Kannattaa muistaa, että PathAi:lla on myös kuvanhallinta tuon kuva-analyysin lisäksi. Ei voi ihan yks yhteen verrata hintoja.

4 tykkäystä

Näissä suomalaisissa medtech- ja lääkeyhtiöissä häiritsee usein se, että omistajista ei löydy yhtään aidosti alaa tuntevaa ammattisijoittajaa.

Revenio aikoinaan sai paljon uskottavuutta kun tanskalaiset ostivat avoimesti ison steikin. Ruotsissa ja muissa alalla pidemmät perinteet omaavassa maassa on taustalla usein lääkealaan erikoistunut VC-yhtiö joka on ennen IPOa tehnyt kunnon DD:n myös ei-julkisen tiedon ja tieteen pohjalta.

Aiforia vaikuttaa Nanoformia ja Nightingalea uskottavammalta yhtiöltä, mutta siltä kuitenkin puuttuu tuo ammattisijoittajan laatuleima. Vai olenko missannut jotakin?

5 tykkäystä

Hallitus kai tässä se tärkein on, ja se tietysti heijastaa omistajakunnan rakennetta.

Nyt puhutaan kyllä ihan eri asiasta.

Ennen listautumista tehtävissä VC-rundeissa tekee alaan syvällisesti tutustunut ja satoja keissejä nähnyt tiimi, tieteellisillä neuvonantajilla avustettuna, kunon DD:n firmasta, kilpailutilanteesta ja teknologiasta. Vaikka tuo analyysi vanhenee vuosien varrella, kertoo sen olemassaolo siitä, että keississä on ainakin joskus ollut järkeä.

Valitettavasti parhaat keissit eivät päädy pörssiin vaan myydään trade sale:llä kilpailijoille tai isoille medtech-firmoille.

Toinen mahdollisuus on sitten että pörssiin päätyneeseen firmaan tulee alan spesialistifundi joko IPO:ssa, pleissauksessa tai suoraan markkinalta ostaen. Suomessa ei tällaisia taida juuri ollakaan.

1 tykkäys

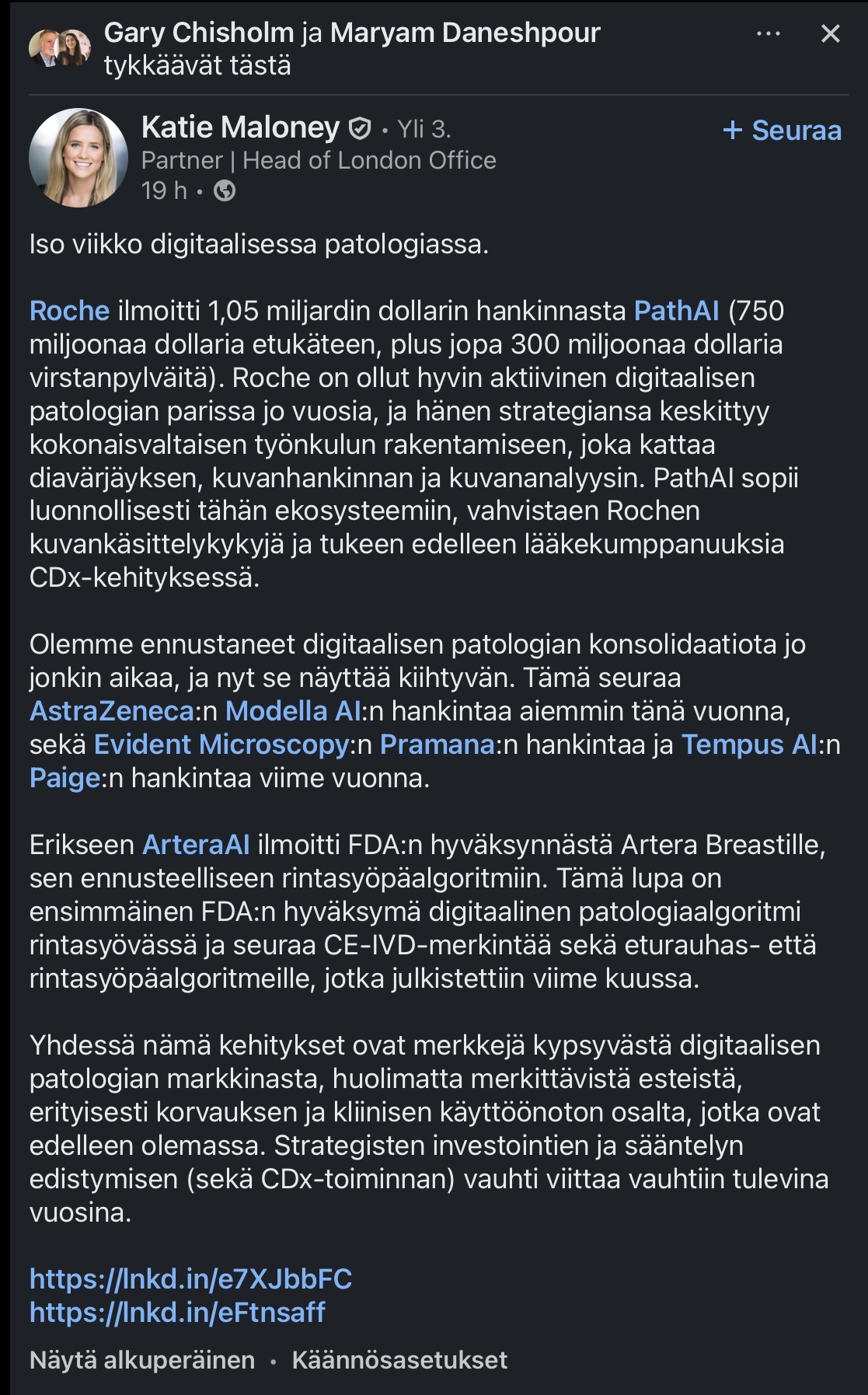

Käynnissä olevasta konsolidaatiosta kommentti viimeisimpien kauppojen osalta.

Postauksen Aiforian kannalta kuittaa Gary Grisholm, joka on viime vuonnna kilpailija Ibex digitaalipatologiasta Aiforiaan siirtynyt jenkkimyyntivahvistus. Käännösvirheistä vastaa Linkkari.

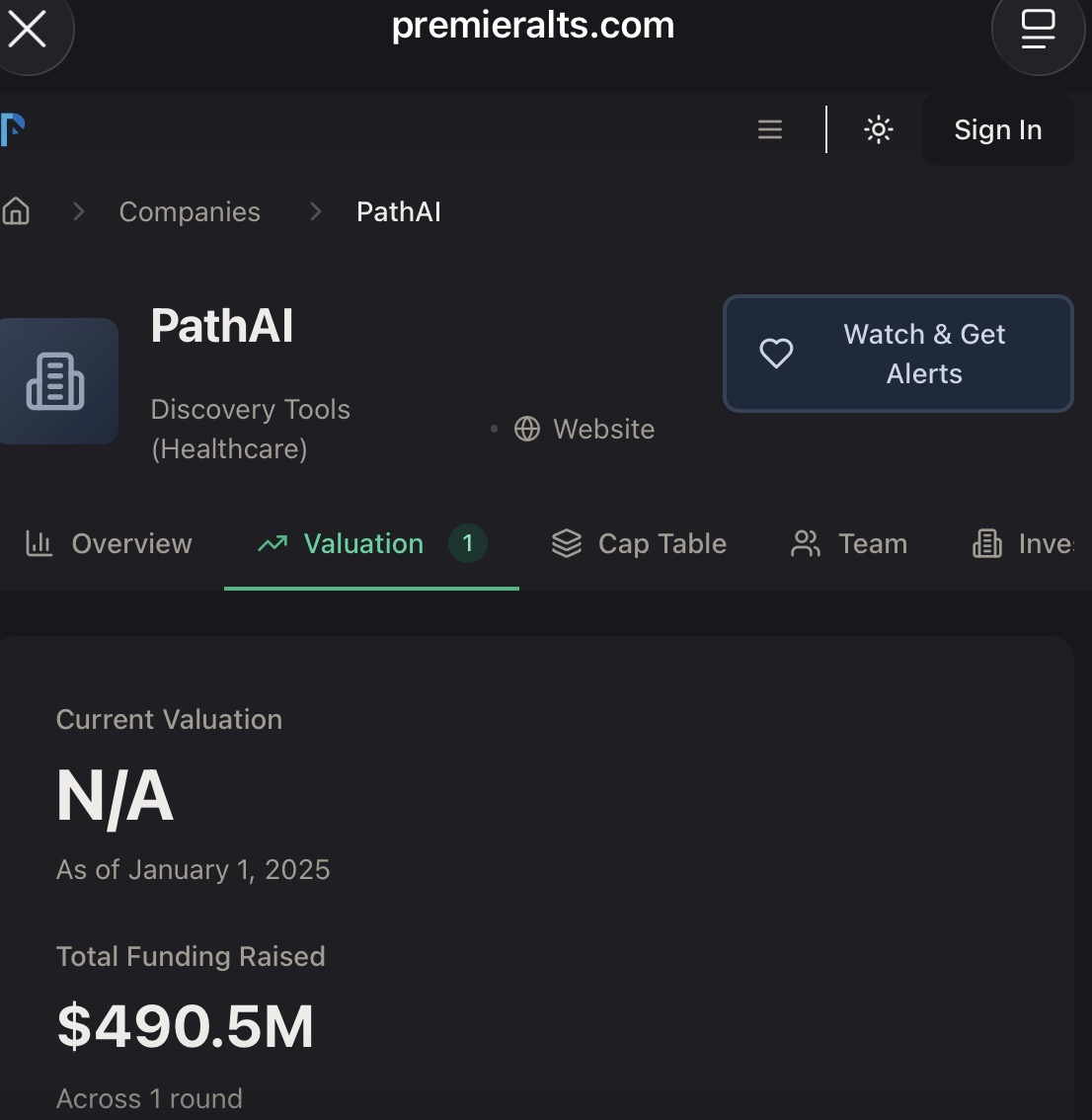

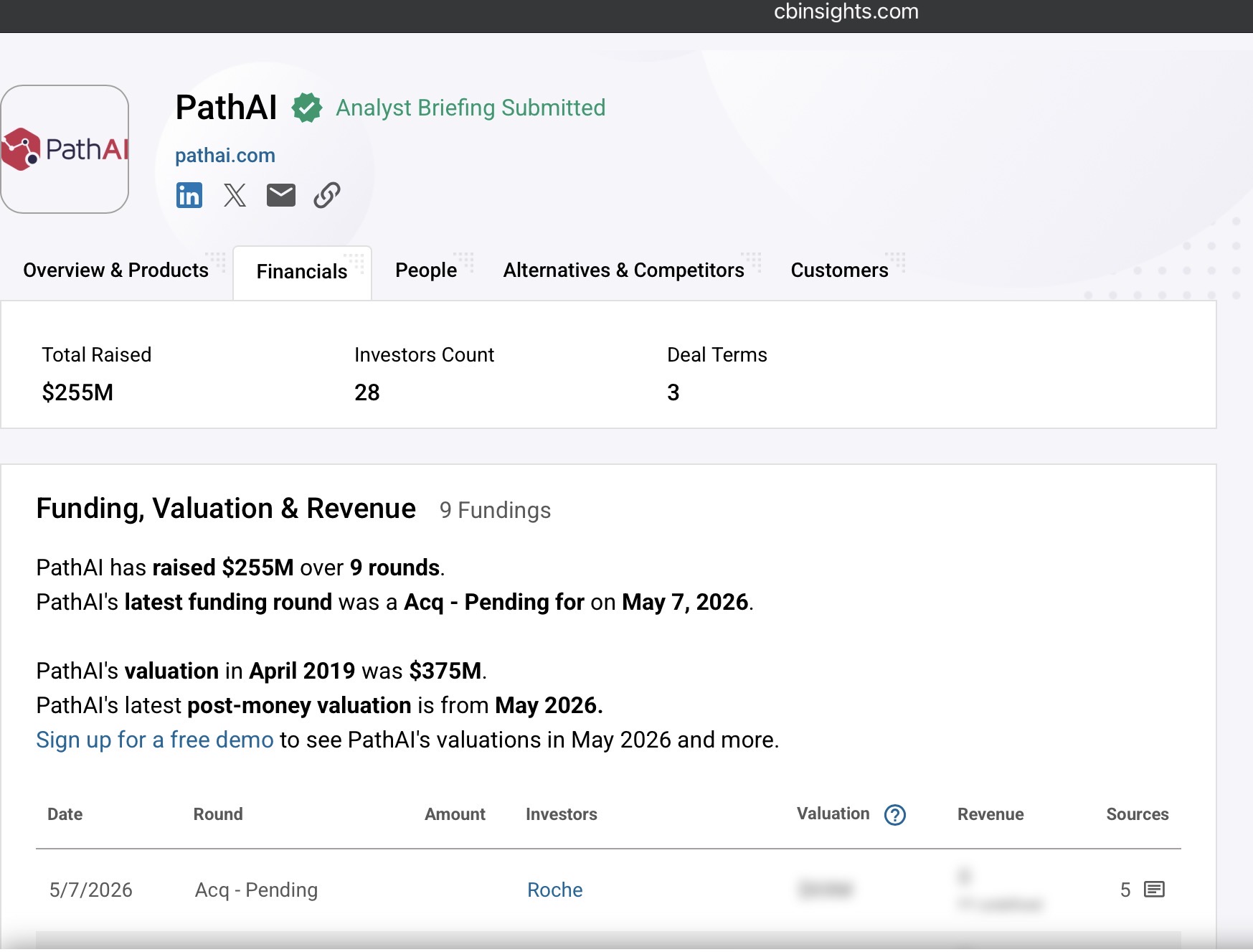

Path AI oli tosiaan yksityinen yritys, jolle ei virallista hintaa voinut pörssistä katsoa. Rahaa on kaadettu jenkkilän tapaan reilusti, eri lähteiden mukaan 250-500 MUSD. Siten sijoittajat saavat parhaimmillaan 2-4x tuoton.

Hesulin pikkuveljen Finolin tämän hetken arvostuksilla exitiin tähtäävät pääomistajat eivät todennäköisesti muuta kuin kuuntele hymähdellen tarjouksia, jos sellaisia tulee, tarkkailijoita epäilemättä on aina yhtiöissä, jotka ovat kiinnostavia integroitavia. Aiforialla on kasvava salkku kilpailussa pärjääviä tekoälymalleja ja työkalut mallien kehittämiseen. Talouden käänne aiheuttaa viimeistään kiinnostuksen lisääntymisen, sitten kun.

Path AI:lla on vähän eri fokus kuin Aiforialla. Tekee Aiforiakin yhteistyötä pharmojen kanssa, mutta kliiniset mallit ihme kyllä pärjäävät kilpailussa hyvin ainakin Euroopassa, vaikka pikkurahoilla täällä pelataankin, jos verrataan.

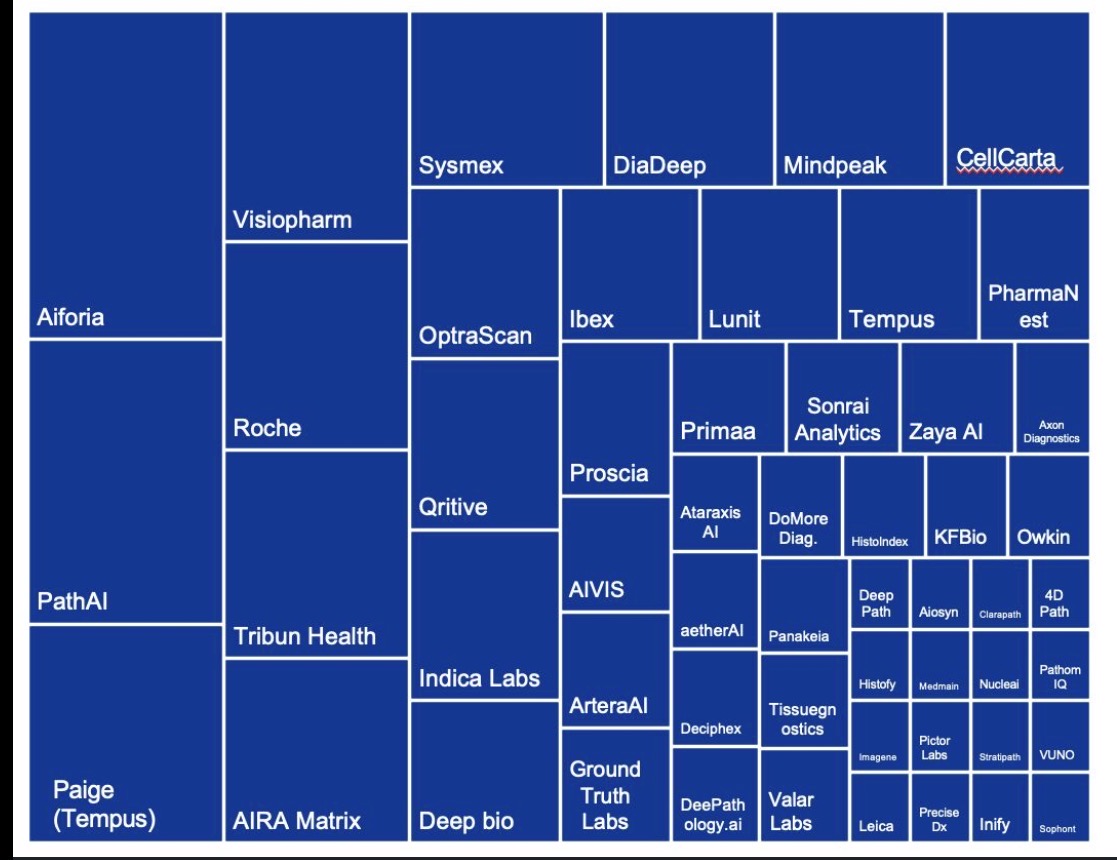

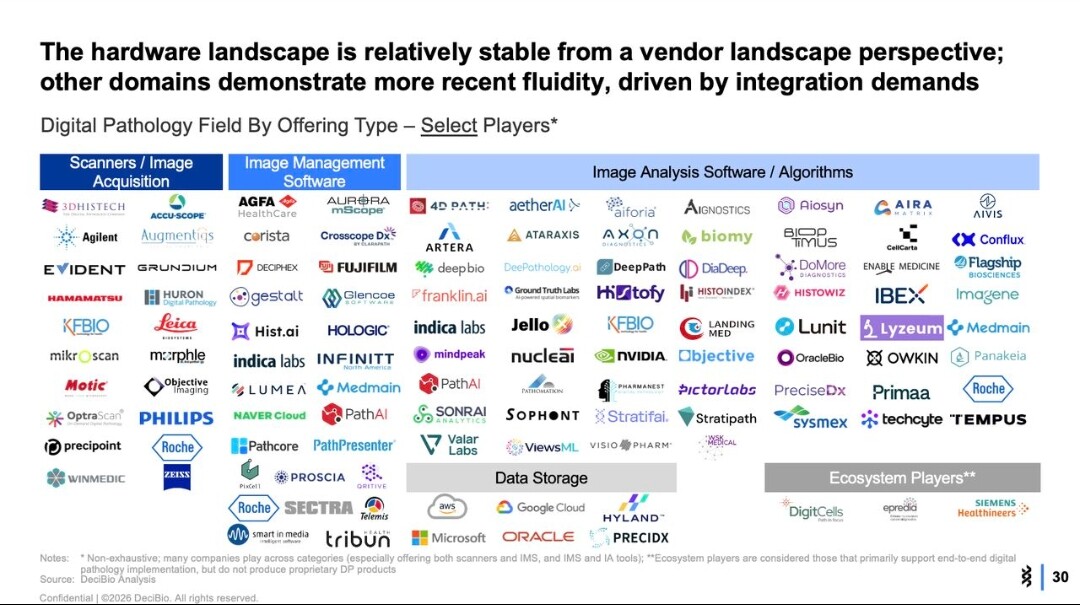

Hyllyvalmiit mallit kenttä (em, Katien postauksesta, häntä kannattaa seurata).

Vielä riittää konsolidoitavaa. Mikäs siellä on (oli ennen Path AI+Roche) ykkösenä? Kärkisijoilla olijat pitävät paikkansa todennäköisimmin, kukaan ei halua työkalujen ja toimittajien tilkkutäkkiä.

15 tykkäystä

Saman Katie Maloneyn toinen julkaisu liittyen digitaalisen patologian tilkkutäkkisyyteen.

Jää tähän tuoreimmankin kaupan jälkeen järjestelyvaraa, Aiforia mainitaan ‘Platform leaderinä’.

19 tykkäystä

Hyvään saumaan tuli tämä Rochen ja PathAi:n diili Aiforian kannalta myös. Näiköhän hallitus rynnii heti ylimääräisen yhtiökokouksen jälkeen annin läpi? Saisi ainakin paremmalla valuaatiolla mitä olisi saanut 3kk aikaisemmin ![]()

Kauan muuten sisäpiirillä on ns. Suoja-aika osakeostojen kanssa ilman, että tulee syytöksiä sisäpiiritiedon väärinkäytöstä? Aiforialla ei taida olla muhimassa ainakaan vielä mitään diiliä kenenkään kanssa, koska sisäpiiri on ollut ostolaidalla vielä maaliskuun lopussa.

1 tykkäys

Ei kai aivan vielä kiirettä ole, siellä on tulossa mm. uutta kliinistä mallia ulos kesään mennessä, ja ehkä uusia asiakasopimuksiakin, voipi kannattaa himmailla annin kanssa hetki.

4 tykkäystä

Mitä omia aikaisemmin tehtyjä laskuja pläräilin, niin kassassa oli 9m€ joulukuussa. Tämä kyllä riittää syksyyn, mutta aivan nahkoille ei kuitenkaan päästetä. Voisin veikata antia kuitenkin vielä H1 puolella.

3 tykkäystä

Itse asiassa, jos kerran (noihin Linkedin-posteihinkin) viitaten konsolisaatio on jo vahvasti käynnissä, ja Aiforia on muutaman johtajan joukossa/ehkä jopa vakuuttavimpana ei-jo-ostetuista, miksei yritysostoa voisi tapahtua paljon arvelemaani nopeamminkin?

Onko Aiforialla jotain milestoneja, jota pitäisi ensin saavuttaa?

Tarvitaanko ensin liikevaihdon myötä jotain ”osoituksia”, vai riittääkö, että mallit on hyviä ja EU-hyväksyttyjä ja laajasti sopimuksia kyetty tekemään?

(FDA-hyväksyntöjen hakemiseen sopivin aika olisi vasta, kun joku toimija olisi integroinut Aiforian osaksi skanneri/kuvankäsittely/AI -kokonaisuutta, koska FDA myöntää toistaiseksi luvat ainoastaan tällaisille kokonaisuuksille…)

6 tykkäystä

Voisi kuvitella, että ostaja odottaa liikevaihdon kasvua sekä kassavirtapositiivisuutta. Tällä hetkellähän Aiforia on vielä mielestäni kallis yritusostokohde nykyisellä valuaatiolla.

1 tykkäys

Sinänsä en ole varma, olisiko isolle toimijalle väliä sillä, ollaanko tilanteessa, että tappiota tulee muutama miljoona tai voittoa muutama miljoona, jos suunta on selvä. Kai siinä ennen kaikkea ostetaan AI-malli, joka voidaan integroida omaan tuotteeseen varmistamaan oman tuotteen (esim. skanneri) kilpailukyky (Jukkahan on toistuvasti haastetteluissa sanonut, että AI on lopulta se porkkana, joka tuo sen hyödyn ja mistä kaikki ovat kiinnostuneita, mikä voisi sen kilpailuedun (siis esim. skannerivalmistajalle) luoda)

Liikevaihto sinänsä luo uskottavuutta, tuote on tavallaan validoidumpi, testatumpi, käytännössä varmaan tunnetumpikin firmalla jolla myyntiä on paljon.

Onneksi Aiforialla alkaa olla aika hyvin kliinisellä puolella referenssejä, vaikka vasta liikkeelle lähtenyt kliinisen puolen liikevaihto!

No jos valuoi suhteessa liikevaihtoon/voittoon mitä ei ole, niin varmasti näin. Jos taas ajattelee, että joku haluaa ne AI-mallit, niin onhan tämä nyt 15 kertaa halvempi markkina-arvolta kuin vähemmän malleja omistava taho mikä just ostettiin. Ajoissa ostamalla voisi siis saada hyvän AI:n vielä järkevään hintaan, voitollinen firma muutaman vuoden päästä jo kalliimpi ![]() (jos siis joku taho näkisi jo tässä vaiheessa Aiforian AI:n olevan heille sopiva)

(jos siis joku taho näkisi jo tässä vaiheessa Aiforian AI:n olevan heille sopiva)

12 tykkäystä

Ylimääräisessä yhtiökokouksessa tiistaina 12.5 annetaan hallitukselle valtuutus suorittaa maksimissaan 5m osakkeen anti. Antihinta tulisi varmaan olemaan tällä kurssilla 1,7-1,8€ osakkeelta ja osakemäärä nousisi 33,6m → 38,6m. Antit odottavat vielä yhtä n. 6m osakkeen antia tämän jälkeen. Saa nähdä tarvitaanko vielä tuota toista antia vai ei.

Joka tapauksessa tämä ensimmäinen anti pitäisi riittää sitten kevyesti vuoden päähän. Toimarihan sanoi myös H2 infossa, että jos latu on auki vahvalle kasvulle, niin ei näe ongelmaa vielä hommata lisärahoitusta. Mainitsi myös, että on mahdollista jarruttaa kasvua ja keskittyä tulokseen, jos tilanne siltä näyttää.

Toivottavasti tulevassa annissa olisi vähän sitoutuvampia osallistujia verrattuna joulukuiseen, eikä dumppaisi heti laitaan uusia osakkeita.

6 tykkäystä

Onkotuo nyt sitten piensijoittajalle n.14 % laimennus..?kun pelikentän laidalle jää annissa kuitenkin…

Itse vähän uumoilin, että Aiforia ostetaan pois kun käyttökate kääntyy plussan puolelle ja ihan viimeistään kun kassavirta kääntyy positiiviseksi, mutta jos kaislikossa suhisee tähän malliin, niin voihan tuo mennä aiemminkin.

2 tykkäystä

Kyllä joku iso kala tämän varmasti jossain vaiheessa ostaa, mutta tuskin vielä hetkeen, koska sisäpiiri ollut vasta ostoksilla. Mielestäni olisi myös parempi kehittää yhtiötä vielä pidemmälle ja saada enemmän referenssejä sekä tekoälymalleja → parempi valuaatio. Mielelläänhän tämä myös pitäisi Helsingin pörssissä eikä aina myytäisi kaikkea pois heti ![]()

4 tykkäystä

No kyllähän tässä ihan omistajakuntakin on osin ongelmallinen kun pysäytti kasvutarinan kannalta välttäämömän annin.

5 tykkäystä