä olikin vähän isompi juttu mitä ekaks ajattelin.

Kaikki yritysostot eivät onnistu. Assa teki 2.2b sekin alaskirjauken jostain Citizen ID:stä

Assa Abloy on vuosikausia kasvattanut omistaja-arvoaan lukuisten pienehköjen yrityskauppojen kautta. Paikallisiin “monopoleihin” perustuva lukitusbisnes on kasvanut kannattavasti. Tämä on ollut suurin yksittäinen sijoitukseni ja olen ollut tyytyväinen omistaja. Hyvä johto on myös nauttinut luottamustani.

Nyt yrityskauppojen koko (ja riski) on kasvanut. Lisäksi fokus on mielestäni vähemmän tarkka kuin aiemmin. Epäilen että lukuisten hankittujen bisnesten hallinta saattaa käydä vaikeaksi aiheuttaen yllätyksiä omistajille. En ole enää yhtä luottavainen firman menestykseen kuin aiempien 20 vuoden aikana. Olenkin vähentänyt omistustani kahden viime vuoden aikana. Nähtäväksi jää mitä tuleman pitää.

Ovat tosiaan onnistuneet kasvamaan vuosikymmeniä tällä strategialla. Olen samaa mieltä että nyt kokoluokka on normaalia isompi ja enemmän kompleksinen. Luotan silti että hyvä tekeminen jatkuu, erittäin hyvä johto ja fiksut omistajat. Latour ja Melker Schörling on omistajina sellaisia joihin voi luottaa. Olen hyvin pitkäaikainen omistaja ja lisäsin pienen siivun viimeisen vuoden aikana.

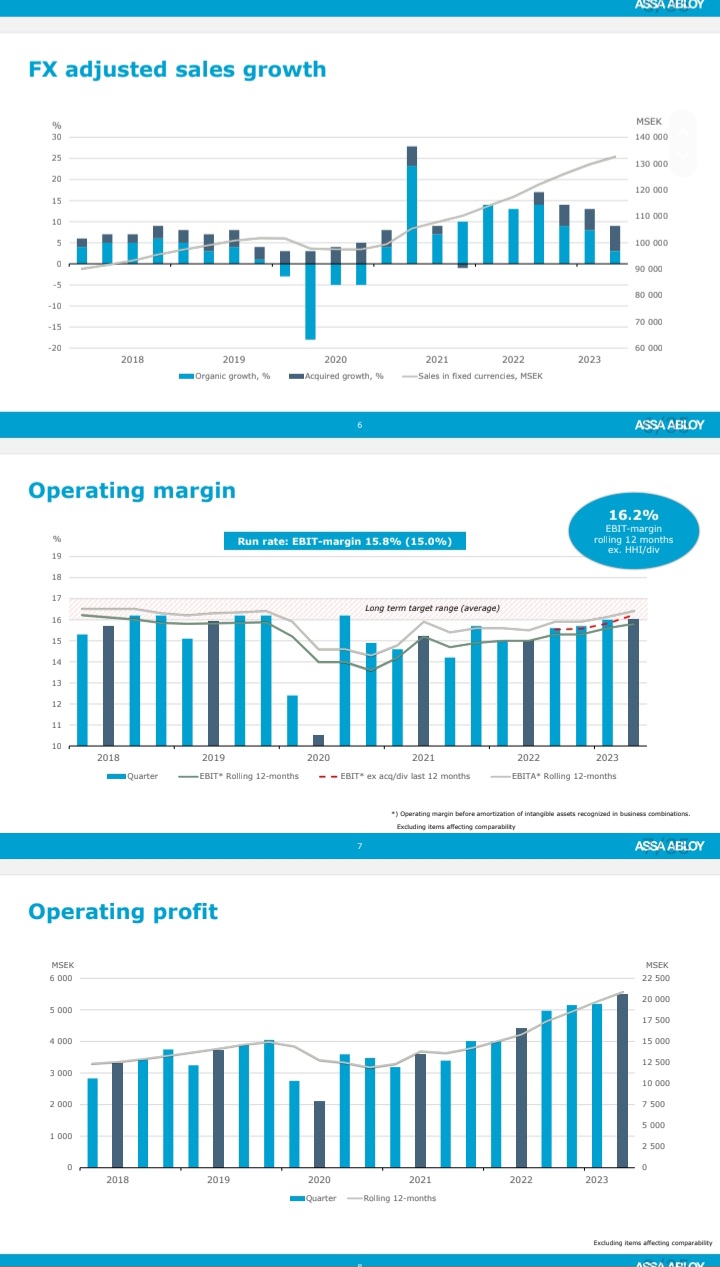

Net sales increased by 17% to SEK 34,474 M (29,466), with organic growth of 3% (13) and acquired net growth of 6% (0). Exchange-rates affected sales by 8% (12).

Very strong organic sales growth in Global Technologies, good growth in the Americas, stable in Entrance Systems, while organic sales declined in Asia Pacific and EMEIA.

The acquisition of Spectrum Brands’ Hardware and Home improvement division (HHI) was completed in June.

The divestment of Emtek and Smart Residential business in the U.S. and Canada to Fortune Brands was completed in June. The divestment gain, including exit costs, totaled SEK 3,661 M for the quarter.

Impairment of goodwill and other intangible assets in Global Technologies led to one-off costs of SEK 2,268 M before taxes.

Operating income1 (EBIT) increased by 25% and amounted to SEK 5,500 M (4,406), with an operating margin of 16.0% (15.0).

The operating margin1 (EBIT) excluding the acquisition of HHI and divestment of the Emtek/U.S. Smart Residential was 16.7%.

Net income1 amounted to SEK 3,731 M (3,156).

Earnings per share1 amounted to SEK 3.36 (2.84).

Operating cash flow amounted to SEK 6,671 M (3,787).

Tiedä mitä konsensus odotti mutta hyvin näyttää puksuttelevan…

• Omsättningen ökade med 16% till 36 881 MSEK (31 820), varav 1% (14) organisk tillväxt och 11% (3) förvärvad tillväxt netto. Valutaeffekter påverkade omsättningen med 4% (16).

• En god organisk försäljningstillväxt uppvisades av Global Technologies och Americas, stabil organisk försäljning för Entrance Systems medan organisk försäljning minskade för Asia Pacific och EMEIA.

• Tio förvärv tecknades under kvartalet med en total årsomsättning på cirka 2 000 MSEK.

• EBITA-marginalen var 16,7% (16,2).

• Rörelseresultatet1 (EBIT) ökade med 16% och uppgick till 5 777 MSEK (4 973), med en rörelsemarginal på 15,7% (15,6).

• Rörelsemarginalen1 (EBIT) exklusive förvärvet av HHI och avyttringen av Emtek/U.S. Smart Residential uppgick till rekordhöga 17,4%.

• Nettoresultatet1 uppgick till 3 656 MSEK (3 552).

-Omsättningen ökade med 12% till 36 970 MSEK (32 915), varav 0% (9) i positiv organisk tillväxt och 11% (5) förvärvad tillväxt netto. Valutaeffekter påverkade omsättningen med 1% (14).

-Stark organisk försäljningstillväxt uppvisades av Americas och god tillväxt för Entrance Systems, medan organisk försäljning minskade för Asia Pacific, EMEIA och Global Technologies.

-Sex förvärv tecknades med en total årsomsättning på cirka 900 MSEK.

-Rörelseresultatet1 (EBIT) ökade med 11% och uppgick till 5 722 MSEK (5 152), med en rörelsemarginal på 15,5% (15,7).

-Rörelsemarginalen1 (EBIT) exklusive förvärvet av HHI och avyttringen av Emtek/U.S. Smart Residential uppgick till 16,8%.

-Nettoresultatet1 uppgick till 3 969 MSEK (3 729).

-Vinst per aktie1 uppgick till 3,56 SEK (3,36).

-Operativt kassaflöde uppgick till rekordhöga 7 315 MSEK (6 588).

-Styrelsen föreslår en utdelning för 2023 om 5,40 kronor (4,80) per aktie, jämnt fördelat vid två olika betalningstillfällen.

Kylläpä orgaaninen kasvu tussahti Q4. Q4’22 orgaaninen kasvu oli sentäs 9%. En tiedä mitä markkinat odotti.

Q1 tulos ulkona, ensimmäistä kertaa orgaanista kasvua sitten Q3 -23. Jälkimarkkina (huolto, korjaus) ilmeisesti tärkeässä asemassa, kun markkinat muuten laahaa. yritysostot (ja myynnit?) laskivat katetta hieman, kuulema tilapäistä

Katselin pitkän aikavälin lukuja ja kannattavuus on ollut kyllä hyvällä tasolla niin tulovirran kuin pääomankin suhteen. (Tuossa on v. 2018 kohdalla joku kertaluonteinen kuoppa, muistaako joku, mikä se oli?).

Katselin nopeasti tuoreita lukuja (2013-2024) niin kannattavuus on hyvällä tasolla, velkaantuneisuus ehkä hieman koholla, yhtiö on kasvanut hiljalleen, tuotekehitykseen panostetaan ja osinko on ollut kestävällä pohjalla. Yritysostot ovat sitten riski, miten ne onnistuvat.

Kilpailusta en nopeasti saanut selvyyttä, mikä on perinteisten kilpailijoiden rooli ja toisaalta onko jotain uusia toimijoita, jotka voivat horjuttaa tilannetta.

Arvostuksesta en oikein osaa sanoa mitään fiksua, kun se ei ole minun vahvuuteni. Tuoreita tunnuslukuja: P/E 23,5 (tot), osinkotuotto 1,7% ja EV/MCap = 118%.

Vaikuttaisi nopeasti vilkaistuna ihan OK, pitääpä perehtyä tähän tarkemmin vielä.

Latasin huvikseni ASSA ABLOY:n koko talousdatan 2013-2024 tehdäkseni “reality checkin” mihin yhtiö on pitkässä juoksussa pystynyt. Se antaa vähän suuntaviivoja tavoitteiden realistisuudelle, toki mennyt ei ole tae tuevasta mutta jotain se kertoo kuitenkin. Laitoin mukaan myös yhtiön tavoitteet niin voitte verrata. Toteutuneet kasvuluvut siis 2013-2024 annualisoituja:

Liikevaihto +9,9% p.a. - tavoite 10%

Tulos +10,5% p.a.

Osakekurssi +9,3% p.a.

Osinko +9,9% p.a.

Eli yhteensä n. +10% kasvava yhtiö kaikilla mittareilla.

Lisäksi laitetaan tähän operating margin, joka on ollut keskimäärin 15,7% ja tavoite 16-17%. Operating margin on ollut hyvin tasainen vuosien yli, vaihtelu on ollut vähäistä.

Eli hyvin “jalat maassa” -tavoitteet suhteessa yhtiön historiaan.

PS. Tällaisen talousdatan jakamisesta pitää antaa tunnustusta, kaikki avainluvut ja tunnusluvut saa ladattua nätisti Excel-taulukkona. Kun kerta luvut ovat olemassa turha pihistellä niitä.

ASSA ABLOY on ostanut Kentix GmbH:n (”Kentix”), saksalaisen datakeskusten valvonta- ja kulunvalvontatuotteiden suunnittelijan ja valmistajan

ASSA ABLOY on ostanut Kentix GmbH:n (”Kentix”), saksalaisen datakeskusten valvonta- ja kulunvalvontatuotteiden suunnittelijan ja valmistajan.

”Olen erittäin iloinen voidessani toivottaa Kentixin tervetulleeksi ASSA ABLOYlle. Tämä yrityskauppa toteuttaa strategiaamme lisätä täydentäviä tuotteita ja ratkaisuja ydinliiketoimintaamme”, sanoo Nico Delvaux, ASSA ABLOYn toimitusjohtaja.

”Olen iloinen, että Kentix liittyy EMEIA-divisioonaan. Heidän vahva asiantuntemuksensa datakeskusten kulunvalvontatuotteissa sopii hyvin Digital & Access Solutions -segmenttimme visioon. Kentix laajentaa kykyämme nopeasti kasvavalla datakeskussegmentillä tarjoamalla integroidun, tulevaisuudenkestävän turvallisuusratkaisun, joka täydentää portfoliotamme ja asemoi meidät hyvin tällä kriittisellä vertikaalilla. Toivotamme Kentixin tiimin tervetulleeksi ASSA ABLOY -perheeseen”, sanoo Neil Vann, ASSA ABLOYn varatoimitusjohtaja ja EMEIA-divisioonan johtaja.

**Kentix perustettiin vuonna 2008, ja sillä on noin 40 työntekijää. Pääkonttori ja tehdas sijaitsevat Idar-Obersteinissa, Saksassa. **

Vuoden 2024 myynti oli noin 8 miljoonaa euroa (noin 90 miljoonaa Ruotsin kruunua) hyvällä EBIT-marginaalilla. Yrityskauppa parantaa osakekohtaista tulosta (EPS) alusta alkaen.

ASSA ABLOY on hankkinut NSP Securityn (”NSP”) Isossa-Britanniassa. Yritys tarjoaa kulunvalvontaratkaisujen suunnittelua, valmistusta ja asennusta pääasiassa opiskelija-asuntosegmentillä.

Uutinen se on tämäkin ja kiva jos saadaan tänne keskustelua!

Hankinnan kokoluokka on melko pieni: NSP:n liikevaihto reilu 9Me vuonna 2024.

Strategian mukainen kuitenkin, ASSAn tavoite on kasvaa 5% vuosittain M&A kautta + orgaaninen.

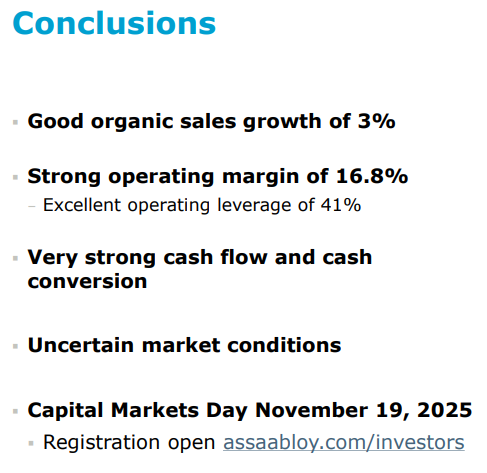

2025 tulos ylihuomenna torstaina, onko yllätyksiä odotettavissa?