Atte has published a new company report on Aallon Group

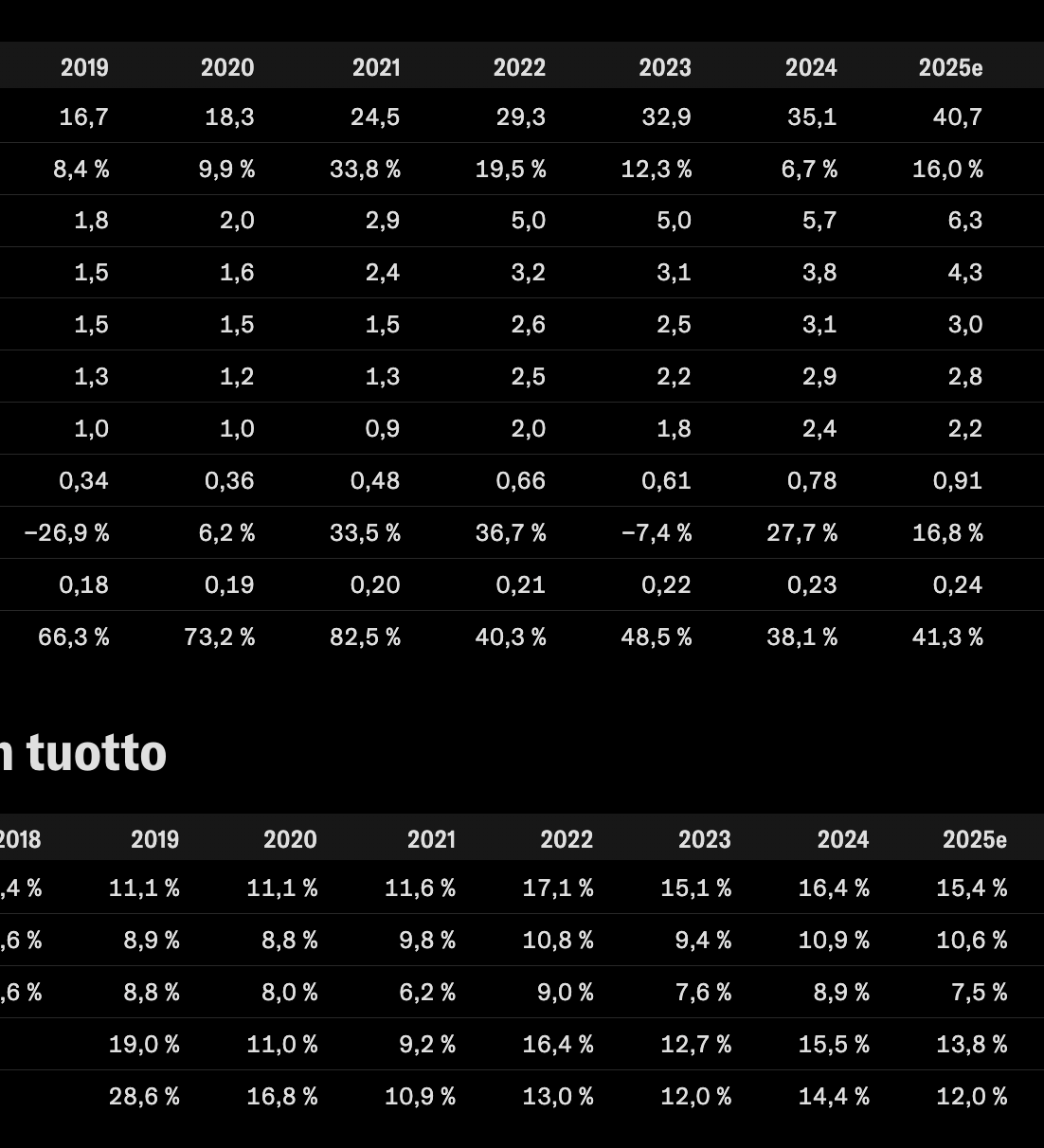

We reiterate our target price of EUR 13.0 for Aallon Group, but following the share price decline, we are upgrading our recommendation to Buy (prev. Accumulate). We have included the company’s two latest small acquisitions in our forecasts, the impact of which on the earnings forecasts for the coming years was only around 1%. However, Aallon Group’s share price has been declining since our last update, and the valuation (2026e adj. P/E 10x) looks attractive in our view relative to the company’s steady and strong cash-flow-generating business and medium-term earnings growth prospects.

Additionally, the number of shares has increased by less than 10% (3.6m → 3.9m → 3.8m) as the company became active in repurchasing its own shares.

Dividends have also been paid increasingly, totaling €1.23/share since the IPO.

Edit: A new CFO has been appointed. That happened quite quickly.

Henri Enola has strong experience in developing financial management for listed companies, financial transformation projects, IPO projects, M&A, and IFRS reporting, among others. Previously, Enola has served as a director in financial management advisory services at EY and, before that, at Nokia. He holds a Master of Science in Economics and Business Administration.